Invesco Perpetual’s fixed income team have said the lack of value in European high yield markets is causing “an issue” for investors searching for yield.

Head of fixed income products Lewis Aubrey-Johnson said rising prices for high-yield bonds across Europe had left yields looking little different to that offered by sterling investment-grade debt benefiting from Bank of England (BoE) bond buying.

Mr Aubrey-Johnson, who described an aggregate yield of around 3 per cent for both sectors of the market as unattractive, attributed the drop to a lack of issuance in the case of European junk bonds.

“One important consideration is the very modest levels of net supply,” he added. “Last year’s figure of E5bn could have been the lowest level since the financial crisis. When we think about the strength of demand for income, that’s a powerful support.”

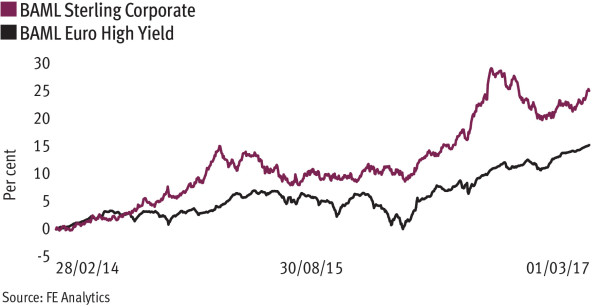

“In euro high yield you can see two distinct phases,” he said. “There was that bear market that lasted for much of 2015 and peaked at the start of last year with yields at 6 to 6.5 per cent. Since then it has been an almost uninterrupted and rigorous bull market.”

He noted that the fundamentals in the high-yield space, such as the number of defaults occurring among issuers, had not been “troubling”. But this, he claimed, left a paucity of opportunities.

“The issue we have got is where that leaves us in terms of yield,” he said. “This market yields barely 3 per cent. Just comparing one against the other, there’s hardly any difference in yield between sterling investment grade and euro high yield.”

As a result, value could only be found in selected cases, he said.

In the UK, Mr Aubrey-Johnson noted that corporate bond yields were low despite having widened against gilts, and saw little scope for a rise given the programme of corporate bond buying initiated by the BoE in September.

“With sterling investment grade, for much of 2015 yields were very stable and arguably spreads widened [later] as government bond yields were falling and corporates didn’t keep pace,” he said.

“The BoE programme was to purchase £10bn of credit over 18 months. We estimate they are nearly 80 per cent through that target already. It has been a very supportive backdrop for those markets.”

Much of the focus for the fixed interest team, which manages funds such as the £4.9bn Invesco Perpetual Corporate Bond and £500m Tactical Bond offerings, has remained on subordinated debt, where contingent convertible (CoCo) bonds offer yields of around 6 per cent.

“CoCos didn’t suffer really in 2015 but didn’t enjoy a bull market last year,” he said. “The yield premium is now quite large. It’s about 3 percentage points between CoCos and sterling investment grade.

“The majority of exposure across the desks is to legacy securities [issued by banks]. It’s a stamp collector’s market. They don’t really trade.”

IN NUMBERS

6.5%

Yield commonly received on euro high yield bonds as a bear market peaked in early 2016

300bps

Spread between aggregate yields of euro high yield and CoCo instruments now