Article 3 / 4

How to build a robust yield into a portfolioHow sustainable are current yields in global economies?

The good times do not always roll, and while in 2011 bond fund managers were in a mini heyday, with plenty of liquidity, today is a different story.

Globally, there is a lack of liquidity, spreads are unattractive and even the higher-risk bonds which are offering better-looking yields may be carrying too much risk for too little cushion.

Even equity dividend income, the next port of call for investors who couldn’t find an embarrassment of inflation-busting yield in fixed income, is looking less appealing.

But the biggest question mark of all hangs over the interventionist policies of central banks and what effect, if any, their monetary policy will have on bond yields.

Nicholas Wall, manager of the Old Mutual Global Strategic Bond Fund, states: “We do not believe current yields are sustainable at these levels, with demand for government bonds falling and the net supply, after taking into account quantitative easing, set to rise considerably.

“On the supply side, most governments continue to run deficits and increase their bond issuance. This has largely been offset by central bank bond purchases but we are past the peak of quantitative easing, where central banks were price-insensitive buyers.

“We are now moving towards an environment where private sector investors will demand a higher real yield to fund government deficits.”

Considerations

The point about central bank involvement and its effect on the sustainability of yield is an important one for investors to consider.

Jonathan Baltora, portfolio manager for Axa Investment Managers, believes to perform an analysis to see how sustainable current yields are in major economies, one has to “distinguish between those economies that are still under the influence of quantitative easing and those where unconventional monetary policies are not being deployed any more”.

Mr Baltora believes that in the first group, which includes the euro area, it is “likely that normalisation of monetary policy poses an upside risk to interest rates”.

He explains: “This is typically the reason why the European Central Bank, which already started to slow down the pace of asset purchases at the end of 2016, is being reluctant to simply use the word ‘taper’ or ‘tapering’, by fear of igniting a bond sell off.

“The word ‘taper’ in [former Federal Reserve chairman] Ben Bernanke’s terms back in 2013 signalled the end of the increase of the Federal Reserve balance sheet and is now associated with ‘taper tantrum’ – one of the biggest bond crashes of the past few years.”

That’s what is happening with those economies which are still under the influence of QE. But what about those where such intervention is no longer being employed?

Mr Baltora adds: “In the second group, technical factors such as the monthly bond purchase from the central bank, are less relevant and economic conditions are likely to play a greater role.”

Here, he says, investors should look into details at both the real yields and inflation expectations. “Upside risks would materialise there, should real GDP growth accelerate, or realised inflation shift higher,” he says.

Mini-cycles and rising yields

Chris Leyland, deputy chief investment officer for True Potential, is a little gloomy about the prospects for the near term, as he thinks there is little sustainability in general across bond and equity income yields.

He explains: “Dividend cycles tend to be quite long and usually end with a recession. This aspect is not particularly great for holders of corporate debt either, as yields and spreads rise, causing capital losses.

“We are not forecasting an end to the dividend cycle in the next 12 months. However we do believe the threat to income sustainability has increased, for some investors who are not doing their homework on sustainability and liquidity.

“These investors are most at risk from mini-cycles, which are likely in some segments of the market. When investors chasing yield sense danger, they panic, try to exit quickly and thereby push prices down and yields up.”

Mr Baltora is clear there are upside risks to bond yields, as in most advanced economies, they remain below the current rate of core inflation. Moreover, he explains a strengthening economy will also pose an upside risk.

He adds: “Should real GDP growth accelerate, this would most likely lift real yields, and rising inflation would feed higher inflation expectations.”

Patrick Connolly, head of communications for Chase de Vere, agrees. He says: “In the medium term, it is possible yields will rise, particularly with regards to government bonds, some of which look very expensive.

“However, rising yields mean existing investors will suffer from capital losses and this will be a concern, as many people hold fixed interest to provide a greater degree of capital security in their portfolios alongside equities.”

Advisers therefore should keep on top of the bond allocation to make sure the income expectations of investors are being met where possible, without increasing the risk profile for the end client.

Pockets of problems

Fixed income managers are keeping their eyes on what central banks do.

Eugene Philalithis, portfolio manager for the Fidelity Multi-Asset Income Fund, is cautious over monetary policy decisions from major economies, for example.

He comments: “We should see continued upward pressure from the Federal Reserve tightening, but monetary policy globally might be a headwind to higher yields.

“If investors continue to see relatively low yields in Europe, then money will flow to higher-yielding markets.

“More widely, investors also need to watch whether China returns to being a deflationary force globally, which could act against the case for central bank tightening.”

