The risks and dangers of cryptocurrencies

- Describe some of the risks associated with cryptocurrencies

- Identify what companies have to do if they are involved with cryptoassets

- Explain what companies have to do to protect themselves from internet criminals

- Describe some of the risks associated with cryptocurrencies

- Identify what companies have to do if they are involved with cryptoassets

- Explain what companies have to do to protect themselves from internet criminals

Cryptoassets are a relatively new commodity – not to be confused with ‘cryptocurrency’, ‘digital asset’ or even ‘digital token’ – but they are growing in popularity and the Financial Conduct Authority is starting to have more of an oversight of this widening market.

While often associated with criminal activity, their legitimate use is also growing and many in the financial services industry are keen to see them reclassified as a mainstream commodity.

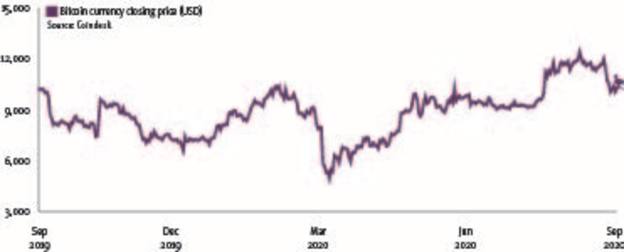

While their valuation is extremely volatile, the peaks can mean they offer very high returns.

In light of this trend, and given the significant risks, even financial services companies not involved in cryptoassets need to take heed of the potential dangers associated with them – especially as these risks have increased as a result of the coronavirus pandemic.

What are cryptoassets?

There is currently no legal definition of this new asset class and one of the barriers to gaining a clear understanding of this topic is the inconsistency of language used by regulators and market participants, as well as confusing terminology.

The FCA describes a cryptoasset as “cryptographically secured digital representations of value or contractual rights that use some type of distributed ledger technology and can be transferred, stored or traded electronically”.

Bitcoin is the most commonly known DLT, which allows data to be stored globally on thousands of servers, although Litecoin, Ethereum and Ripple are other examples. It is designed so that everyone on the network can see everyone else’s entries in near real-time.

Within this umbrella term, cryptoassets can perform very different functions. Practically speaking, cryptoassets can generally be separated into three types:

• Those acting as a voucher for an external reference asset or service, eg rights in property;

• Those that are exchanged for value – the most commonly used of which is Bitcoin; and

• Those that act as the building block for applications, sometimes labelled ‘cryptofuel’, which assists with the development of blockchain applications.

Increased activity

Given the decentralised nature of cryptoassets, it is difficult to accurately chart the growth of cryptoasset activity as an asset class.

However, market commentators have suggested that there has been a massive uptick in cryptoasset activity since the Covid-19 pandemic began, with investors willing to take the unmistakeably high risk of investing in this type of asset.

Cryptoasset trading is still not a mainstream investment offered by the big trading houses.

Key Points

- Many in financial services would like to see cryptoassets classified as a commodity

- Bitcoin is the most well-known crytpoasset

- Many criminals use cryptosassets due to their anonymity