Hargreaves Lansdown's role in the Woodford saga could lead to further scrutiny of its services by the Financial Ombudsman Service, experts have suggested, particularly if consumers feel they have been misled by the wording on its website.

The platform featured the Woodford Equity Income fund on its buylist until the point at which it was suspended on June 3. The subsequent decision to wind-up the fund, made earlier this month, is expected to crystallise losses for investors.

Around 30 complaints about Woodford IM have already landed at the Fos. The number of complaints made about Hargreaves in relation to Woodford is unclear.

Paul Resnik, director of risk planning firm PlanPlus, claimed the wording used by Hargreaves to describe its fund selection process seemed “similar to that of advice” to the untrained eye.

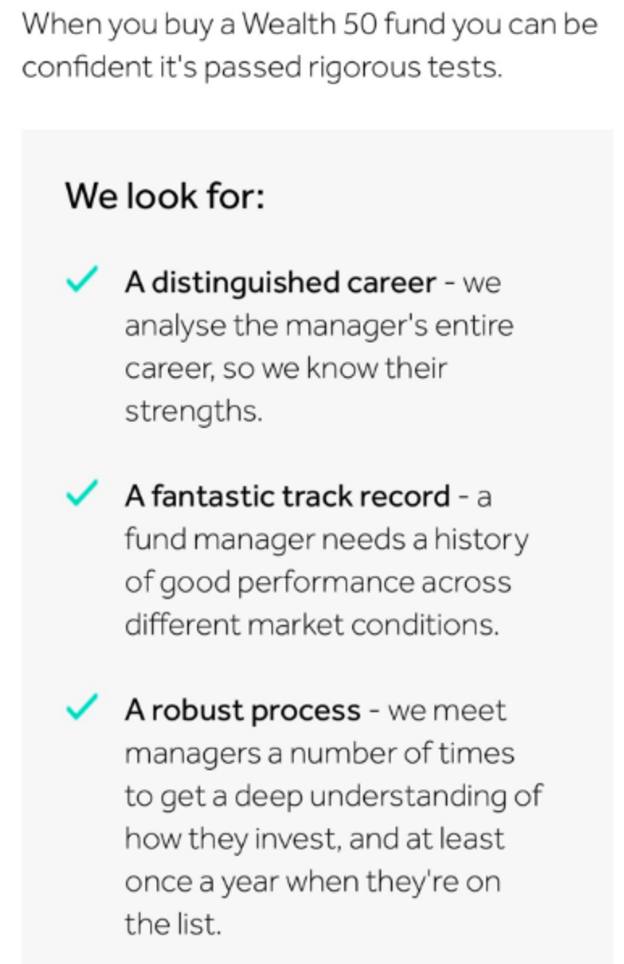

He pointed to wording on the platform's website that suggested the Wealth 50 list had “passed rigorous tests” and included managers with a “distinguished career” and funds with a “fantastic track record”.

Mr Resnik did not suggest that Hargreaves had broken any rules or strayed into advice, but rather that the ombudsman might find a consumer may have misunderstood whether they were being given advice.

A screenshot from the Hargreaves website:

Mr Resnik said: “You can’t just make a claim like ‘we don’t give advice’ and that’s it. You have to go to the mindset of consumers. And consumers could have taken that as a recommendation.”

Hargreaves disputed Mr Resnik's comments, saying it had made it "very clear that we offer information about investing and saving, but not personal advice.”

Hargreaves' website states at the bottom of every page: "Our website offers information about investing and savings, but not personal advice". It encourages consumers to contact their financial adviser if they are not sure about a product.

A spokesperson for the platform added: “The FCA’s research showed that buylists delivered better outcomes and value for investors.

“Our research has resulted in the selection of funds onto the Wealth 150/50 which have on average outperformed both their relevant benchmark index and their sector average after charges, by 5.8 per cent and 11.8 per cent respectively over the period they have been on the list."

Mark Polson, director at the Lang Cat, said that in regulatory terms Hargreaves had stayed at the “right side of the line” and had not crossed into advice.

But he added consumers might have thought they had received advice based on the way the buylist was advertised.

He said: “I think individuals have a different understanding of what advice means and if you asked consumers who invested through Hargreaves Lansdown, eight out of 10 would say the firm recommended it to them.

“But [the company] did not give ‘advice with a capital A’ and the firm does not know anything about the individuals who bought the funds through the best buylist, so could not give a personal recommendation.”

Mr Polson thought there was a possible “mismatch” between the regulation and those who believed they were recommended the product, which meant consumers could have some recourse with the Fos.

He added: “You just never know with the Fos. I don’t think anyone could tell.”

Mr Resnik said the Fos was more “consumer-centric” than the FCA and in its assessment of a case would likely ask "was this a positive recommendation?" and act accordingly.

Paul Stocks, director at Dobson & Hodge, agreed there was a possibility of the ombudsman ruling in favour of complainants, noting the service seeks out issues of consumer detriment. But he said that practice would risk creating further problems.

Mr Stocks said: “If consumers who don’t seek advice can get the same recourse as those that do when their investments don’t work out, then what does that mean? Where does that leave advice?”

imogen.tew@ft.com

What do you think about the issues raised by this story? Email us on fa.letters@ft.com to let us know.