Article 4 / 7

Summer Investment Monitor 2017Making the most of smids to tackle anomalies of size

European markets are on the up, small and medium-sized stocks included. Currently, small caps generally span companies ranging from €200m (£176m) to €2bn while mid caps constitute the next level up to about €10bn.

The size effect is an equity market anomaly suggesting that smaller companies can provide higher returns than large caps.

The first serious study of the size effect was published by Banz in the Journal of Financial Economics in 1981. It showed that US companies accounting for the top 30 per cent of all stocks in the market in terms of market cap significantly underperform those accounting for the bottom 30 per cent.

One dollar invested in these larger caps in July 1926 would have turned into $4,301 (£3,380) by the end of December 2016. Impressive as that might be, the same dollar would have turned into $25,899 if invested in the bottom 30 per cent of names. However, along with these higher returns came higher volatility – 27.5 per cent for small caps versus 17.9 per cent for large caps – over the period.

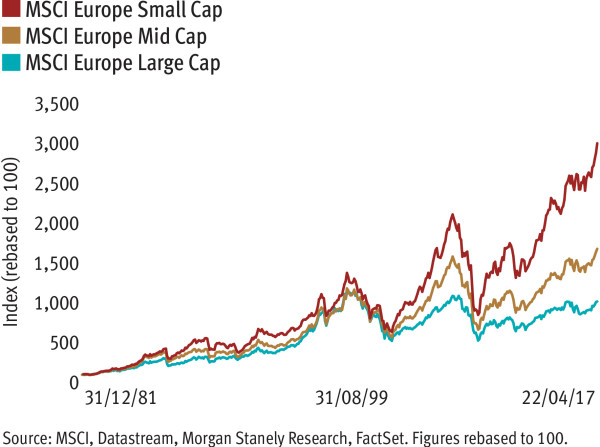

Is the size effect applicable to the European market? It appears so. From the end of December 1981 to the end of December 2016, the longest time frame for which we have data, the cumulative returns for small, mid and large caps are 2,711 per cent, 1,496 per cent and 881 per cent respectively.

It was surprising that there was a relatively narrow range of volatility, within 1 per cent, across the three groupings. Within the eurozone, smaller caps have even been slightly less volatile than large caps since the advent of the euro in 1999.

Small and mid (smid) caps differ from large cap in three ways: international exposure, specific risk and cyclical (interest rate) risk.

International exposure

European smid companies are more domestic oriented than large caps, but not by much: the top 300 largest companies in Europe have a 47 per cent international exposure compared with 41.6 per cent for smid caps.

In contrast, the US Smid Cap index, as represented by the Russell 2000, is about 84 per cent domestic oriented. This partially explains the fact that the sensitivity of European smid caps to domestic macro-economic factors is much less than US smid caps.

Because of their specialised and niche business models, smids carry a higher level of unsystematic risk or ‘specific business risk’. Specific risk can be diversified through a portfolio of different companies, but market risk cannot.

Cyclical risk

Smids have a slightly higher exposure to the cyclical segment of the economy, but only marginally. While they are more exposed to cyclical sectors, such as industrials or materials, their exposure to banks or energy companies is lower.

However, smid caps are probably still more sensitive to the interest rate cycle because of their higher than average leverage (debt burden) and reliance on bank credit.

Do active fund managers generally outperform?

An HSBC study conducted in 2013 concluded that eurozone smid-cap managers on average seemed to refute the efficient market hypothesis – which states that stock prices reflect all publicly available information.

Indeed, in the 2013 study we found that active eurozone smid-cap managers handily beat their respective indices in most periods. HSBC attributed this to the lower coverage of smids compared with large caps.

But in the past five years we have found that smid-cap managers are still beating their indices, but not to the same extent as before. Whatever the reason for this, the higher inefficiencies in the smid-cap market can create ample outperformance opportunities for the well-informed stockpicker.

European smids are often overlooked in an allocation to European equities. But the exact allocation depends on the individual investor.

History and common sense show that combining a meaningful level of smid caps with large caps serves to reduce overall risk and increase returns over time.

Meike Bliebenicht is senior product specialist in HSBC Global Asset Management’s multi-asset team