Reforms to dividend taxation announced in last week’s Budget may force advisers to restructure how they provide equity income strategies to wealthy clients as tax-free allowances are cut further.

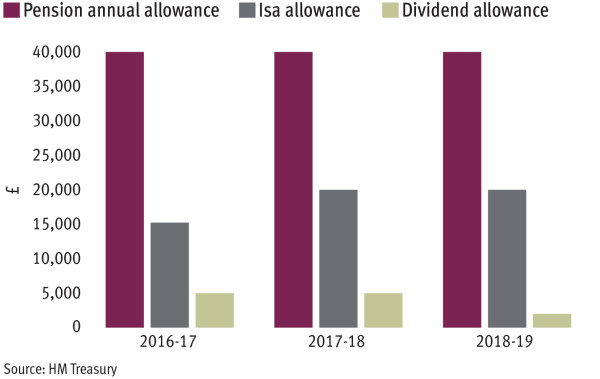

Chancellor Philip Hammond unveiled plans to cut the annual tax-free dividend allowance from £5,000 to £2,000, citing the aim of ensuring support for investors was “more effectively targeted”. The change is due to come into force next year, just three years after the £5,000 limit was first announced, and follows recent cuts to the pensions lifetime and annual allowances.

The change has been labelled a major headache for income investors, some of whom will have to shunt holdings into tax wrappers, pay a higher bill or, in more extreme cases, consider a lower-yielding investment approach to avoid breaching the £2,000 threshold.

The Treasury estimates some 2.3m individuals could be affected in the 12 months after the reform is introduced. Advisers have suggested there could be a scramble to prepare portfolios for the change.

Mike Horseman, managing director at advice firm Cockburn Lucas, said the onus was now on using the two tax years prior to the reduction to make portfolios as “tax-friendly and efficient as possible” in order to avoid any impact on either costs or investment strategy.

“It’s an area that requires input in the coming two years,” he said.

The Office for Budget Responsibility acknowledged last week that the government’s decision to “preannounce” its previous, more comprehensive package of dividend taxation reforms had cost the Treasury £800m in revenue as taxpayers reduced their prospective liabilities in the intervening nine-month period. “Ordinary investors are now vulnerable to paying much more tax on their dividends unless they use tax shelters to protect their income-producing funds and shares,” said Laith Khalaf, senior analyst at Hargreaves Lansdown.

While there is less room to manoeuvre on this occasion, those overseeing portfolios have some breathing space. A rising Isa allowance allows investors to shelter a larger amount, while transferring holdings to other vehicles such as Sipps could be an option.

Specialists have pointed to the so-called “bed and Isa” or “bed and Sipp” strategies, where investors sell holdings and immediately buy them back via a tax wrapper.

“Investors who own shares or equity funds outside of tax-free wrappers and who were not anticipating fully funding their Isa allowances with new cash should certainly explore reallocating these assets into a more tax-efficient environment through [this process],” said Tilney Group managing director Jason Hollands.

Those who have maximised pensions allowances and have more than £20,000 to invest in an Isa next year are more constricted. Mr Yearsley said that running an investment strategy to skirt below the £2,000 limit would not be ideal.

“Am I going to invest my portfolio in lower-paying things?” he said. “I don’t want to be making [investment] decisions based on tax reasons. You want to be making them based on investment reasons.”

Investors have also been warned not to rely on the fact that a portfolio generates less income than the current limit.

“It may yield that amount in future, or this government or the next may come back for another swipe at the dividend allowance,” said Mr Khalaf.

IN NUMBERS

7.5%

Dividend taxation rate above the £2,000 threshold for basic rate taxpayers

32.5%

Level for higher rate taxpayers

38.1%

For additional rate taxpayers