Conversations about US equities have focused on three different areas this year. As valuations continue to rise, volatility remains near record lows and retail investor interest appears somewhat mixed.

Strong leadership from US technology stocks has helped push returns higher, with the so-called Faang (Facebook, Amazon, Apple, Netflix and Google – now Alphabet) companies marching higher. The flip side of this is dismay at valuations. The S&P 500 index’s forward price-to-earnings ratio is more than 18 times, well above its global counterparts’.

A further uncertainty concerns volatility. The Vix volatility index moved back below 10 last week, a level rarely reached in its history, indicating – on the surface at least – almost total calm. Despite a short-term blip surrounding tensions with North Korea, volatility remains anchored.

This somewhat muddled outlook has led to moderate fund sales. The IA North America sector has seen positive flows in five of the opening seven months of 2017, reaching a total of £780m. But equity sales overall have hit £5.2bn, suggesting the US may no longer be favoured from either an active or a passive perspective.

The North America sector has fallen behind its Europe ex UK counterpart, which secured £1.2bn of sales over the period despite being more than £15bn smaller in size. The IA Global group has seen £2.2bn of net sales, leading the way in inflows for much of the year, though this category is twice the size of the North America cohort.

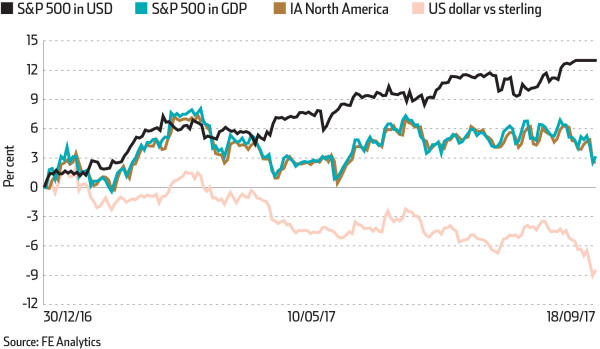

Currency may have also had a part to play in dampening demand. The S&P 500 is up 13 per cent in US dollar terms year to date, but the greenback’s weakness against sterling and euro has started to affect investor sentiment. Currency movements have meant the index is only up 3.2 per cent in sterling terms. The dollar is down 8 per cent against the pound and 12 per cent versus the euro so far this year.

Fund managers have started retreating as well. This month US equity allocations fell 6 percentage points to a 28 per cent underweight – the largest negative positioning since November 2007 – according to the Bank of America Merrill Lynch global fund manager survey. This drop is far below the long-term average and comes despite overall equity allocations sitting at a 34 per cent overweight.

Despite this, managers in the sector with exposure to tech have delivered. The Faang stocks now account for 12 per cent of the S&P 500. The leading funds have gained 22 per cent year to date, with most holding the Faang names in their top 10s to achieve these returns.

So there are returns to be found from US stockpickers, but the notion of this being a difficult market to beat remains true. A lack of volatility will only add issues for active manager performance, despite the market having risen steadily upwards. Few expect a spike in volatility in the near future.

Neuberger Berman’s multi-asset chief investment officer Erik Knutzen notes that the Vix index has closed at record lows six times this year, marking a longer-term run wherein equity volatility is lower than that of US Treasuries.

He adds: “As long as realised volatility continues to be lower than that implied in options markets, and as long as the major central banks stand as the marginal buyer of financial assets, the market’s volatility structure can remain suppressed.”

THE PICKS, BY FE

Artemis US Select

Cormac Weldon adopts a flexible approach to investing in this £621m strategy, in which he adapts the portfolio according to where the best opportunities lie. Mr Weldon moved to Artemis with the majority of his US equity team from Threadneedle to replicate his previously successful investment process. Stockpicking has traditionally been the largest contributor to the fund’s outperformance over the S&P 500, returning 20 per cent in the past year versus a 15 per cent rise by the index.

Fidelity American Special Situations

Angel Agudo’s approach involves investing in stocks that have fallen out of favour with investors. Mr Agudo prefers companies with recovery potential and limited downside risk. The £1.3bn fund backs the IT and Financials sectors, with allocations of 25 and 21 per cent respectively. The portfolio has outperformed the S&P 500 index and IA North America peer group in every calendar year between 2013 and 2016, but has struggled year to date.

EDITOR’S PICK

Baillie Gifford American

Tom Slater, Gary Robinson and Helen Xiong run this concentrated portfolio focusing on exceptional businesses with growth potential, a good culture and an “edge”. The fund is biased to consumer discretionary and IT, particularly firms that utilise technology to transform conventional business models. Concentrated positions in such stocks have led to strong year-to-date outperformance relative to the S&P 500 index and the IA North America peer group. Over three years the vehicle has returned 84 per cent, against a sector average of 49 per cent and a 58 per cent gain by the index.