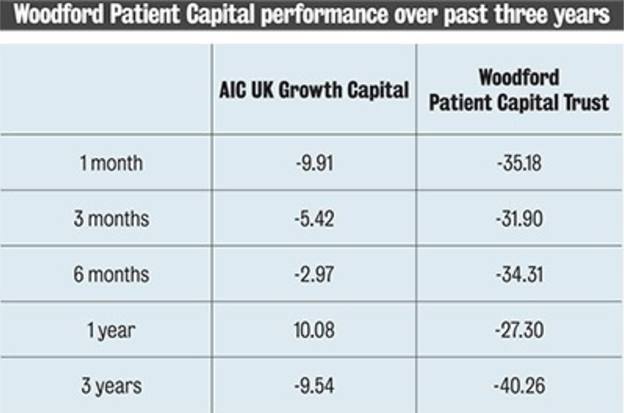

Following the Woodford Equity Income fund debacle, investors may be wondering where that leaves Neil Woodford’s investment trust – Patient Capital Trust – and whether the board will continue to back him.

As in any public company, the board of an investment trust is charged with managing the business of the company (for that is what it is) in the interests of shareholders. After all, the shareholders own the company.

The business of an investment trust is to manage a pot of money in much the same way as the business of Tesco is to run supermarkets.

They are both public, quoted companies with the same structure.

The difference is that the investment trust has a board and no employees.

The task of managing its assets is outsourced, for a fee, to a business that specialises in asset management.

The ‘interests of shareholders’ sounds simple, until you delve down into the what it actually means.

Is that the interest of shareholders in respect of their returns this year, next year or over the next five to 10 years? Such is the challenge facing any board.

The board will probably sensibly conclude the answer is future interests of shareholders – that is, the ongoing success of the company.

Changing a manager will only be considered if performance has been poor for some time.

If changing means taking a hit this year to improve the outlook the board may very well do that.

The challenge is gauging whether action today will produce a better outcome tomorrow. When an investment trust board is mulling changing the manager of its assets there will always be a cost to doing so.

This is what will be on their next board meeting agenda to decide on: is the inadequate performance of the current manager fixable?

We all know of times when we have lost faith in a manager, just in time for them to recover their mojo.

Improving performance with the same manager is much less costly and disruptive than moving the portfolio to another manager – they may even be amenable to reducing the management fee until it does improve. But here we have the problem with any outsourced service.

The bald truth is that if the assets of the fund are not being well-managed the board’s ability to tweak things is limited.

Usually it is a simple case of threatening to move the mandate to another manager – if that does not work, move it.

If the manager is a large asset management house there is some flexibility. It could decide to appoint, at the request of the board, a different team to run the assets. A small one does not have that same flexibility.

But investing history is littered with the carcasses of investment trust boards who avoided grasping the nettle for too long.

Eventually confidence evaporates, the discount to net assets builds and the fund is wound up.

What is the notice period for the current manager? This will often be a year.

So the fund will still be managed by an outgoing team for 12 months – not ideal – or the board will pay out the notice period and seek to move the money across to a new manager as soon as possible.

That will mean double management fees for a year, to be borne by the fund.

Likewise the current manager may administer any savings plan for the trust, which will also be on a notice period.

What is the shape of the fund? If there are big holdings the market will realise a manager change is in the pipeline and may bid down the stocks, assuming that the new manager will quickly want to sell holdings and construct a portfolio in line with the strategy they have mapped out to the board.

Might it be better to encourage the current manager to steadily adjust the holdings to a less risky configuration and then change the manager?

This may be desirable, but it requires a very co-operative manager and for the board to have nerves of steel since they are effectively micromanaging the expert they have appointed to run the assets.

What is the shortlist of prospective managers for the assets?

If the investment trust is in a specialist area the shortlist may be tiny.

And would they be able, or want to, take on the assets?

After all they may have their own agenda – offering direct to investors to merge the investment trust with their own listed vehicle perhaps.

For a big, generalist asset class – like UK equities – the list will be longer so there will be competition to run the assets.

But the best managers will know the value of their reputation and will negotiate fees and notice periods accordingly.

What do the big shareholders in the investment trust want?

The board should have at least a feel as to what the bigger holders of the trust are thinking.

If there is an activist shareholder on the register, the board will be aware that their time horizon may not be the same as the other shareholders.

We have found there are usually complications unique to each trust that need to be cleared before any decision is made.

When drawing up a shortlist of prospective new managers, the board must check carefully for conflicts of interest between their own directors who are also directors of one of the managers on the shortlist.

Key points

- Investment trust boards have to think of the interests of shareholders

- There are many failed investment trusts where the board has not dealt with issues in a timely manner

- Changing a manager can depend on the shape of the fund

This will also apply to any of the directors who are former directors of any of the managers.

Where a clear conflict exists, the conflicted party should not be permitted to vote on the change and the conflicted parties should recuse themselves from discussion and voting on the issue.

Lastly, the board will have to factor in the cost of changing the name of the trust if it currently carries the name of the manager (many do) or accepting that the trust will henceforth be managed by a different manager to what its name implies.

Nick Wilson is chairman of the Gulf Investment Fund