The managers of UK investment trusts have U-turned on their gearing tactics as uncertainty grows and the sector tries to de-risk, data has shown.

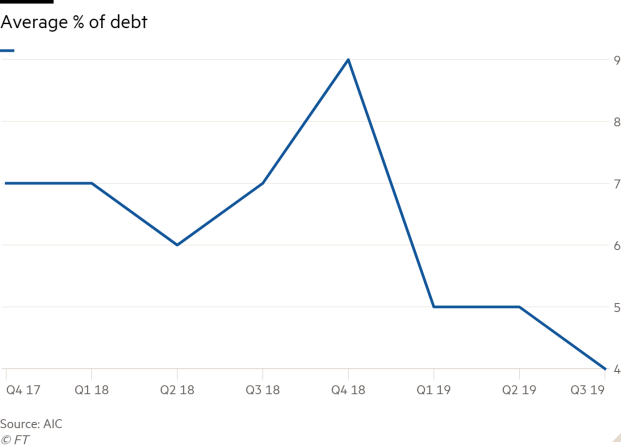

Data from the Association of Investment Companies and Morningstar showed from the end of December 2018 to the end of September 2019, the average trust in the AIC UK All Companies sector more than halved its gearing from 9 per cent to 4 per cent.

Debt in the average trust in the UK Equity Income sector decreased from 10 per cent to 8 per cent while reductions were also seen in the UK Equity and Bond category and the UK Smaller Companies category.

By comparison, last year investment trust managers bucked the political upheaval and opted for more gearing, with the average trust in the AIC UK All Companies sector increasing its gearing from 6 per cent to 9 per cent from July to the end of the year.

Investment trusts, unlike open-ended funds, can take on long-term debt and use it to make more investments.

If the money is invested prudently, then the investments should generate enough cash to repay the borrowed money with interest, and provide additional returns for shareholders.

If the money is invested badly, then the returns to shareholders are diluted by the need to pay the debt.

Advisers thought the reduced level of gearing was primarily down to reduced investor sentiment and uncertainty.

Simon Munday, director at Prosperity IFA, said gearing brought more exposure to risk which nobody wanted in the current uncertain environment.

He said: “There is a lot of uncertainty around at the moment and that’s why the managers of investment trusts will be adjusting their financial plans and outlooks accordingly.”

Jason Hollands, director of communications at Tilney, agreed, adding it was “not surprising” given the political uncertainties that the sector was looking to de-risk.

He thought cautious managers would want to ensure any gearing was comfortably within the covenants set by their lenders in the event of a reduction in the net asset value of their portfolio.

Peter Adcock, director at Adcock Financial Group, said it was a combination of Mifid II induced fears, a tightening of credit conditions and a more cautious investment approach in a global economy that was "clearly shutting down".

Meanwhile Kingsfleet Wealth’s managing director, Colin Low, thought the fact managers were lowering debt could help reassure some advisers who were averse to using investment trusts.

He said one of the reasons fellow advisers gave for not using trusts was that they considered them to be higher risk because of the possibility for gearing so any sign that showed managers were responsibly handling debt in uncertain times was a good thing.

He added: “The fact that the data suggests managers are paying down debt at a time when they are concerned about a slowing economy should be a reassurance and a reduction in debt is sensible if there are concerns about future company growth.”

Advisers have historically tended not to use investment trusts and some platforms — such as Old Mutual Wealth or Aegon — do not even offer trusts as an investment option.

A recent report from the Lang Cat put adviser aversion down to an “inherent market bias” which included the fact model portfolios appeared incompatible with investment trusts and that advisers saw the liquidity of investment trusts as a big issue.

imogen.tew@ft.com

What do you think about the issues raised by this story? Email us on fa.letters@ft.com to let us know.