Article 4 / 4

The Guide: Fixed IncomeTake a broad view when investing in bonds

Fixed income continues to be an interesting and challenging asset class. While two key areas of focus are often government and corporate bonds, more esoteric areas of the bond world could be offering fruit ripe for the picking.

Many in the industry have begun looking for less conventional opportunities. Investors can no longer solely rely on income to find a meaningful return on developed market government bonds, given the current prolonged low-yield environment. Capital appreciation has become the larger driver of returns compared with what has historically been the norm.

As a result, investors now need to be more flexible than ever when dealing with government debt, in particular due to a recent global synchronised upswing in growth and inflation. It appears central banks may be realising the limits of their unconventional monetary policies and are looking to normalise their balance sheets.

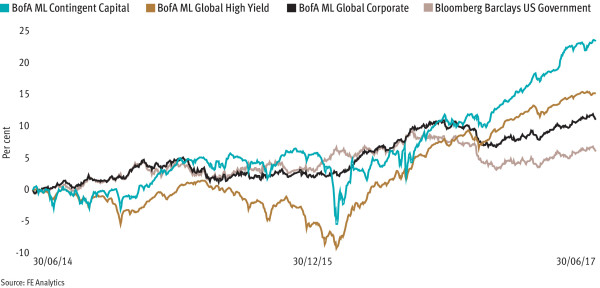

A good example of this trend can be seen in the US, where 10-year government bonds yields have traded up from 1.8 per cent to a high of 2.6 per cent since the election of Donald Trump. They are now trading at 2.2 per cent as markets grapple with the reality of whether the president can enact his long-promised populist attempts to increase growth and inflation, against a backdrop of the US Federal Reserve increasing short-term interest rates. In this environment, continual screening of the global fixed income market may well remain of upmost importance.

But with the uncertain backdrop and lower income within the government bond space, there are arguably areas of the corporate bond market where there is a much clearer path in terms of allocating capital. Debt issued by banks and insurance companies could be viewed as compelling from both a potential income and capital appreciation perspective supported by a number of fundamental tailwinds.

First, central banks are increasingly acknowledging that a zero per cent interest rate monetary policy is bad for bank earnings, which in turn has negatively affected lending and economic growth via decreased impulse in the money multiplier across credit-based economies. This further complicates the immediate outlook for rates, but over the longer term this attitude by central bankers could help ensure that banks enjoy the benefit of a gradually steepening yield curve.

Second, the regulatory trajectory seems to be changing to become advantageous for financials. Capital requirements are being relaxed, and insolvency laws are being harmonised across Europe. The restructuring of the banking sectors of Italy and Portugal, in particular, is nearing completion, potentially leading to greater systematic resilience across the whole European banking sector. Meanwhile, some big litigation uncertainties – notably at RBS and Deutsche Bank – are in the process of being resolved, which again may provide a positive for the sector.

Third, banks have made notable progress in building capital over the past 12 months, with many approaching their targets for additional tier 1 and tier 2 securities holdings. While such bonds have proved popular with investors, a dwindling supply could drive returns.

Some also maintain that positive technicals re-enforce this: positioning in financial credits appears clean relative to both high-yield and government issues. It could be that lacklustre recent returns, combined with the heightened complexity of the space, have flushed out many of the more fickle holders. The ground is potentially well prepared for the sector to return to favour among sophisticated investors.

This year has seen bank debt outstrip high-yield returns in both Europe and the US, up 8.4 per cent year to date, versus 3.9 and 4.8 per cent respectively. Given all of these drivers, there is potential for this to continue.

However, the importance of credit selection is becoming increasingly important given the high level of idiosyncratic risk. As we have seen recently in Spain, bail-ins are a very real threat. Equally, on the positive side individual issues are increasingly benefiting from being called by banks during capital stack restructurings. This offered investors returns quite separate from underlying fundamentals.

For those willing and able to enter the space, the mooted rewards could be worthwhile.

Jon Mawby is a portfolio manager at Man GLG