Segmenting clients into bands and groups is an invaluable method for advisers because it ensures tailored advice, products and services, to each segment and, therefore, to each client.

It also leads to correct charging structures and enables advisers and their companies to evidence and track clients’ financial journeys, were they to come under scrutiny.

“For example, if the client files a complaint and says they have been given the wrong service or that they are being overcharged, that can then point straight back to the fact that the advisory firm has not segmented properly,” explains Chris Davies, founder of Model Office.

He continues: “The benefit to the firm in segmenting clients is they streamline which means services become far more efficient, effective and profitable.”

With the Senior Managers and Certification Regime only months away, it is more important than ever for advisers and their businesses to recognise and understand the importance of segmentation and ensure it is done right.

But whether or not an advice company segments its clients depends on the size of the firm, according to Mr Davies.

He says: “There are still some firms not doing it or paying lip service to it and that has got to stop because they will be found out particularly with SMCR coming through.”

He adds: “Not segmenting is dangerous; you have to segment to ensure the right clients are getting the right service.”

Mifid II: a Prod in the right direction

The Financial Conduct Authority received 1,335 notifications of inaccurate transaction reporting last year. The figures, published by regulatory consultancy Bovill, provide a snapshot into how companies adjusted under the weight of Mifid II in its first year.

In fact, since the directive took effect in January 2018, advisers have been warned the client segmentation they carried out directly after the Retail Distribution Review in December 2012 would not be sufficient under the new rules.

Jamie Farquhar, business development director at Square Mile, explains: “When commission was killed and fees were introduced it was obvious that IFAs would have to segment their client base and define a service proposition to the different segments, in order to justify the fees that they were charging for that service for each segment.”

To understand how advisers are currently segmenting their clients and how it works more generally, it is important to take a step back and look at what the current rules say.

The FCA’s Product Intervention and Product Governance Sourcebook defines product oversight and governance as “the systems and controls advice companies have in place to design, approve, market and manage products throughout the products’ lifecycle to ensure they meet legal and regulatory requirements.''

It also states that good product governance results in products that meet the needs of one or more identifiable target market and are sold to clients through appropriate distribution channels to deliver appropriate client outcomes.

The aim of the Prod was to improve the industry’s product oversight and governance processes and it sets out the FCA’s statement of policy on making temporary product intervention rules.

According to Mr Davies, what advisers need to keep in mind is that product governance in its own right is all about product manufacturers and target market criteria.

He suggests this is because product manufacturers have to factor in the way they build their product features such as benefits, costs and charges, into the client type: the knowledge and experience of the client as well as their ability to bear losses, their objectives, needs and their risk appetites.

Then there are, of course, the distribution channels, or in this case, IFAs.

The FCA provides suitability rules for advisers to ensure that their services, and their products, are suitable to meet clients’ needs.

This is where segmentation comes in because what Prod demands is that advisers clearly segment clients around the outcomes clients are trying to achieve, according to Mr Farquhar.

He explains: “You have to define the target market for the different segments of your centralised investment proposition, at which point you need to really segment your clients and define their revenue and the service proposition you can give them."

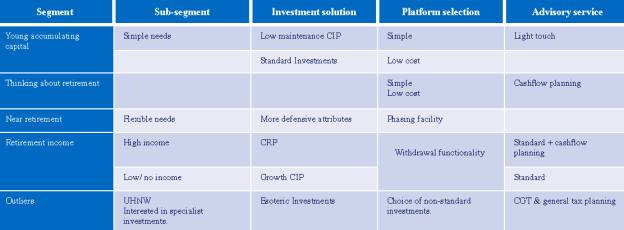

Source: Square Mile

How are advisers segmenting clients?

The way advisers have historically come at segmentation, if at all, has been fairly transactional, according to Mr Davies.

By 'transactional' he means segmenting around two key demographics: age and assets under management.

But in a post-Mifid II environment, that is no longer enough to comply with the requirements, he suggests.

Mr Davies explains: “It will not meet the rules and regulations; it is not going to meet what clients need.”

So what will? These days it is a lot more complex, and he suggests segmenting clients has to be taken from a behavioural point of view.

He continues: “[So] if you segment clients now you also have to factor in whether it is profitable for the business to take on a certain section of clients, different types of technologies, costs and charges – how much you are going to charge each particular section of the clients – and then you also have to factor in and map over the product arrangements target market criteria.”

He adds: “It's not an easy exercise and advisers often think they can approach it transactionally, based on age and wealth, but that is just not going to work.”

According to Jiten Varsani, mortgage and protection adviser at London Money, some advisers segregate based on occupation: teachers, doctors, lawyers.

He says: “Of course there are those who do not have set segregation criteria but may have a minimum fee for any work carried out which in turn could lead to segregation between those with the means to pay and those that cannot afford it.”

While Mark Polson, principal at the Lang Cat, says: “We are finding more and more that advisers are becoming aware of the requirements of Prod in terms of segmenting clients by need rather than asset size.

“This is a good thing because AUM is a pretty bad indicator of client requirements, except at the extremes.”

He continues: “Whether firms are doing it by life stage, or by occupation – so one segment for employed accumulators, another for company directors, another for doctors and other senior public servants – we are seeing firms move up and away from pure AUM segmentation.

“Arguably firms have segmented on attitude to risk for a long time; that drives the portfolio they are in, but this is something a little more fundamental than a slightly tweaked asset allocation.”

Fact find is key

Importantly, you cannot segment until you have done a fact find, notes Mr Farquhar.

He explains: “You need to understand exactly what the client's financial position is, what their needs and aspirations are etc.

“The client fact find is everything: if you get that right everything else falls into place.”

For example, he says you might have a segment of clients that are looking for long-term growth and accumulation of value in their portfolio as they are saving for retirement.

He continues: “Yet within that segment, you need to go through attitude to risk and appetite for loss at which point you might use an attitude to risk questionnaire, but there will also be multiple risk profiles for clients that sit within the same segment of client outcomes.

“But I think the most important thing with tools like the ARQ, is that they are designed to encourage a genuine conversation with the client.”

Victoria Ticha is a features writer at Financial Adviser and FTAdviser