Article 3 / 5

The Guide: Multi-Asset InvestingHas multi-asset ‘gone back to the future’?

If an alien visiting from Mars picked up a copy of a financial newspaper, they would probably think multi-asset investing was where all the action was – given the column inches and headlines over the past few years.

Multi-asset investing has been around since the 1970s and started with the advent in defined benefit pension schemes of what is known as a ‘balanced’ or an ‘exempt’ fund. This was a product designed to deliver long-term capital growth for investors, with a lower level of volatility than the global equity market, by using primarily fixed income instruments and cash alongside equities to deliver a smoother return. It could be argued that this was ideal for pension investments in the 1970s and 1980s.

The balanced fund evolved into the distribution fund of the 1980s and 1990s: a vehicle that normally had a higher weighting to fixed income and perhaps some property to deliver a steady stream of distributions. As the industry moved through the noughties it saw the emergence and proliferation of fund of funds, which were still multi-asset funds but took their exposure through other, either fettered or unfettered, strategies. The industry also saw the emergence of what are now collectively called diversified growth funds.

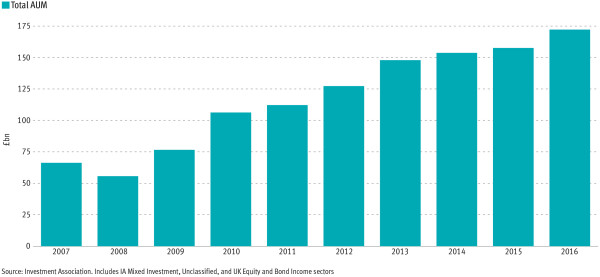

These offerings are directly invested but with much wider investment freedoms, and are used as the default funds in many defined contribution schemes.

The workplace pensions cap and the RDR have contributed significantly to the growth of multi-asset investing in the past five years, particularly the growth of risk-profiled or risk-targeted multi-asset investing and absolute return multi-asset investing.

There is a high chance the introduction of Mifid II will provide another headwind to the sale of fund of funds, irrespective of whether they are fettered or unfettered, unless you are a fund manager who has a vertically integrated business model. So have we in fact – as Marty McFly in the film – gone back to the future?

Investors today are able to get access to investment strategies that historically would have only been available to larger institutional investors. Surely this is a good outcome. Most multi-asset funds, being directly invested, are also able to achieve a total ongoing cost of ownership to the client of between 0.6 and 0.8 per cent a year, and this is only going to become more important after Mifid II.

Another point in need of consideration is the growth of absolute return investing since the financial crisis. This originally took the form of hedge funds but the need for liquidity from investors has led to a decline in hedge fund assets in favour of liquid alternatives – some of which are either single-asset or multi-asset.

Within this category the evolution of multi-asset funds has moved from their starting point of investing in just equities and bonds, to using a much wider range of tools and assets to achieve their objectives. In some cases this has led to funds becoming very difficult for the investor to understand – almost becoming too institutional.

However, we have also seen the emergence of relatively straightforward and simple products, such as multi-asset growth, multi-asset balanced and multi-asset income, which use non-traditional assets such as renewables, infrastructure or asset backed-securities to achieve the diversification they need and the outcomes investors want.

Looking at multi-asset investing today shows that, much like in the 1970s, the industry is still trying to deliver a one-stop solution for investors that meets their investing needs, matches their liabilities and provides a smooth return pre-, at- or post-retirement.

The only difference is that fund management teams are able to use a much broader range of assets to achieve these goals, and the institutional skill of multi-asset investing, which is already available to most of the population in a defined contribution pension scheme, is also available to advisers.

Add to this the more competitive total cost of ownership of a directly invested multi-asset fund and it is perhaps clear why they have become so popular among such a wide range of investors, and the trajectory looks like it is only going in one direction.

Fergus McCarthy is head of UK and Ireland intermediary distribution at BNY Mellon Investment Management