The chaos that engulfed markets in March answered one of the great puzzles that had bewitched investment professionals over the past decade, but left several other questions unanswered.

As investors stared at the sea of red that swept across their screens with the pandemic bringing pandemonium to asset prices, a sliver of light emerged from the darkness, as the prices of most developed market government bonds rose stoutly when March gave way to April.

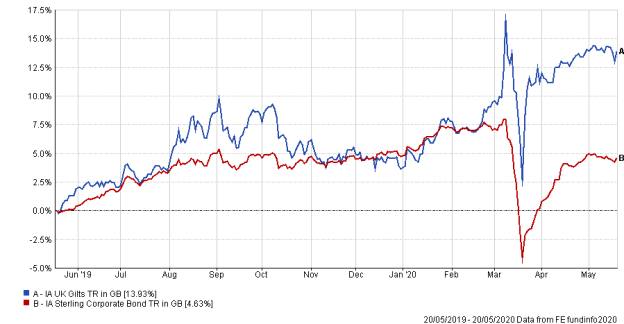

Data from the FE Analytics shows the Investment Association UK Gilts sector produced a positive return of 4.2 per cent for the months of March and April.

And, to an extent, that is the great bond market question answered.

Traditionally, the role of government bonds in a balanced portfolio is to be a diversifier from equities, and to rise in value when equities fall.

Government bonds

Government bonds tend to rise in value at times of severe market stress as investors rush to them as a safe haven, reasoning that the government will always have the cash to pay investors, even if the private sector is collapsing.

In addition, the fact that most global financial services companies, such as banks and insurers have to hold some government securities for regulatory reasons means there is always liquidity in those assets, so they can be quickly sold off in times of strife.

The question mark that dangled over the above hypothesis was whether, given how bond prices had risen sharply and consistently in the decade prior to the financial crisis, there was any room for government bond yields to rise further.

Andrew Hardy, co-head of research and a portfolio manager at Momentum Global Investment Management says government bonds will “always have a part to play” in portfolios because of the regular cashflow and liquidity.

Sebastian Mackay, multi-asset investor at Invesco, says UK and US government bonds had plenty of room to move upwards in price as they continued to trade at lower levels than Japanese and many Eurozone government bonds.

The bonds of those countries have traded at lower yields, and so higher prices, than their UK and US equivalents for a decade because the market expected those latter named economies to grow at a much faster rate than those of Japan and Europe, and so investors were more willing to hold the equities.

But he says the Covid-19 economic shock is such that “it has moved the UK closer to Japan in terms of outlook” and so government bond demand has risen.

A central driver of demand in all parts of the market is the vast programme of bond-buying being undertaken by central banks.

As FTAdviser has previously reported, the specific aim of such bond buying is to push bond prices upwards, and increase liquidity.

Dean Cheeseman, a multi-asset investor at Janus Henderson, says it took the instigation of another round of this bond-buying to make government bonds perform well.

Mr Cheeseman says: “In the first days of the sell-off, all anyone wanted was cash, and even the government bond market was buckling under the weight of people trying to raise cash. It was when central banks stepped in that government bonds began to perform better.”

He says that in a typical multi-asset portfolio, “I think there will always be a place for government bonds, due to the diversification that you get. The point of a multi-asset portfolio is to have assets that perform differently to each other, and that is what government bonds continue to do.”

Central banks have also been buying corporate bonds, and the effect of this has been seen across the bond market with prices also rising for most corporate bonds.

Bond yields

Mark Preskett, multi-asset investor at Morningstar Investment Management says the first thing to understand about bonds is that the yield on the bond at the time the purchase happens is the major determinant of what the returns will be in future, and with bond prices already very high, even if the diversification effects remain as potent in years to come as they proved to be in March.

He says that to achieve the diversification “investors are just going to have to stomach the low yields.”

Aviva Investors bond fund manager James Vokins says that “equity investors have not been able to believe how low the yields had gone on bonds", but with central bank intervention and low levels of economic growth forecast for the foreseeable future, “bond yields can always go lower.”

Bond yields move inversely to bond prices, so lower yields mean the price is rising. The higher price is positive for investors whose priority is capital gain, but negative for those who want income.

Bob Tannahill, multi-asset portfolio manager at wealth management Ravenscroft says he continues to use bonds in multi-asset portfolios for clients, but believes that corporate bonds, while having a higher yield than government bonds, were shown in the sell-off in March to be much less liquid.

He says: “We will continue to use bonds in balanced portfolios, but we have to be realistic about what you are buying today.

"Liquidity cannot be assumed in the same way it was before the global financial crisis and this was hammered home in March. So in building a balanced portfolio today, if you need liquidity in the toughest of periods then you probably need to think about assets other than corporate bonds such as short-dated government bonds or cash.

"Here again, however, we have to be realistic on pricing.

"In the past, these bonds were an insurance policy that paid you to hold it, thanks to yields trending lower over time. Today, a bit like real world insurance policies, there will likely be a price to be paid in terms of portfolio return over the medium to long term for having this protection and that needs to be considered.

"Finally, corporate bonds still have income and lower volatility characteristics to offer and so a role to play.”