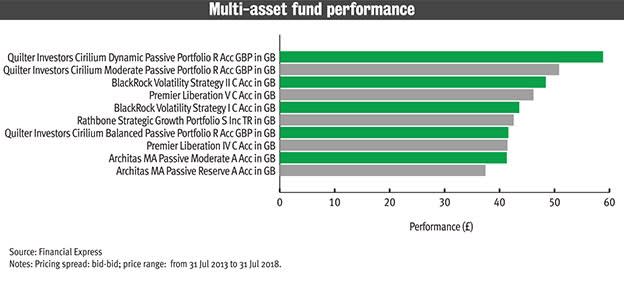

Is multi-asset investing the best approach for clients' portfolios?

- To understand the differences between multi-asset and multi-manager

- To learn about the investing principles behind the different of fund

- To grasp why one might have advantages over the other

- To understand the differences between multi-asset and multi-manager

- To learn about the investing principles behind the different of fund

- To grasp why one might have advantages over the other

Multi-asset or multi-manager: which is better? Two experienced fund managers go head-to-head as advocates of their particular portfolio management path

In favour of multi-asset investing: David Coombs, head of multi-asset investments at Rathbone Unit Trust Management

I have played both ends of this wicket. We switched the Rathbone Multi-Asset Portfolios from multi-manager to a direct, multi-asset approach in October 2015 because we believed it was no longer the optimal way to run our funds.

I started my career – too many decades ago – as a multi-asset manager, helping to build diversified portfolios by buying individual stocks and bonds. It was only in the early 2000s, while at Barings, that I was asked to manage a newly launched multi-manager fund. They were extremely popular at the time.

It would be wrong to say that multi-manager is a flawed approach. However, people are questioning its effectiveness today because it’s difficult for these funds to survive and thrive in a painfully cost-conscious world.

These funds labour under layers of cost: they have to pay all the management charges and trading costs of their holdings and then levy another round of the same charges on their unit-holders.

All advisers now come equipped with standard-issue magnifying glasses on lanyards round their necks, all the better to suss out costs (and rightly so).

Structurally lower expected returns just compounds this imperative: costs come straight off bottom-line performance for clients after all.

That is not to say that some multi-managers do not add value though. The larger brands with long and strong performance probably have the clout to push for lower fees and they definitely still command a loyal following of both advisers and DIY investors. But I imagine it is harder to drum up new business than it is to hold onto what they already have.

Cost was not the reason why we switched tack to using direct securities within the Rathbone portfolios, however. Sure, it was a bonus, and part of the reason why our ongoing charges (OCFs) are now significantly lower.

Different funds, different techniques

You see there are several types of multi-manager funds – not all use the same technique. Some buy a blend of managers across relatively fixed regional weights to reduce risk. They essentially pick managers the way a bottom-up equity fund manager would pick stocks.

Rathbones took a different approach in that we were more active in how we allocated our portfolio between asset classes and regions and style. For example, suppose we liked the prospects for the US and believed growth would outperform value stocks. We would then buy one or two managers to run that exposure for us. This tended to result in a more high-conviction, focused strategy than the blended approach. This worked well for us, but there were problems that cropped up every now and then.

Sometimes our views on markets and those of the managers we used would diverge over time. This was uncomfortable and meant having to find a replacement. Not being close enough to the coalface was also frustrating – you are a step removed from the underlying companies which makes it harder to fully understand all the risks you are taking.

By 2015, our internal research team had grown to the point where I believed we could move to direct investing: analysing and buying the underlying assets ourselves. So I went back to multi-asset investing.