In January, to stimulate its economy, Japan adopted an unconventional negative interest-rate policy that penalized banks for hoarding too much money.

According to Nathan Gibbs, client portfolio manager for Japanese equities at Schroders, January's move to negative interest rates came as a shock, with a resultant downturn in the equity market performance.

He comments: "The move was a major surprise to equity investors. Although such aggressive easing should be supportive for equities, any positive effect was outweighed in the short-term by the continued appreciation of the currency and a general rise in global uncertainty."

Kwok Chern-Yeh, head of Japanese equities at Aberdeen Asset Management, concurs: "The idea, as with quantitative easing (QE) experiments everywhere, was to boost lending and raise inflation expectations.

"Instead, the Bank of Japan (Bank of Japan) move simply hurt banks as their lending spreads narrowed."

The yen went down and the stock market followed suit, precipitating the Bank of Japan into "policy back-pedalling" since, he adds.

Mr Gibbs adds that the Bank of Japan taking time to "fine tune" its policies over the year has been met with a "more conventional response within the equity market, with improved performance from financial-related sectors".

Recent moves

September's focus shifted from targeting just the monetary base towards targeting the yield curve.

This seems to be attempting to alleviate what Mr Gibbs calls the "previously unforeseen adverse implications of the negative interest rate policy".

The Bank of Japan capped 10-year government bond yields at 0 per cent, and offered to buy any bonds at that price.

According to contributors to this guide, this measure has been designed to steepen the yield curve and should support bank profitability.

But whether this will have any effect in the long-term is still a matter for debate, according to Ben Willis, head of research for Whitechurch Financial Consultants.

He says: "You could argue it has done little for the economy, but it certainly has provided a support to stock markets.

"Attempts to weaken the yen may not be working as planned but this has been designed to boost large-cap exporters.

"Much of the attraction of Japanese equities is they are relatively cheap on a valuation basis but corporate earnings are key if we are to see further recovery."

Moreover, it seems to have had little discernible effect on GDP growth; the latest data suggests no clear upward trajectory although it may again be too early to tell.

Biggest investor

One of the biggest investors in Japanese equities, of course, is the Japanese central bank, being one of the most active buyers through exchange-traded funds (ETFs), primarily through instruments that track the Nikkei 225.

According to Schroders' Mr Gibbs: "The current target of Y6trn in ETF purchases a year should provide significant support for the equity market.

"The main issue is whether this can be accomplished without creating significant distortions in the market as the ultimate outcome of this policy will be to leave the central bank as one of the largest holders of Japanese equities among all investor classes."

Aberdeen Asset Management's Mr Kwok says this ETF purchasing has resulted in "gaming of certain parts of the market", although this seems to be reversing slightly with the Bank of Japan starting to favour the Topix, which is a market-cap weighted index, unlike the Nikkei.

He adds: "Whether this action stabilises equities remains to be seen."

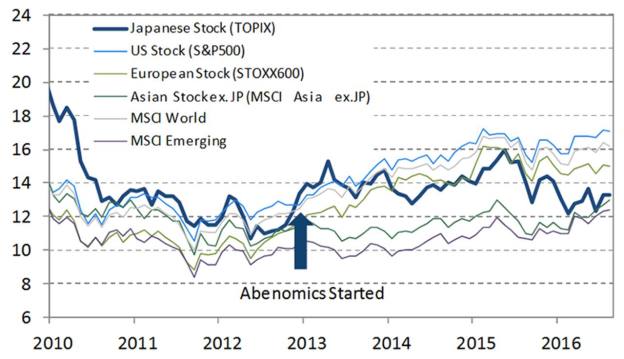

Data from Nikko Asset Management in October showed the Japanese market’s price-to-earnings (P/E) multiple is now close to its post-Abenomics low and is lagging that of other developed markets.

Abenomics refers to the economic policies advocated by Shinzo Abe since the December 2012 general election, which saw him elected for a second term as prime minister of Japan.

Abenomics is based upon "three arrows" of fiscal stimulus, monetary easing and structural reforms.

Current P/E multiples remain at approximately 13.5 times on a 12-month forward basis, compared to post-Abenomics highs of around 16 times in 2015.

Furthermore, the Bank of Japan's doubling of its annual ETF purchases to Y6trn, combined with an estimated Y6trn of share buybacks by firms will limit downside risk and set the stage for further expansion of P/E multiples, Nikko data has claimed.

But according to Katsunori Kitakura, strategist at SuMi Trust, although the Bank of Japan is attempting to "build momentum in the equity market" through the ETF purchases, this has "led to speculative trading and increased levels of rotation and volatility in the market".

He says this was most notable in the severe style shifts seen in August, when there was a shift from small to large cap, and growth to value outperformed.

"The Japanese market has experienced the effect 'wall of money' investing and this can move markets. However, this can regularly lead to mispricing of stocks, as fundamentals are ignored in purchases or sales of the broader market."

Uncertainty

Cyrique Bourbon, portfolio manager at Morningstar's Investment Management group, is not as impressed by 2016's fiscal policy.

He comments: "In light of the year-to-date underperformance, the Bank of Japan's efforts have accounted for little to nothing.

"This highlights a broader anti stimulus effect, where the lagging markets globally - UK, Europe and Japan - have been the ones announcing further quantative easing.

"The key will be whether investors have confidence in the long-term outlook for corporate cash flows and profits.

"The Bank of Japan continues to try hard but sadly 2016 has seen weaker global growth, an environment in which Japanese equities tend to lag. Add to this the fact the yen has strengthened - hurting Japanese exporters - and it's seemingly had the opposite effect to what the BoJ wanted."

For Nick Peters, multi-asset portfolio manager at Fidelity International, the effect of the Bank of Japan's monetary policy has been "something of a paradox".

"On the one hand", he says, "the market fell because investors lost conviction in the ability of Abenomics to reflate the economy. However, it would have been a lot worse if Bank of Japan policy had not been so loose.

"The looseness has held yen strength in check and played a preventative role in holding back bigger stock market falls this year."