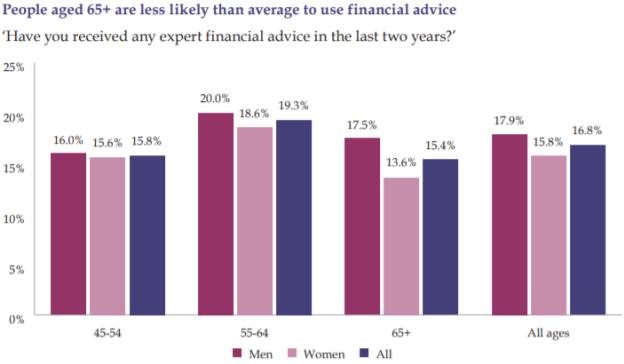

People that have already entered retirement are less likely to seek advice than those aged under 65, despite decisions in later life being more difficult to navigate due to the pension freedoms, a report has warned.

A report from the Pensions Policy Institute (PPI) looking into the complexity of financial decisions older people may face in later life, published yesterday (October 23), found that in the run up to retirement (ages 55-64), 19.3 per cent had received advice, falling to 15.4 per cent after the age of 65.

The PPI warned at present the focus was on providing advice during the accumulation phase and at the point of transition into retirement, despite the introduction of pension freedoms in 2015 making the decisions throughout retirement a lot more complex.

It said people were likely to need much greater support in terms of ongoing guidance and advice in later life in order to be able to make appropriate decisions about how to access and utilise their retirement savings to meet their needs.

The report stated: "Given the complexity of retirement decisions, many people will find it difficult to make choices that will best meet their needs over the course of later life.

"For some people, initiatives aimed at increasing engagement and financial capability will equip them to make appropriate decisions.

"Advice and guidance plays an important role in supporting people while making these choices, although most advice and guidance offerings currently focus on at-retirement decisions rather than ongoing support throughout later life."

But Darren Cooke, chartered financial planner at Red Circle Financial Planning, did not fully agree with the PPI's assessment.

Mr Cooke said: “I think the vast majority of advice firms have developed services for in-retirement clients to deal with their more complex needs and want to continue to provide a service to those clients.

“Guidance services provided by government agencies etc, may not have kept pace with this change in the retirement choices to provide ongoing support but that is not the fault of the regulated advice profession.”

The PPI said initiatives aimed at helping people better understand the value of advice could help to increase take-up levels later on in life.

Robo-advice could also play a role as it offers continuous access which is not constrained by distance or opening hours, as well as access to a larger amount of information, it said.

But the PPI said others may need more support from government to achieve a better retirement. This may include government setting default options for people who are unable or refuse to make an active choice in retirement or safety nets which are designed to help those in financial hardship to protect them from the worst outcomes.

The government and regulator are already looking to introduce default options in drawdown to protect consumers.

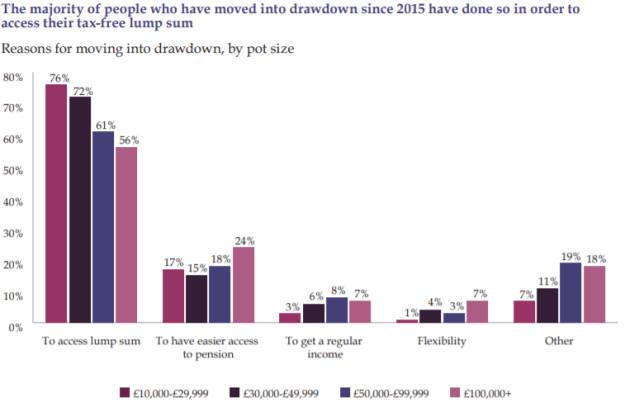

The PPI found the proportion of advised drawdown purchases had increased in the two years to 2018, from 68 per cent in 2016 to 77 per cent in 2018.

But a mere 37 per cent of drawdown customers said they knew exactly where their money was invested, alongside 34 per cent who claimed they had a broad idea and 28 per cent who were not sure.

In fact, the majority of savers seemed to be accessing drawdown to get access to their tax free lump sums, it found.

The PPI found that awareness of drawdown investments correlated with pot size, with three quarters of those with pots of £200,000 or more knowing exactly where their money was invested compared with one in five of those with pots between £10,000 and £29,999.

Tim Morris, independent financial adviser at Russell & Co, said: "Although defined contribution pensions are now the default, many members of occupational pensions still don’t understand fully how their money is invested and level of risk/volatility. Most just see an increase from the contributions paid in during the accumulation stage.

"The key differential post retirement is to keep more in the short term pot to draw upon. This is important where you remain at the mercy of the markets. It can help negate the impact of 'pound cost ravaging' where the markets fall soon after retirement."

amy.austin@ft.com

What do you think about the issues raised by this story? Email us on fa.letters@ft.com to let us know.