The move to list marks the completion of a turnaround for the company, which is expected to be valued at around £5bn, according to the Financial Times.

This decision will be a relief for active managers on the UK equity markets. The initial public offering (IPO) market is a well-known source of alpha for them, due to the length of the process behind a listing.

The underpricing of IPOs is a well-documented fact of empirical equity market research – underpricing being the difference between the issue price of a new share and the first trading price on the secondary market.

One study, conducted by Professor Jay Ritter, reports results from stock exchanges in 38 countries, all of which show evidence of first-day abnormal returns.

Despite the presumed intention of underwriters to obtain the best price for the issuing firm by balancing supply and demand, the evidence is less than convincing that they can accomplish this task consistently.

An active equity manager can therefore, generate some excess return by participating at the IPO and selling on the trading day.

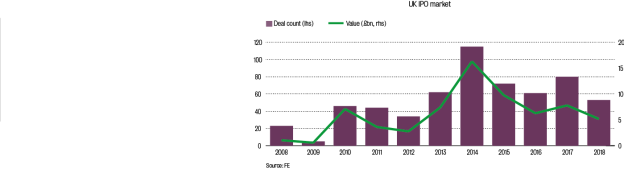

It is fair to say that this source of alpha has significantly dried up in recent years. Looking at the IPO list since 2016, except for the announced listing of Aston Martin, the size of the deals has been low.

The largest deal concerned medical products specialist ConvaTec, which raised £1.47bn from stock investors. Other notable names include Avast, ContourGlobal and Ascential.

The deal list gives us an insight into the structure of the UK equity markets, which tend to be concentrated around two main industries: financial services and commodity-related industries. The best example is the listing of Vivo Energy in April 2018, the biggest African-focused IPO for over a decade.

The petrol station and retail chain raised £650m from UK equity investors. Within financial services, we can look to the likes of Quilter Cheviot, Metro Bank and Sabre Insurance, all of who have raised capital over the past three years.

One could have expected UK equity active managers to rush on those deals. This was not the case.

It looks like active managers only became interested in the IPO of Sabre Insurance in June 2016. Well-known investors such as Thomas Moore at Aberdeen Standard Life, Simon Brazier at Investec and Daniel Nickols at Old Mutual Global Investors participated in this issuance.

Nick Price at Fidelity also took a small stake in Vivo Energy for his emerging markets fund.

What could the reasons have been for not fully participating? Was the issue price of a new share correctly assessed?

Given the high number of companies that have decided to withdraw or postpone their listings, it can be assumed this was not the case. Once again, Brexit generated a lot of confidence for company management teams to get their shares listed on UK markets at the right price.

Additionally, academics have proven that the size of IPO underpricing is cyclical; for example, at the height of the dot-com bubble, the average IPO was underpriced by more than 50 per cent.

For UK equity active managers, there was little uncertainty that this IPO mispricing effect would work again, given the small appetite for UK equities among global investors.

With little conviction on alpha being generated from the IPO market, UK equity active managers turned to the mergers and acquisitions market, as the discounted valuations for UK companies offered fertile ground for overseas companies to harvest.

Charles Younes is research manager of FE