The Financial Services Compensation Scheme chief executive has vowed to work with the advice industry to mitigate the effect of regulatory cost rises on advisers and make the lifeboat work better for consumers.

Caroline Rainbird said the organisation would meet with the industry to help address the root causes of people falling into the FSCS, and improve consumer confidence in financial services.

She said: "We recognise the problem that rising costs have for advisory firms against a challenging economic backdrop", acknowledging that while there is no "simple solution" to the "complex problem", the FSCS is working to minimise those elements of the FSCS levy which are under the organisation's control.

This includes its management costs, recovery of money and work to prevent future failures and their subsequent drain on the levy.

Ms Rainbird said: "We will continue to meet regularly with all parts of the industry, including Pimfa, to help achieve these two important elements.”

Her comments came as trade body Pimfa unveiled its latest study into the advice market.

In a 12-page report, 'A rising tide lifts all boats', the Personal Investment Management and Financial Advice association confirmed that financial advice business owners and chief executives of wealth managers were suffering from unsustainable rises in professional indemnity insurance premiums and FSCS levies.

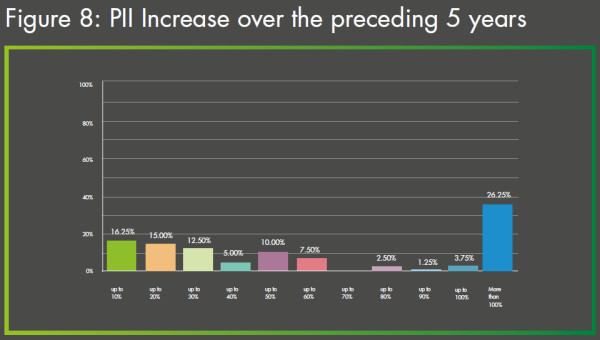

Over the past five years, the report showed, 45 per cent of all member firms have seen increases of more than 100 per cent in their FSCS levy bill, while 26 per cent have seen rises of more than 100 per cent in their PII premiums.

The report stated: "Rising PII premiums represents a significant challenge for firms as well as the FSCS longer term. Without the ability to cover claims, firms will fail and fall onto the FSCS raising compensation claims and FSCS levies as a result.

"Pimfa firms are already not confident in their ability to gain affordable PII cover in the short term future, with only 17 per cent considering themselves very confident in their ability to gain affordable cover next year."

In September, the Financial Conduct Authority told its annual public meeting that the regulator was aware of adviser concerns over a hardening of the PII market, and that it was working to tackle shortfalls in PII cover.

But while discussions continue, the reality for advice businesses is that the costs are becoming unsustainable.

The survey of 84 member firms also revealed the impact of these rising costs on the businesses' bottom line: 82 per cent of members said FSCS costs now accounted for at least 20 per cent of all outgoings.

But members said their levels of trust in the FSCS to deliver fair outcomes for consumers or their firms had not improved in the past five years.

Liz Field, chief executive of Pimfa, stated: "The FSCS plays an absolutely vital role in protecting consumer savings and we recognise that the trust it engenders for consumers has a benefit to our firms.

“But the results presented in this survey point to a wider disconnect between a profession, which seeks to deliver the best possible outcome for consumers, and a regulatory system that most firms see as providing inadequate support at best, or failing both consumers and firms alike at worst."

Last week, FTAdviser reported on the incoming phase two of the Treasury review into regulated financial services in the UK.

Following its 2019 consultation paper: Financial Services Future: Regulatory Framework Review, the Treasury's review will look into aspects such as checks and balances on the regulator, and how the FCA interacts with the Treasury.

At the time, industry commentators called this an "opportunity" for the UK to create a regulated financial services market that worked for the UK.

Rob Sinclair, chief executive of the Association of Mortgage Intermediaries, told FTAdviser: "It is fundamental that whatever solution we produce out of the back end of this, it has to work for every aspect of the advice marketplace, and we have to work together to deliver that outcome."

simoney.kyriakou@ft.com