How times have changed.

Since the referendum, the UK’s currency has fallen dramatically, hitting a 31-year low against the US dollar at one point last year.

There is little sign of it picking up in value, so long as uncertainty surrounding the negotiations for the UK’s departure remains.

The implications of the fall in sterling could be quite far reaching.

Léon Cornelissen, chief economist at Robeco Investment Solutions, says: “Sterling has always steadfastly remained outside the EU’s auspices after the UK’s repeated refusal to join the euro.

“Pro-Brexit commentators had long mocked the euro as being susceptible to the long-running economic sagas of the eurozone, leading to bailouts for Greece and the largest European quantitative easing program in history. Some doubted whether the euro would even survive.”

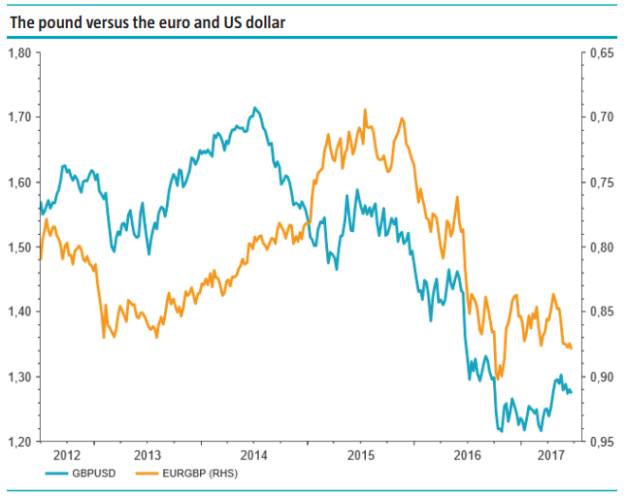

Figure 1: The pound versus the euro and US dollar

Source: Robeco Investment Solutions/Thomson Reuters Datastream

But he observes: “Now, the boot is firmly on the other foot.

“After the Brexit referendum the pound weakened about 12 per cent vis-à-vis the euro and the US dollar, as investors concluded that leaving the largest internal market in the world would probably be a structural headwind for the UK economy.

"The pound fell another 1.5 per cent after the Conservatives failed to win an overall majority in the 2017 snap election and is seen weakening further in the absence of a trade deal to replace membership of the single market.”

Inflation looming large

Some of the biggest beneficiaries of this decline in the pound have been companies which export their goods or services, and this is why the FTSE 100 has received such a boost in the aftermath of the referendum.

The majority of businesses in the index generate a significant amount of their revenues overseas, and as a result have been able to take advantage of sterling’s drop.

However, imports into the UK are being hit and this is feeding through into higher costs for many food items, for example.

Higher food and fuel prices mean a higher rate of inflation, which hit 2.9 per cent in May, only to come back down to 2.6 per cent in June.

As Mr Cornelissen points out: “Real incomes are now declining, as British workers are not compensated for the rise in inflation with pay rises, due to companies remaining cautious amid the increased economic uncertainty.

“This has also been true of public sector workers, who have also been declined pay rises that mirror rising inflation, as the government reins in its spending.”

In other words, spending power is being eroded and not that slowly either.

While some feel this could help the UK’s balance of trade, Will Hobbs, head of investment strategy at Barclays Wealth and Investments, is not convinced.

“The reality is that the elasticity of demand of domestic consumers for imports, and of foreign consumer of British exports is quite low. Historically, the quantity of imports or exports consumed has changed little in periods of sterling weakness,” he suggests.

“The devaluation will help the UK’s net external investment position, with the UK having more foreign currency assets than liabilities. However, this will be of scant consolation to UK consumers while they try and digest this admittedly transitory bout of imported inflationary pressure armed only with stagnant wages and a regulator just starting to sound a little more cautious on the credit outlook.”

While consumers earned a slight reprieve in June as inflation dropped to 2.6 per cent, there are many who still think inflation has the potential to hit 3 per cent in 2017.

Wouter Sturkenboom, senior investment strategist at Russell Investments, is working on the assumption the UK economy will continue to slow down “as the pain from higher inflation and slower wage growth lowers the living standards of the UK consumer, hitherto the engine of economic growth”.

He adds: “This will continue as inflation rises to 3 per cent in 2017 and could accelerate if unemployment creeps higher due to a slowdown in business investment and housing construction.”

With inflation having reared its head again, all eyes have been on the Bank of England as one way to curtail the rate of inflation could be to hike interest rates.

At the last Monetary Policy Committee (MPC) meeting in June, three members voted for a rate rise.

Complicated picture

But complicating the picture is the spectre of Brexit, as Ed Hutchings, UK sovereign portfolio manager at Aviva Investors, points out.

“[Mark] Carney has highlighted the transitory nature of inflation on numerous occasions. The sharp rise in inflation over the last year is mainly a result of the depreciation of sterling following the EU referendum and much of the impact has now fed through,” he explains.

“Nevertheless, in its latest inflation report, the Bank said the fall in sterling is likely to keep inflation above its 2 per cent target throughout the next three years, which arguably gives the MPC grounds for a more hawkish stance.”

Mr Hutchings warns: “However, given the uncertainty around the UK’s economic prospects, it is difficult to argue for a rise in interest rates. Such a move might precipitate weaker consumer spending at a time of great uncertainty.

“There is no clear visibility as to what the UK’s exit deal from the European Union will look like two years hence.”

He adds: “If it were to raise rates, the Bank is unlikely to embark on a major hiking cycle. Such a move could hit the consumer and the economy quite hard, especially as lenders are already tightening credit criteria or restricting loans under pressure from the Bank itself.”

There is no sign the pound will rebound dramatically in the coming months, as the negotiations rumble on with very little indication of the outcome for either side at this stage.

Vinay Sharma, senior trader at ayondo markets, predicts sterling will only move lower as the negotiations over the terms of the UK’s departure develop.

“However, as is typically the case, it may take longer than the two-year negotiation period, and eventually there will be an agreement of sorts that appeases everyone,” Mr Sharma suggests. “Therefore eventually sterling will recover.

“I would imagine that spending power for Brits will remain depressed for many years to come as I envisage it will take many, many years before we get to pre-Brexit levels for sterling.”

eleanor.duncan@ft.com