The Standard Life-Aberdeen mega-deal has prompted analysts to question the assumptions underpinning not only the deal but also asset management merger and acquisition (M&A) activity in general.

Researchers from Berenberg and RBC Capital Markets have added their voice to those who have suggested fund selectors will be hesitant to use Aberdeen or Standard Life Investments (SLI) products because uncertainty could affect performance.

While analysts expressed understanding for the long-term benefits, they added uncertainty around which funds would close and which managers would leave could put off buyers until the dust settles on the mega-merger.

RBC analyst Peter Lenardos said the issue could crop up more as M&A deals get larger.

“Merger announcements pressure flows, as consultants and advisers are usually reluctant to push funds from companies that are merging, due to likely dislocation among investment staff and the possibility for performance issues.

“Consultants and advisers may also review existing positions within merging asset managers, which could further exacerbate gross outflows.”

Mr Lenardos said the problem could affect the Henderson-Janus Capital merger, despite Henderson chief executive Andrew Formica saying last month that the firm’s UK investor fund range is unlikely to be combined with Janus’ offerings.

Berenberg analyst Trevor Moss said comments from SLI and Aberdeen suggesting that few consultants would put the merged business on watch seemed “optimistic”.

“In most fund management mergers, where there is actual overlap, there is some loss of AUM. Assets were shed even in Standard Life’s fairly uncontroversial acquisition of Ignis Asset Management ... even if consultants do not officially put the companies ‘on watch’, [advisers] and institutional investors will still be wary of pushing flows into a company until they see what it means for individual products and teams.”

Mr Moss said preventing this uncertainty by locking in key staff would be difficult, given the size of the deal.

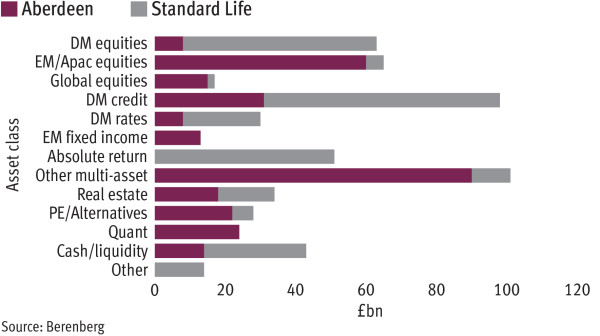

For Aberdeen and SLI, the AUM crossover is not overly significant at a group level. Aberdeen has expertise in emerging market equity and debt, multi-asset and quantitative funds, while SLI’s focus is on developed market equity and debt and absolute return.

However, there is noteable duplication in terms of retail funds. The two firms have similar funds in almost every Investment Association sector. Both have six funds in the IA UK All Companies sector, and they account for six of the 47 funds in the IA Property sector.

James Calder of City Asset Management said: “The merger would not stop us buying Aberdeen’s closed-ended funds because they have given reassurances. But we might be more reticent to invest in the open-ended funds.”

Mr Calder said he sometimes uses SLI’s developed market equity funds, such as the top-performing Unconstrained range. He admitted there was now uncertainty around those strategies.

“I would be gobsmacked if any SLI developed market equity managers had to fall on their swords to accommodate Aberdeen managers,” he said. “But there may be concerns about capacity: will the managers be comfortable managing much bigger funds [if the Aberdeen portfolios are merged into SLI counterparts]?”

KEY NUMBERS

6/47

Number of funds in UK property sector managed by Aberdeen or SLI

£660bn

Pro-forma AUM of the two companies