Most investors should be content with the returns they have received so far in 2017. Equity markets continue to flirt with new highs, and bond markets have recovered from the lows earlier in the year.

The MSCI All-World index had gained 6.9 per cent in sterling terms, as at May 30, and the Bloomberg Barclays Sterling Non-Gilt benchmark was up 2.9 per cent.

Probably the main story in 2017 has been the fading of the reflation and value trade, which started last summer and gained traction after the US presidential election. Donald Trump’s failure to make progress on tax cuts in the country has dampened expectations for inflation, leading to lower bond yields globally.

However, economic growth expectations have held up. After a weak first quarter in the US, the second quarter has looked much stronger. In addition, the strength of the economies in Europe and the UK has surpassed many expectations. In China, the economy has benefited from government stimulus, and growth continues at a robust pace.

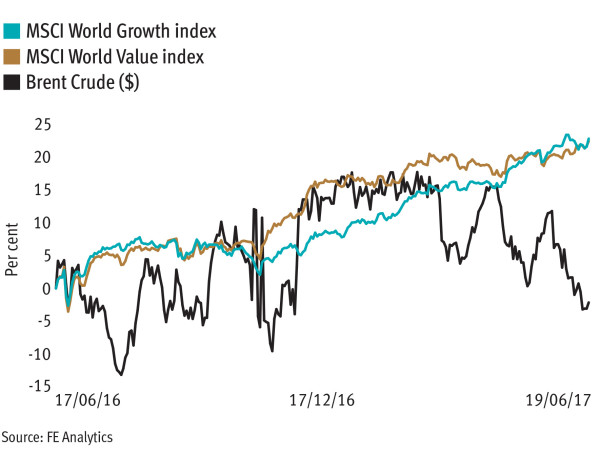

Despite this there has been significant rotation within equity markets. As reflation fears (or hopes) receded, growth stocks have come back into vogue at the expense of value.

In the US, for example, just five companies accounted for roughly one-third of the return of the entire market – Apple, Amazon, Facebook, Microsoft and Alphabet (Google). Lower inflation means lower interest rates, and these shares are up 25 per cent as a group due to the fact that their long-term growth is worth more if a lower discount rate is used.

At the same time the traditional value sectors of energy and financials have underperformed, as yield curves have flattened and commodity prices have rolled over.

So where will inflation expectations go from here, and how will that impact short-term interest rates and long-term discount rates?

One of the most important inputs to headline inflation expectations is the price of oil, and the balance between demand and supply appears to be changing. This could spoil the party for growth stocks and give a lease of life for value stocks. At the recent Opec meeting the cartel agreed to extend its agreement with Russia to curtail production for another nine months.

Unlike previous agreements, compliance with recent deals has been very high. Production is running at about 32m barrels per day (bpd) – about one-third of global production – and is down more than 1m bpd compared with the 2016 average.

There has been a lot of focus on the pick-up in US shale production, but this has increased by only 500,000 bpd on the same comparison.

Meanwhile, oil demand in emerging markets continues to be strong and inventory levels have started to decline. Markets appear to be disappointed that Opec was not more aggressive, leading to some softness in the price of the commodity. But the International Energy Agency is now estimating that global demand for oil is greater than supply.

All things being equal, this should put upward pressure on the price and reverse the recent favourable trend for growth stocks.

Should inflation expectations rise again, we could see another retreat from bond markets where current levels of real yields are well below long-term averages. If a return to ‘normal’ inflation is in prospect and investors are less concerned about the risk of deflation, real yields should rise.

Central banks are likely to taper their monetary accommodation policies and the US Federal Reserve push ahead on its path for higher rates. Very little of this is discounted in markets today and could cause rotation and volatility.

In 2004-05 the Fed raised interest rates from 1 per cent to 4 per cent, but the equity market continued to rally. This was because the economy was strong and companies were growing profits and dividends.

The cycle this year has been very different, and there are challenges ahead that make it very difficult to be sure history will repeat itself. Investors face both political and economic uncertainty in all parts of the world, which should restrain over-exuberance – probably not a bad thing.

Jeff Keen is a director and co-head of fixed income at Waverton Investment Management

KEY FIGURES

November 30

Date of the next Opec meeting

1-1.25%

US federal funds rate after June’s hike

8ppt

Global growth stocks’ outperformance over value peers year to date

1.68%

US inflation expectations as of June, now below the level at last November’s election