But while it is hard to see the tit-for-tat trade dispute receding anytime soon, it is important to look at how the dispute relates to the US electoral cycle and President Donald Trump’s image as ‘dealmaker’, as well as the longer-term impacts of this dispute on China, which are often overstated.

US politics and tariff decision making

The US electoral cycle remains a key point of reference for the direction of the trade wars story. With the US midterm elections edging closer and Republican control of both houses of Congress at stake, it is hardly surprising that Mr Trump wants to portray the image of being tough on trade, just as he promised in his campaign.

As such, it is likely that this rhetoric will continue to escalate at least until November, and if his party is successful, then trade wars are likely here to stay.

But the outcome of the midterms will also affect the decision-making processes of China and other US trade partners – will they negotiate, retaliate, or put off these decisions until the presidential elections in 2020?

Trump as ‘dealmaker’

However accurate it may be in reality, Mr Trump sees himself as a ‘dealmaker’, so is there the possibility that his ultimate goal is to strike a historic ‘deal’ with China?

After years of rhetoric directed towards the US’ North American Free Trade Agreement partners, Canada and Mexico, Mr Trump forced both parties to the table to renegotiate the 1994 agreement.

While the verdict is still out on how much Mr Trump really achieved here, he took great pleasure in announcing this ‘truly historic’ new deal, evidencing how his tough talk ultimately leads to deal making.

In comparison to China, however, Canada and Mexico are far more reliant on US trade – exports to the US contribute more than 20 per cent to Canada’s GDP and 37 per cent to Mexico’s GDP – and as a result, they are much more likely to be responsive to US demands.

This begs the question, is a ‘winning deal’ with China even possible?

China has been effective at diversifying its trading partners through its Belt and Road Initiative, and Made in China 2025 is working towards achieving dominance in high-tech manufacturing, making it less reliant on foreign – and indeed US – technology.

With these long-term strategic plans making progress, it is unlikely that Mr Trump even has the bargaining power he may have had over China 20 years ago, and as a result the likelihood of a ‘winning deal’ appears less likely.

Staying positive on China

It must be noted that while GDP in China is slowing, this has been driven largely by segments of the economy specifically targeted by the government’s deleveraging efforts, such as infrastructure fixed asset investments.

But on the positive side, private sector manufacturing is increasing, driven by the party’s determination to ensure sufficient funding for small and micro enterprises, which will continue to be a key focus for growth moving forward.

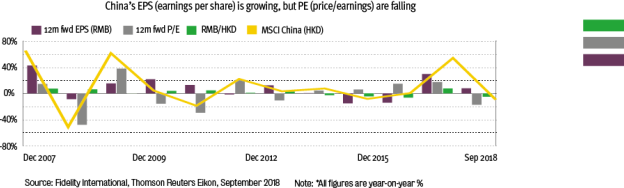

The trade wars have driven weakness in Chinese equities, particularly in sectors most exposed to US trade, but to put this in context, less than 5 per cent of the MSCI China Index revenue share comes from the US, and we believe there is a case to be more constructive on China.

The return on equity growth rate in China is one of the best in Asia and is supported by structural tailwinds: better margins driven by factors such as improving domestic consumption, cost reduction trends, and consolidation in state owned enterprises.

In addition, after a nearly 25 per cent drop in Chinese equities since January, the price to earnings ratio is now below its long-term average, and we believe this represents an attractive entry point for investors looking to get back into the market.

George Efstathopoulos is a portfolio manager at Fidelity International