Power prices have been on people’s minds in 2020, with the pandemic causing a drop off in demand and further softening of prices, followed by a subsequent firming up. Forecasting power prices is key for renewable energy generators, and in this week’s instalment, Will Argent, Fund Adviser to the VT Gravis Clean Energy Income Fund, discusses the varying impact of power prices.

For any renewable power generator, the price of electricity – and long-term forecasts – will be important in projecting the revenue streams that a wind farm or solar park, for example, can generate over its assumed lifetime.

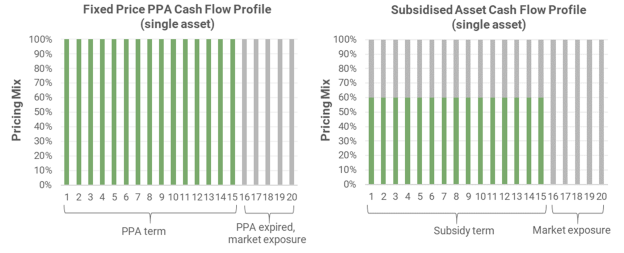

For companies that own renewable energy assets with long-term fixed/known price Power Purchase Agreements (PPAs) for the electricity they generate, there is very little/no sensitivity to fluctuations in power price expectations, as cash flows are linked to a pre-determined price. Such arrangements appear frequently in North American renewables projects where contracts can be >15 years in length.

Where PPA markets are less developed, such as the UK, the build-out of renewable energy capacity has been aided by subsidies that provide some certainty for the cash flows which incentivises developers to commit to a project. For example, the Renewables Energy Certificate, Feed-In Tariff and Contract for Difference schemes, used in the UK, Europe and Australia, assisted by facilitating a payment to the generator per unit of electricity produced, or by providing pricing certainty for the expected output from an asset over a 15-year time horizon (or longer). Although, there remains uncertainty as long-range forecasting is difficult and can lead to inaccuracies.

Example of simplified cash flow profiles for single renewable energy asset (fictional) under long-term fixed PPA and subsidy basis

The ‘value’ of assets developed without any form of certainty to the cash flows are highly sensitive to movements in near-term electricity prices and long-term price projections. Now renewable energy technologies are geographically widespread and cost-competitive with conventional forms of electricity generation, the construction of new, unsubsidised assets is increasing. The asset owner must be prepared to take on material uncertainty for future cash flows. However, that risk may be considered acceptable: it is widely anticipated that society will become increasingly reliant on electricity, e.g. through the electrification of transport and heat, and increasing digitalisation – the International Energy Agency forecasts annual demand growth of c.2% per annum between now and 2040, price increases in real terms over coming decades.

Renewable energy assets located in different geographies, where subsidies differ, or assets that are of varying ‘vintage’, since subsidy schemes have adjusted over time, will typically have different cash flow profiles due to the underlying mix of fixed and merchant price exposure. Companies that own diversified portfolios of renewable energy assets (by geography, technology and vintage) will have a unique blend of cash flows and varying degrees of sensitivity to assumptions relating to power prices.

Near term cash flow mix (1 year view):

Since asset valuations are calculated by discounting future cash flow expectations, a higher exposure to merchant power prices results in valuations having greater sensitivity to movements in price projections – both near-term and long-term. We see this in the net asset valuations reported by UK-listed renewables companies on a quarterly basis, which incorporate the latest long-term pricing projections from energy consultancies. The table above provides three company examples which demonstrate varying exposures to fixed pricing and resulting merchant power price sensitivity.

Over the last year or so, electricity price forecasts have been under pressure. On the supply side, a general oversupply of oil and natural gas has weakened pricing (electricity prices are still somewhat linked to the trajectory of gas prices) while on the demand side, the Coronavirus pandemic and resultant cessation of economic activity meant that demand fell sharply during March and through Q2 2020, compounding the price weakness.