The proliferation of advised model portfolios has led to them becoming an “expensive administrative burden” for some firms, Aegon has claimed.

Advisers could be burdened with having to administrate as many as 300 portfolios as slow responses from clients cause them to drift in out-of-date models.

Advised model portfolios, particularly on platforms, have remained popular investment choices in recent years despite the emergence of alternative options such as outsourcing to a discretionary fund manager or advisers taking on discretionary permissions themselves.

But the need to obtain permission before making changes to an advised portfolio means intermediaries can be forced to leave some clients in old models.

Garry Latimer, head of retail proposition at Aegon UK, said: “Even firms with the best processes in the world may only have a 95 per cent success rate of contacting clients and getting agreement. This means there will always be clients left behind in old model portfolios. In a reasonably sized firm, there can easily be the odd client in 300 model portfolios.”

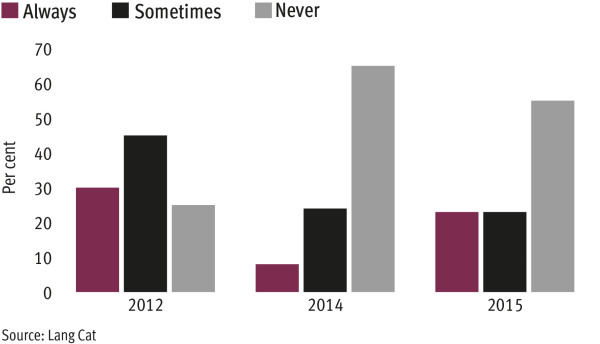

Mike Barrett, consulting director at the Lang Cat, said: “It is really messy. You end up with so many different versions. If advisers do not stay on top of it, it almost defeats the purpose [of model portfolios].”

Mr Barrett said the proliferation of portfolios was “definitely a problem” for advisers and has become increasingly apparent due to the growing popularity of advised model portfolios on platforms. While the excess portfolios present an administrative headache for advisers, clients in out-of-date portfolios could miss out on gains or be hit by losses not incurred by the up-to-date portfolios.

Mr Barrett called on platform providers to develop solutions to aid advisers with the portfolio proliferation problem.

He pointed to Transact, which has introduced a “client authorisation tool” for speeding up the process of obtaining client approval and then implementing changes to model portfolios. He said Nucleus was trialling a similar tool and called on other providers to follow.

Alistair Cunningham, who runs advised model portfolios for Wingate Financial Planning, said while he thought Aegon had overstated the issue, there were problems with clients not replying in spite of advisers’ best efforts. One solution used by Wingate was to recommend to “serial offenders” who rarely reply to requests that they move into Wingate’s passive models, which are updated annually.

Mr Cunningham said obtaining discretionary permissions was the ideal solution, but added the onerous capital adequacy requirements imposed on firms with these permissions had held Wingate back, leaving it likely to carry on managing advised portfolios and having to chase clients for every change.

Matthew Bird, who runs advised model portfolios for Seer Green Financial Planning, said: “All clients are warned at point of policy setup about the importance of reviews [and] rebalancing. The occasional one that doesn’t respond at their annual review must be left in the original portfolio, which can drift in asset allocation over time, which isn’t ideal, but we endeavour to keep in contact with the client and remedy this.”

Fraser Donaldson, insight analyst at Defaqto, said the problem had been helped by technology advancements. “The use of platforms means it is a lot easier to monitor who has and who has not changed,” he said.

KEY NUMBERS

31%

Adviser research by NMG has found 31 per cent of investments below £50,000 are in models

Q4

The FCA is to study platforms, encompassing model portfolio usage, in the fourth quarter