Lifestyle insurance is increasingly being developed and used to help people in short-term employment contracts, renting or getting them into the protection habit.

It has not been easy for the industry, however, to sell short-term protection products. To some extent, decent products have been sitting in the shadows as a result of the scandalous way banks and building societies flogged payment protection insurance (PPI).

Figures from the Financial Conduct Authority reveal just how costly the mis-selling of PPI has been. A total of £205.3m was paid in April 2017 to customers who complained about the way they were sold payment protection insurance (PPI). This takes the amount paid since January 2011 to £27.1bn.

So it is understandable why many consumers are distrustful of the protection industry - to the layperson, 'protection' and 'insurance' can have negative connotations.

Paul Reed, co-founder of Cardiff-based Vita, agrees this is an issue. He says: "The key thing is, no matter the badge on the product, the consumer has to be number one, and they need to be aware of what they are getting."

But the PPI furore also affected advisers who never advised on PPI, with spurious claims against financial advisers reaching the Financial Ombudsman Service, only for the cases to be dismissed after a lengthy process.

For example, Alan Lakey, founder of CI Expert, and Derek Bradley, founder of online advisory forum PanaceaAdviser, went to the Ministry of Justice back in 2013 to present their cause against frivolous claims being brought by claims management companies.

Yet a year later, as reported by Financial Adviser, ambulance chasers were still submitting phony claims against advisers.

To some extent, this could be why intermediaries have tended to stick to products such as long-term income protection plans or workplace protection, rather than look at shorter-term alternatives, even when these alternatives may be the best product for the client at that time in their lives.

Usefulness of short-term protection

However, lifestyle insurance is increasingly meeting a need for what Mr Lakey calls the "budget option, as it keeps costs to a minimum by limiting claims in payment to a specified period, such as two years".

He cites a growth in the number of products available to advisers from income protection insurers such as LV=, The Exeter and British Friendly Society.

Peter Hamilton, head of retail propositions at Zurich, comments: "PPI and lifestyle insurance are different. PPI is typically very short-term protection, up to 12 months. It is also renewable annually, so premium levels and cover are not guaranteed.

"Most PPI plans only pay out if you do can't do an occupation for which you are suited by training or experience.

"However, an income protection plan, whether short or long term, will typically cover your own occupation, giving you a much better chance of making a successful claim.

"There's no doubt more and more advisers see this kind of proposition as suitable for growing numbers of their own clients. These products can provide a very helpful foundation."

Standalone product

Importantly, according to Andrew Sajo, spokesman for The Source, the fact that lifestyle insurance is a standalone product makes it a good product for advisers to consider for clients.

He explains: "The vast majority of PPI was coupled with a financial services product, but short-term income protection plans are based on the customer's individual lifestyle commitments, rather than being coupled with a single product."

According to Mr Sajo, some 56 per cent of Source's IFAs and mortgage brokers said if you can get the product right, there is "huge potential" when it comes to providing short-term cover for clients.

He adds: "The main barriers to sale are the stigma attached to the PPI mis-selling, price and product flexibility. If you can tackle these barriers, this will give even more confidence to IFAs offering this type of product to clients."

Generation rent

For Emma Thomson, life office relationship director for Lifesearch, it is important to help more people get engaged with protection, and she believes specific products such as lifestyle insurance, given its short-term nature, can help a wide generation of people.

In particular, she points to Generation Rent as a prime market for short-term insurance products. With more people renting now than ever before, and a higher proportion of working people aged 40-plus living in rental accommodation, Ms Thomson believes a greater range of short-term, flexible insurance products are needed.

She explains: "Products designed for the rental market could really help. Too much emphasis is on protecting mortgages and there is not enough focus on renters, who are arguable more exposed in some cases.

"It would make sense to have a simple application process, so an automated acceptance-style product like PPI or accident, sickness and unemployment, could appeal better to consumers and advisers."

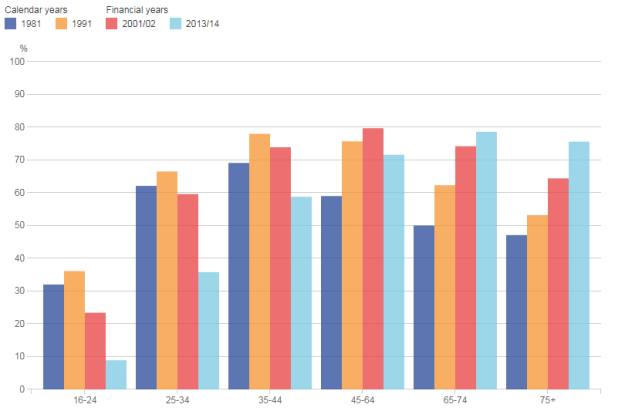

Indeed, figures from the Office for National Statistics show how since 2010, the number of homeowners aged 40 and under has fallen considerably. The pale blue bar shows just how much homeownership among the youngest - 18 to 24 - has fallen since the 1980s and 1990s.

Ms Thomson believes lifestyle insurance products go further than ASU, however, as ASU has exclusions for pre-existing conditions, which can be a downside. Another potential downside to ASU is that cover can be withdrawn or changed at the renewal stage.

Therefore, some form of shorter-term income protection plan like lifestyle insurance products, which would have an element of underwriting, would "make sense", she comments.

Engagement

Ms Thomson adds: "Moreover, short-term products can present the opportunity to get people engaged with protection quickly and easily, and use that as a stepping-stone to help arrange more comprehensive cover when they are ready for it."

Moreover, because lifestyle products are sold as an advised product, this makes it an important part of the adviser's toolkit when it comes to engaging and recommending cover, according to Julie Highman, income protection product manager for Aviva.

She explains: "Short-term income protection is sold as an advised product so the consumer is guided through a fact find with their financial adviser, first to establish their needs and then to recommend the correct product and options within that product to meet their specific needs."

simoney.kyriakou@ft.com