Investors believe the direction of the stock market may warrant becoming more cautious.

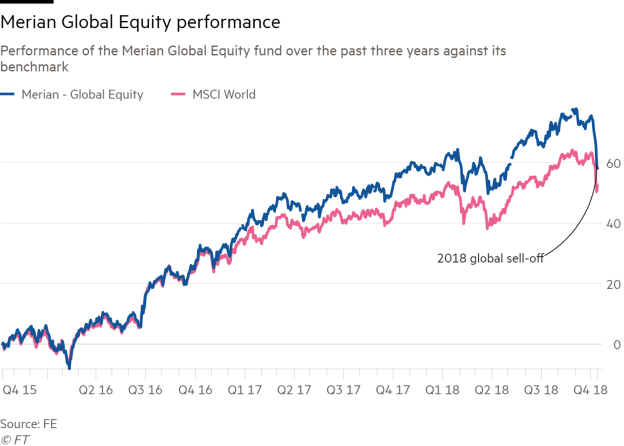

Ian Heslop, who runs the £986m Merian Investors Global Equity fund and the £2.8bn Merian North American Equity fund, said he has been "more defensive" about the US equities he has been buying.

He said the normal cycle of markets was for a small number of stocks to display strong growth as economies exit recession, and so enjoy strong share price gains. This is the period when the growth style of investing performs best.

The second phase is for economic growth to become more widespread, more companies show growth, and valuation becomes more important, meaning this is the time when the value investing style does best.

The final phase happens when economic growth slows and many companies stop growing.

Mr Heslop said US interest rate rises, concerns about the health of emerging markets and other geopolitical uncertainty meant markets may skip the value stage and move straight to caution. But he said in 2002 the end of the boom in tech shares led to a period of intense volatility before the value style of investing asserted itself.

He said if the downturn in stock market performance proved persistent the shares of insurance companies would be likely to perform well, but if the market began to reflect the level of economic growth, banks would be expected to perform well.

Mr Heslop said that the growth style of investing has dominated in recent years with the growth of the large, mostly American, technology stock. He said even when economic growth became more widespread, this was not reflected in the stock market and the same large cap technology shares outperformed the rest of the market.

He said this "decoupling" of the performance of the stock market from the performance of the global economy is the result of the unconventional monetary policy of recent years, particularly of low interest rates and quantitative easing.

Because those policies kept interest rates low, they tended to boost the growth style of investing because they keep bond yields low and since growth companies tend to pay lower dividends than the market, lower bond yields make those shares more attractive.

Bryn Jones, head of fixed income at Rathbones said he had owned inflation-linked bonds in anticipation of bond yields rising.

Expectations of higher interest rates in the US have caused bond yields to rise, which precipitated the recent market volatility, and Mr Jones has responded by selling his inflation-linked bonds, and has bought UK government bonds instead.

He said the reason for this is that the yield on regular UK government bonds had risen sufficiently that the gap in yield between the inflation linked and non inflation-linked bonds has narrowed to the point where he didn't view inflation-linked bonds as a good investment.

Meanwhile Alec Cutler, who runs the £36m Orbis Global Balanced fund, said he continued to avoid owning bonds, which he said were "not even close to cheap".

He was very wary of investing in European equities. Mr Cutler said: "Even with the tailwind of global growth improving and very low interest rates around the world, the European economies and stock markets have not performed well, so the question for investors must be how well European equities can perform when interest rates are rising and the outlook for global growth is weaker."

Ben Seager-Scott, chief investment strategist at wealth manager Tilney, said: "I’ve been talking quite a bit on this with clients and internal staff over the last few days – we’re fundamental investors, and the fundamentals have not changed significantly so if anything this could be an attractive entry opportunity for those investors who have been waiting with cash on the sidelines.

"Although there are some signs of cooling economic momentum, fundamentals are still supportive if you look at company earnings growth expectations, and there are no signs yet of inflation getting out of control.

"Markets mostly seem to have been spooked, but I don’t see any fundamental reason to change asset allocation though there may be some tactical opportunities to take advantage of cheaper valuations.

"We also recently started to take a little profit on the US which is looking complacent, but that’s largely been rebalanced within other equity regions especially the UK."

david.thorpe@ft.com