Investors can be lulled into a false sense of security with income-generating investments.

Because they are seeking dividends from longer-term, lower-turnover stocks and funds, rather than aggressively seeking to cream the rewards of high-growth strategies, investors can become complacent that the dividend payments will always come in.

Unfortunately, this is not the case. Moreover, the way in which portfolios are composed can sometimes lead people astray in thinking their portfolio is well-balanced and the income streams are spread out, but in fact there is a high correlation or asset risk.

Moreover, some funds may be focused more on capital protection rather than on maintaining a sustainable dividend, while others may be focused on income generation regardless of capital erosion.

These risks may not always be immediately evident when first assessing a fund's suitability for a particular client.

Knowledge is power

For the end user, making sure the investment strategy is the right fit for the client's income needs is of paramount importance.

Patrick Norwood, insight analyst for Defaqto, comments: "It is vital for clients and advisers to know what type of income fund they are investing in."

Mr Norwood says: "Some funds will seek to preserve the capital value of the fund as much as possible, at the expense of income, while others will do the opposite, namely aim for a high income but with the likelihood that the capital will run down sooner. Many funds will be somewhere in between these two extremes."

While fund managers and investment advisers, however, will understand what the income/capital trade-off might be in an income-generating portfolio, communicating this to the client can be more difficult.

Indeed, trying to explain that volatility, while a risk to a portfolio, is not always a bad thing, can be difficult enough in and of itself. After all, there are so many things to consider, including:

- Political risk.

- Market risk.

- Credit risk.

- Currency risk.

- Interest rate risk.

- Inflation.

- Liquidity.

- Sector-specific risks.

- Reputational risk.

Tim Morris, IFA for Russell & Co Financial Advisers, says: "Fund managers provide data on volatility – including standard deviation and the Sharpe Ratio.

"These are useful for advisers, yet mean little to the average client. Robust risk profiling is an integral part of finding the right strategy. This must be presented in a format which clients understand."

Risk categories

There are many agencies, such as Diminimis, Distribution Technology, Finametrica and others which provide some form of risk profiling tools, which can help advisers and their clients narrow down their attitude and financial tolerance for risk.

This can help the adviser narrow the range of appropriate and suitable investments for that particular client within the risk profile the client and adviser have selected together (or self-selected, if the client is provided with an online questionnaire before the initial meeting as part of the fact-find).

To help advisers narrow down the field, individual funds and multi-asset portfolios often come with risk and suitability ratings by agencies that can help the adviser make a more tailored decision about the suitability of the multi-asset fund (or the discretionary fund manager to whom the investment decisions are outsourced).

These can also help advisers assess whether the initial client portfolio construction, suitability of portfolio selection and suitability of transactions to portfolio mandate will be the right fit for the client.

For example, Defaqto has introduced suitability ratings for income funds, which puts the fund into one of four different risk categories based on the income versus capital volatility trade-off.

Such tools, although not the be-all-and-end-all to an adviser, can also assist in the ongoing assessment of portfolio risk and suitability, as markets' and clients' financial situations change.

Challenges

For Mr Morris, the way in which the investment world seems to be moving can present a challenge for advisers when trying to mitigate risk and maintain a well-balanced, diversified and risk-appropriate multi-asset portfolio.

He explains that, as people have been chasing income for many years - even more so perhaps since the 2008 financial crisis - spreads on fixed income have narrowed and dividend growth in equities has become tougher to find, as everyone is hunting in the same grounds.

He says: "Increased correlation of equities and bonds is a concern."

Correlation is indeed a concern. According to Rathbones' multi-asset team, maintaining a focus on correlation is important for a fund manager when it comes to portfolio construction and management, as well as for an adviser keeping watch to ensure ongoing suitability.

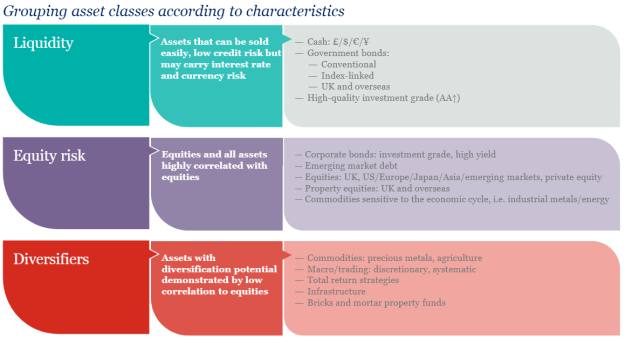

The below graphic illustrates some of the risks inherent in each of the main asset classes within a multi-asset portfolio, which need to be managed accordingly.

Source: Rathbones

Discussing risk

While understanding all these risks and mitigating these can be a challenge, Bob Szechenyi, investment director for Rathbones, says it can be done - and the key to manage these is by really knowing your client.

He says: "This can be achieved through a combination of qualitative and quantitative approaches.

"Ultimately it is about knowing your client, understanding their overall circumstances and their life goals, through discussions, risk questionnaires and risk profiling, in order to ascertain that the strategy and risk tolerance are the right fit."

Joe Roxborough, chartered financial planner for Ascot Lloyd, agrees, but cautions the conversation has to be clear for the client to understand.

"The very first step in discussing risk", he says, "is to operate with a shared language that both parties understand.

"I see a lot of discussion about cautious, balanced, growth and adventurous models, but in most circumstances these are loosely, if at all, defined."

This is because words mean different things to different people, particularly to those who do not have an in-depth understanding of the terms by which financial services professionals refer to things.

Mr Roxborough adds: "First and foremost, I would start with an example benchmark portfolio, examine the holdings and consider the volatility, past performance and potential risks of a portfolio."

Ascot Lloyd uses Distribution Technology's attitude to risk assessment, so the client can compare their thoughts and opinions to others with similar attitudes, and see how their personal portfolio compares with the model suggested.

"In terms of speaking with my clients, I prefer to think of volatility and capital risks as the main components here," he says.

simoney.kyriakou@ft.com