Article 4 / 4

Investing in multi asset strategiesIdentifying return prospects in a fragile environment

At the start of 2017, US growth was expected to benefit from president Donald Trump’s “America first” policies, meaning a strong dollar and higher Treasury yields.

Elections in Europe added political risk to a sluggish economic recovery and the UK was set to enter unknown territory once Article 50 was triggered. To position a portfolio at the outset needed a contrarian view and an active approach to asset allocation, with a focus on relative value as much as absolute.

Eight months on and the US dollar has fallen. Emerging market equities have risen more than 20 per cent and bond yields have fallen further. There are many more examples of consensus trades that have turned out to be very costly.

Valuations remain a concern. Credit markets are priced for perfection and corporate earnings need to rise to justify valuations at a time when consumers are under pressure from falling real incomes.

Loose monetary policy may have prevented a depression, but long-term growth prospects remain modest and the risk of market falls when monetary stimuli are withdrawn is real.

The right approach in this fragile environment has been to use the full breadth of the global universe to identify attractive opportunities, looking for a blend of bond, credit, real estate, infrastructure and equity opportunities that collectively offer an attractive risk-adjusted return.

Portfolio construction has also been an important consideration and a source of added value.

While diversification has always been critical, we must be wary of over-diversification. Thus it looks wise to employ a relative volatility target to ensure risk levels remain appropriate, and hold fewer securities where we find less attractive opportunities.

Our equity specialists have been overweight large-cap technology stocks on the basis that their business models are powerful and cashflow growth has been stellar. These growth stocks are held in growth portfolios, but are more difficult to accommodate in income portfolios because dividend yields are too low.

But a positive view on technology has led to some higher-yielding stocks such as a Taiwanese tech companies that are suppliers to mobile phone manufacturers.

Another example of opportunity relates to the impact of e-commerce on traditional retailers and investing in subsectors. Many market participants hold Amazon, but its business model also could lead investors to property companies that own warehouse distribution sites designed to facilitate the needs of e-commerce retailing.

In fixed income there has been a return potential in bank bonds. Regulators required banks to hold more capital, delay distributions to shareholders thereby reducing credit risk.

US banks led the way and their European counterparts are now more interesting from a credit improvement perspective. It makes sense to build a portfolio of the most attractive bank credits to benefit from this investment idea.

In these ways, investors can remain positioned for modest growth and a continuation of the ‘lower-for-longer’ theme that has dominated capital markets in recent years. We expect central banks to err on the side of caution and policy tightening will be gradual.

Owning credit, equity dividends and currencies remains attractive but should be targeted rather than indiscriminate.

Vincent McEntegart is a multi-asset investment manager at Kames Capital

Key figures

Zero - Number of pro-growth corporate tax reforms passed by US president Donald Trump

12.8% - Reduction in the yield on a 10-year US Treasury year-to-September 1

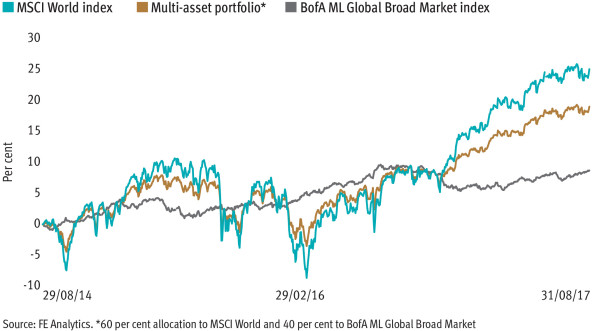

7.6% - 2017 volatility for a 60/40 portfolio in global equities and global bonds

March 2019 - Date the UK is expected to withdraw from the European Union