Article 3 / 4

Investing in alternative assetsPlotting to secure highest quality credit return

Credit investors are being challenged to adapt their thinking in order to obtain reasonable returns while avoiding excessive risk in today’s hunt for yield. While some move down the risk spectrum, others add leverage to achieve their target returns.

Many resort to these approaches reluctantly, and struggle due to poorly structured mandates. In markets like these, investors can benefit from revisiting investment aims and challenging preconceptions.

Investors are familiar with a traditional two-dimensional return for risk graph. In credit, rating is often represented as the x-axis and credit spread as the y-axis. But simply moving along the x-axis to achieve a target return, or rescaling the y-axis by applying leverage, is suboptimal.

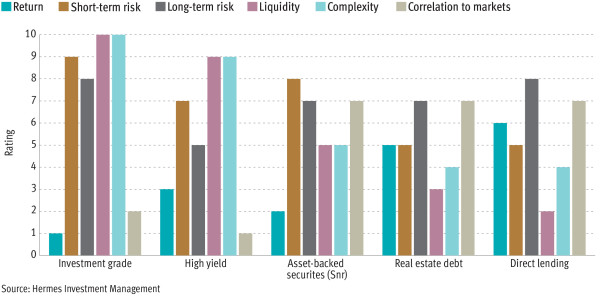

Credit assets have a number of other variables that should be mapped on different dimensions when seeking to achieve the highest quality returns. Dimensions investors often overlook include liquidity, complexity, correlation to markets, long-term risk (as opposed to volatility) and environmental, social and governance (ESG) factors.

Lower liquidity and the concept of illiquidity premium is often the first dimension examined by investors hungry for better value. Unfortunately, many still view liquidity as a binary factor, convincing themselves that liquid assets are perfectly liquid, or illiquid assets are illiquid and cannot be liquidated under any circumstances other than at maturity. This is patently not true within credit markets: liquidity is a spectrum and changes with time.

Asset-backed securities (ABS) exhibit an entire spectrum of liquidity within their asset class. Even the slightly more exotic ends of the ABS market display the characteristics of liquidity at times, but will be highly illiquid at others. Unfortunately, this gives rise to a situation where some investors include all ABS in the liquid bucket and others as illiquid, and therefore uninvestable. Neither approach gives rise to optimal decision making.

The second mistake is the perception that lower liquidity is equivalent to higher returns. We know that highly liquid assets are delivering lower returns than in recent history, but moving down the liquidity spectrum is no more certain to increase returns than moving down the risk curve.

We believe that liquidity is a parameter to be assessed in concert with others, and that a modest return from a less liquid strategy that has a significantly lower risk can be a compelling proposition.

The second non-traditional assessment parameter is complexity, which some investors feel they were burnt by in 2008. As a result, when combined with a lack of liquidity, complexity can be enough to make an investor dismiss an asset class.

If you were to look at a Venn diagram of credit markets, the overlap between complex and less liquid would be significant, but they are not equivalent. We believe this area is a rich seam for credit investors and that the alternative credit universe that sits in this overlap is one of the most attractive opportunity sets. Direct lending, real estate debt, infrastructure debt, peer-to-peer lending and asset-based lending are all areas worthy of further analysis.

Alternative credit does not fit into a classic fixed income assessment approach. It includes complexity, uncertain refinancing risk and currently tends to exhibit low liquidity. But on the flip side it can deliver high absolute returns, can be structured in a way that the risk of principal loss is very low, and may also display much lower correlation to broader markets.

Central bank activity, coupled with changes in regulatory treatment of some credit assets, has distorted markets, but so has the appetite of investors for vanilla products. Alternative credit assets and approaches to managing and lending can tap opportunities from distortions.

A focus on instrument selection, eschewing the barbell approach and incorporation of ESG factors have been drivers of success for those prepared to look beyond the traditional.

Returns over the next few years from credit assets are unlikely to match those over the past few years. However, those returns will undoubtedly be enhanced in absolute terms and in their quality by investors willing and able to look beyond the traditional confines, and to embrace the opportunities created by banks and insurers exiting their strongholds.

Andrew Jackson is head of fixed income at Hermes Investment Management