Trade bodies and regulators have urged pension providers to adopt a new two-page annual statement when communicating with their members.

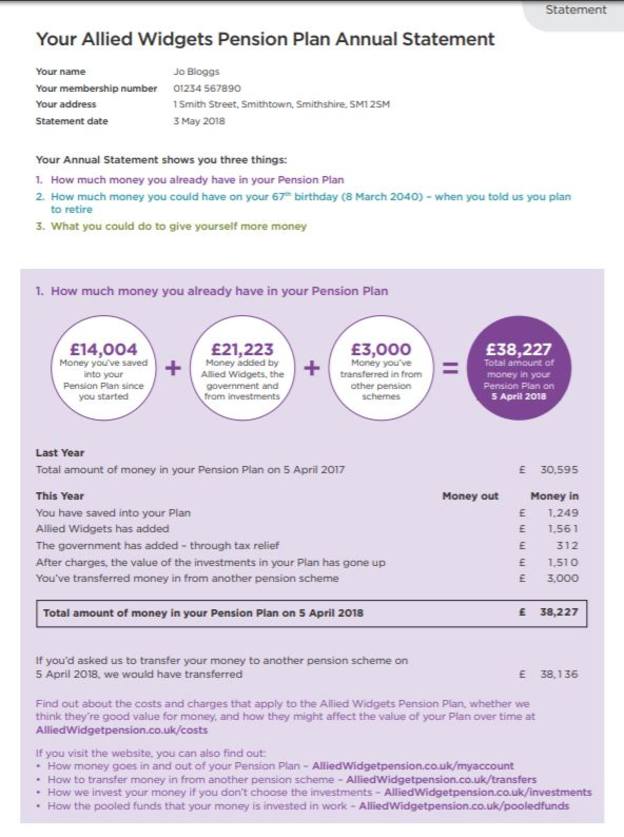

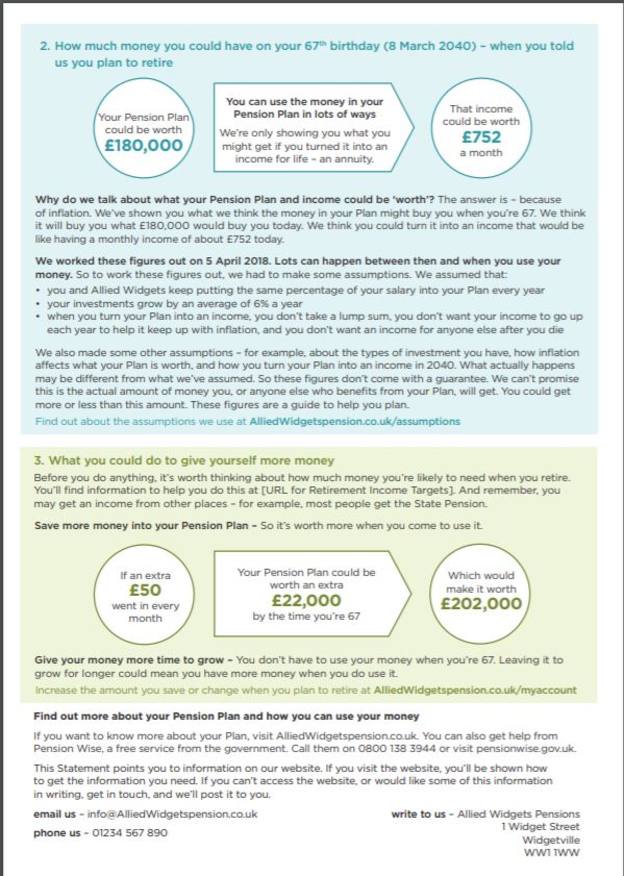

The document, which was developed collaboratively by an industry group in response to the government’s 2017 review of automatic enrolment, provides information on the amount of money someone has saved into their particular pension scheme, the amount their employer has contributed, the tax relief they have benefited from and the amount of money they have in the scheme.

The statement also signposts to other detailed information that can sit separately on a website. This reflects legal requirements and can be adapted by providers using their own branding, the industry group said.

Guy Opperman, minister for pensions and financial inclusion, launched the statement as an example of best practice at the Pensions and Lifetime Savings Association (PLSA) annual conference yesterday (18 October) in Liverpool.

The Financial Conduct Authority has also given it its blessing, stating it was "supportive of its aims".

The document was developed collaboratively by Ruston Smith, co-chair of the DWP’s 2017 automatic enrolment review advisory board and chairman of the Tesco Pension Fund, Vincent Franklin and Mark Scantlebury, from communication consultants Quietroom, and Karen Mumgaard and Francois Barker, from law firm Eversheds Sutherland.

It was tested by Ignition House, which conducted independent research involving more than 70 in-depth interviews and a survey of 1000 scheme members.

The research found the two-page document was clearer and easier to understand for consumers and that it could be read and understood in two minutes.

The respondents said they were more likely to read the simpler annual statement than a longer version and would consider it alongside their other statements to work out what they’ve got.

The new statement, however, won’t include information on costs and charges.

Mr Smith said information on costs and charges was critical but it was important to get transparency and consistency right.

He said: "When we looked at the research about the simpler annual statement, people were asking questions but also trying to come to their own answers to those questions and getting them wrong. That is very easy to do in the way we present information.

"So let’s make sure it is simple, it is consistent, so if you're comparing one statement with the other you can understand it. There is no requirement on the statement itself today to include information on costs and charges, but there is a requirement to signpost it to a website where this information is available."

Lesley Titcomb, chief executive of The Pensions Regulator (TPR), said it was important people understood the importance of savings to provide an adequate income in retirement, especially as more people start to build savings through auto-enrolment.

She said: "We encourage the trustees of any defined contribution scheme looking to improve its member engagement to take this new format on board as good practice."

Alex Roy, acting head of cross-sectoral & funds policy at the Financial Conduct Authority, said the regulator supported measures to make pensions more understandable for consumers and understood the benefits of a simpler annual pension statement.

He said: "We are always open to ideas which can deliver better outcomes for users of financial services. As such, we have engaged with the working group during the development of the statement and we’re supportive of its aims."

The watchdog is also currently reviewing the effectiveness of the retirement wake-up packs, which are sent by providers to individuals six months prior to retirement age.

Companies that support the launch of the simpler annual statement include Legal & General, Aviva, Hargreaves Lansdown, Scottish Widows, Smart Pension, Pensions Bee, Nest and The People’s Pension.

maria.espadinha@ft.com