Article 1 / 4

Guide to exchange-traded fundsHow the ETF market has grown

Before the US housing bubble burst, before Steve Jobs unveiled the iPhone, before the Bank of England bailed out Northern Rock – from the viewpoint of 2006 few predicted the enormous changes about to hit.

Few too, back then, would have forecast the phenomenal growth of what was at that time a product hardly known outside of institutional investors' circle.

But exchange traded funds (ETFs) and other exchange traded products (ETPs) have had a decade to reckon with.

Back in 2006, assets held globally in ETFs amounted to US$580bn, according to figures from research provider ETFGI.

Now they stand at a staggering US$3.2trn. Record inflows of US$389bn were gathered in 2016 alone.

“The focus of much of this growth has been the US market, which accounts for over 70 per cent of ETF assets globally,” James McManus, investment manager at robo-advice firm Nutmeg says.

“However, growth has been exceptionally strong in other markets too – assets invested in European ETFs have grown from $94bn in 2006 to $524bn today.”

In their simplest form, ETFs trade on a stock exchange like a stock, experiencing the same daily price fluctuations, and track the performance of a specific index or basket of assets.

They are a type of fund which owns the underlying assets (shares of stock, bonds, oil futures, gold bars, foreign currency, etc.) and divides ownership of those assets into shares, which investors then buy into.

So what is behind the explosion in demand for these types of investments?

“The growth of ETFs has been driven by a variety of factors,” Joe Parkin, head of UK wealth and retail sales at ETF house iShares, explains.

“Firstly, the types of investors that are using ETFs has widened. Traditionally ETFs were primarily used by institutional investors, but are increasingly a staple in retail investors’ portfolios.”

UK retail investors have been turned on to ETFs for three main reasons – their low cost, access to previously unobtainable investments and changes in regulation that made them more likely to be recommended by financial advisers.

ETFs give investors the chance to buy whole indices as easily as buying a share on the London Stock Exchange.

Eligible for inclusion in Isas but attracting no stamp duty, ETFs also have the lowest annual charges of all collective investment schemes.

Mark Fitzgerald, product manager at fund house Vanguard, which does a thriving business in ETFs, said the “extraordinary” birth and growth of the market has “been fuelled by investors becoming increasingly aware of the importance of lowering costs”.

Regulation

The Retail Distribution Review, introduced at the end of 2012, has also helped level the playing field for ETFs.

While prior to December 2012 other retail investment products saw a commission paid by the product provider to the recommending adviser, ETFs have never paid commissions.

Historically this made ETFs less attractive to UK retail financial advisers for obvious reasons – they were not being paid to recommend them.

“By banning commissions from fund issuers, RDR has changed the value proposition for independent financial advisers in the UK, moving from fund picking to deeper financial planning,” Mr Fitzgerald said.

Daniel Greenhough, investment manager at St Albans-based Lumin Wealth, says the use of ETFs is increasing among advisers like him, as well as discretionary fund managers, in part because more investment platforms have made ETFs available to trade.

In addition, ETFs are growing so rapidly because they offer investors an attractive and efficient way to implement both passive and active investment strategies.

“Investors are increasingly blending ETFs with active funds in their portfolios to best fit their investment objective,” Mr Parkin said.

“For example, ETFs can be used as the main component of an investor’s portfolio or a core satellite approach, whereby they allow an investor to tactically tilt their portfolio.

“When blending active funds with ETFs, investors often use an ETF when it can be difficult for an active manager to outperform the market, or to gain exposure to a market that is otherwise difficult to access.”

Mr Greenhough says he is seeing an increasing number of managed portfolio service providers launching passive only model portfolios for advisers to sell to clients.

Availability

The number of ETFs and ETPs on the market has certainly skyrocketed. In 2006 there were 888 different products availbel - at the end of December 2016, the Global ETF/ETP industry had 6,625 ETFs/ETPs, with 12,526 listings, from 290 providers listed on 65 exchanges in 53 countries.

On a practical basis, Mr Greenhough believes the amount of time spent on due diligence and ongoing monitoring is lower for ETFs than active managers. This is going to be attractive to a time pressured adviser.

He attributes part of the growing popularity of ETFs to marketing carried out in the US finding its way over here and influencing investors.

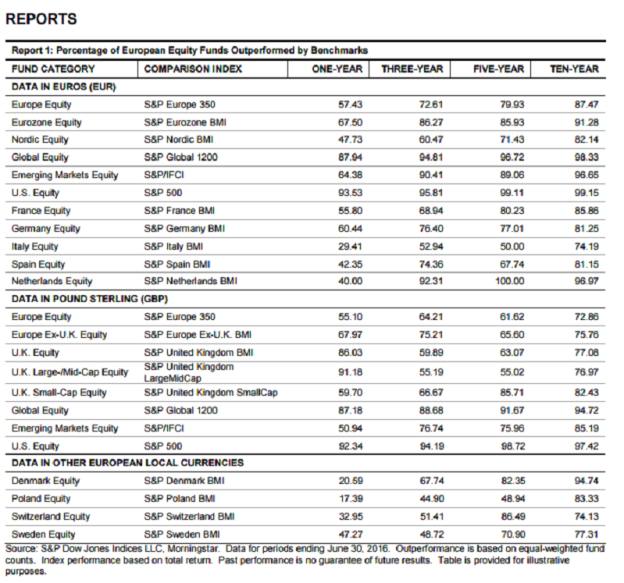

“The percentage of active funds outperforming the US market is generally lower over time than it is for managers trying to beat the UK market,” he says.

“Although it is not an assets under management weighted piece of research, the reports produced by S&P Dow Jones suggest over a five-year period only 1 per cent per cent of US fund managers outperformed, whereas in the UK 37 per cent outperformed (source: Mid-year 2016 SPIVA Europe Scorecard below).

Luis Rivera, CEO and co-founder of ETFmatic, a robo-adviser specialising in the funds, believes even the huge growth in ETFs over the last decade is “significantly slower than it’s about to grow”.

“Mobile Internet has changed the rules of the game and Europeans have finally got tired of being abused by banks and betting on fund managers that underperform. We have a lot of catching up to replicate distribution in the US market; among others in terms of investor education.”

laura.miller@ft.com