Article 3 / 4

The Guide: Investing in emerging market equitiesStrong foundation driving bull market

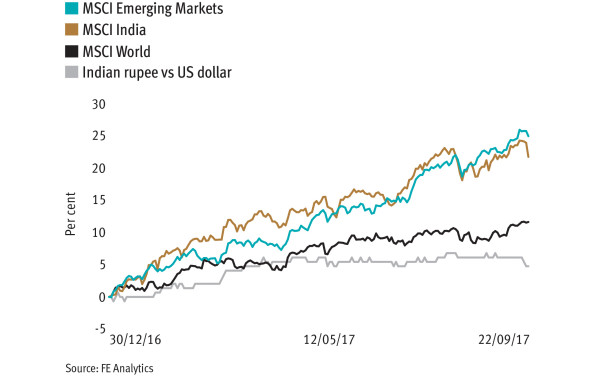

The Indian investment opportunity is not new. The country features prominently in most global emerging market portfolios, and has indeed been one the best performing equity markets in 2017.

As far as allocating to emerging markets goes, it’s difficult to argue that India is not a relatively consensus investment. And for good reason. The well-known demographic tailwind, a stable political backdrop and a relatively insulated economy, combined with recent reforms, creates a strong foundation to drive a multi-year bull market.

Prime minister Narendra Modi possibly deserves more credit than he gets. He may have had luck on his side with oil prices tumbling, but he has enjoyed broad support to push through reforms. Nonetheless, demonetisation was a brave move, and the goods and services tax (GST) had been debated for 16 years before its eventual implementation this year. Mr Modi pushed through both in quick succession.

The GST bill is described as the biggest rule change in India since independence for its ambition of targeting large-scale problems, such as price transparency and price consistency of goods across different states. It is also seen as a positive development for governance, both for the government and corporates: it should improve data collection and transparency, increase the tax base and improve efficiency, both in production and consumption.

Economists estimate that the new tax bill could add as much as 1 to 1.5 per cent to GDP over time. However, it does not come without risks – infrastructure to name one. Some 20 per cent of the population does not have access to electricity, and infrastructure is still underdeveloped by almost any standard.

The next general election is in 2019, and it’s likely Mr Modi will start to focus on job creation and investment. This should ensure both cyclical and structural support for the economy and corporate profit recovery.

Inflation remains subdued, while real rates are as high as they have been in the past decade. Expectation for GDP growth in 2018 is as much as 8 per cent.

Combine all this with the attractive demographics, low credit penetration, benign oil prices and a good monsoon season, and leading indicators are unsurprisingly positive. Both business and consumer confidence are picking up, and a multi-year profit recovery is indeed possible. Many sell-side analysts are indicating 15 to 20 per cent corporate earnings growth for the next few years.

Investors should be mindful of the risks. This year is likely to be strong for earnings growth, but until now the recovery has disappointed. Demonetisation was brave, and the consequences and short-term liquidity shortfall are more severe than first indicated. GST will have long-term benefits, but as with every other state bill, deadlines will almost certainly be missed and implementation will be less smooth than hoped for.

The biggest risk, however, is a derating. Earnings and cashflow multiples are at multi-year highs – a forward price-to-earnings ratio of just under 20 times represents an Indian market that is more than two standard deviations above its long-term average, and very close to its all-time high. Should the profit recovery come through and be sustained, the market might grow into these multiples, but history would suggest investors will have a more attractive entry point at some point in the future.

An often-neglected factor is currency. The Indian rupee is trading at an all-time high on a trade weighted basis. Even with the economy in good shape, a robust investment outlook and more stable current account, there is clearly more downside risk to the rupee.

The foundations have been laid for a multi-year bull market in the country. The demographic, political and economic backdrop all point towards a brighter future, but the market seems to know it.

Today might just be the time to remember Warren Buffett’s wise words: “Be fearful when everyone is greedy, and greedy when everyone is fearful.” Right now, it’s difficult to find anything to fear, and almost everyone seems to be greedy.

Ernst Knacke is a fund research analyst at Quilter Cheviot