Default risk

Many commentators said they were keeping a keen eye on the eurozone, where Italy’s banking system poses no small potential problem, while Greece is by no means sorted when it comes to debt levels.

Figures from Standard & Poor’s in 2016 show that, from 1915 to 2015, there were 189 country defaults and serious debt restructuring. Many of these countries – such as Argentina - are outside of Europe, which is reassuring, given this is a repeat offender. Moreover, some countries don’t exist any more, such as Yugoslavia.

But while these defaults would not have had so protracted an effect on other countries even 60 years ago, today’s increasingly globalised and intertwined economies means this becomes more of a global problem.

Add to this the fact one small country default in the eurozone now will have a significant impact on the rest of Europe as well as the UK and the US, and the situation becomes even more precarious.

Moreover, higher levels of indebtedness at a corporate level, as borrowing has been so cheap over the past decade, could indicate a higher risk of corporate defaults.

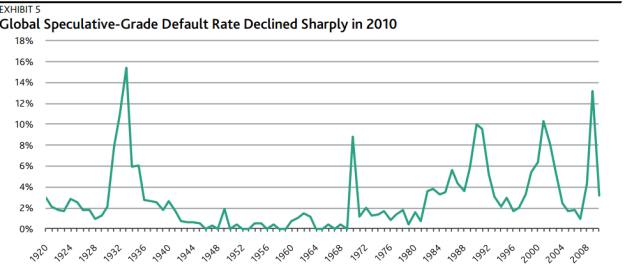

This was seen in great clarity during the recent financial crisis. According to research from ratings agency Moody’s, global corporate defaults had been low, spiking during the Great Depression, the early 1970s at the height of the oil crisis, Black Monday, the Tech Bust, and then spiking again in 2008-2009.

After 2010, defaults have subsided. According to Moody's 61-page research paper, Corporate Default and Recovery Rates 1920-2010, only 57 Moody’s-rated corporate issuers defaulted on a total of $39.1bn of debt in 2010.

By comparison, 265 companies defaulted on a total of $330bn of debt in 2009, with 103 defaults registered in 2008, affecting $280.9bn of debt.

Figures remained low for several years, but then in 2016, fellow ratings agency Standard & Poor’s reported a sharp rise again in corporate defaults.

According to S&P, there were 150 firms defaulting globally. This was a 40 per cent rise on 2015, making 2016 the worst year for corporate stress since the height of the global financial crisis.

Will there be any more exogenous or intrinsic shocks to the market, pushing more companies and even countries to the brink of default – and over? That’s a question for a medium, not a fund manager.

According to Dan Ivascyn and Alfred Murata, managers of the Pimco Income Fund, the fixed income manager’s job is to: “target an attractive distribution and a positive real return” for clients.

Duration risk

Then there is duration: inflation is already threatening to erode returns in the UK, with forecasts of 3 per cent CPI by the end of 2017. This way outstrips the 0.1 per cent yield available on a two-year UK gilt (as at 5 June).

But also compare this with the yield on a 10-year UK gilt of 1.05 per cent – is it worth holding such bonds for any length of time given the propensity of the yield to be eaten away by inflation? And what happens when interest rates rise over time?

Just because the bank base rate has been at a record low in the UK since 2009, the days of 15 per cent interest rates, as seen in the early 1990s, is still etched into many investors’ memories.

Mr Leyland observes: “We have worked diligently with our manager partners to ensure they are comfortable with taking credit risk and managing duration to restrict sensitivity to changes in the general level of interest rates across the funds and models.”

This is one reason why maintaining a short duration on part, or even all, of a portfolio is helpful if the client’s main concern is to have a steady income stream in the near future that is outstripping the pace of inflation.

Stable, not stunning

For many fixed income managers and advisers managing portfolios for clients, bond yield is not about shooting the lights out or aiming for a stunning yield, but about sustainability, given all the various concerns.

Mr Leyland says: “Our partners are not reaching up [the risk curve] for yield and, in fact, we have seen model portfolio yields decline slightly as a result of deliberately pursuing a sustainable income strategy.

“We believe this is the right mix between having a level of yield that is attractive for income investors and the ability to deliver income sustainably.”

Chris Iggo, chief investment officer for AXA Investment Managers, says: “In times like today, when yields are low and volatility is low, it is perhaps important to remind oneself that income cannot be created out of nothing, and strategies that promise higher levels of income necessarily need to take more risk.

“That said, in the long-term it is just as important to focus on avoiding the big losses than making the higher return.”

simoney.kyriakou@ft.com