PARTNER CONTENT by JUPITER ASSET MANAGEMENT

This content was paid for and produced by JUPITER ASSET MANAGEMENT

IG credit: bubble trouble, alpha opportunity, or both?

Current conditions in the sterling investment-grade corporate bond market warrant an approach that is active, pragmatic and risk aware. Those who embrace such a philosophy may discover some attractive alpha opportunities ahead.

As an asset class, corporate bonds have many well-recognised attractions. There are, after all, good reasons why investment-grade credit is a mainstay allocation in many well-diversified portfolios.

One of the primary features of bonds is that they are finite instruments, characterised by a contractual obligation to generate a stream of cashflows. This certainty of cash flow and specified duration typically delivers lower volatility relative to higher beta risk assets such as equities. However, because the cash flows themselves are capped, credit spreads operate in a mean-reverting manner. When the market is excessively bullish, these finite cashflows become too richly valued, and this lays the base for future underperformance.

For investors who are prepared to undertake diligent, fundamental credit research, and to reduce risk exposure into euphoric market conditions, sell-offs can provide attractive opportunities to generate alpha, as and when they materialise.

Lessons from history

Within our investment-grade corporate bond portfolios, 2020 provided a particularly strong example of this philosophy in action. We entered the year defensively positioned, believing that bond valuations were too rich relative to economic fundamentals and that better entry points would subsequently present themselves. Covid-19 was the pin that pricked the bubble, but with investors positioned so bullishly, any economic weakness could have prompted a repricing.

As the coronavirus spread, our research had focused on how the pandemic itself might evolve, and on considering the outlook for issuers that we believed had sold-off excessively in the initial drawdown. Having entered the pandemic with a relatively defensive stance, the subsequent sell-off created opportunities to increase portfolio risk at attractive entry points, even as many of our peers were forced to crystallise losses by selling corporate bond exposure into the credit spread widening.

As the pandemic drew on, an overwhelming sense of fear in the market gave way to euphoria, as investors perceived that health risks from covid-19 were contained, and that, in any event, governments and central banks would continue to provide policy support at levels that might once have been considered unimaginable. To believers in this “free lunch” theory, a recovering economic environment will continue to be combined with emergency settings on fiscal and monetary stimulus indefinitely. Inevitably, this has led credit spreads to tighten to multi-year extremes – and for us to become increasingly concerned about valuations in certain parts of the high-yield and investment-grade credit markets.

We believe it is at such times, when the market narrative becomes so manifestly one-sided, that it is hard to overstate the importance of both a cool head, and of continuing to undertake the detailed valuation work and sell-discipline that is one of the mainstays of our approach. Put another way, history teaches us that in these conditions, across virtually all major asset classes, few things are as mean-reversionary as credit spreads.

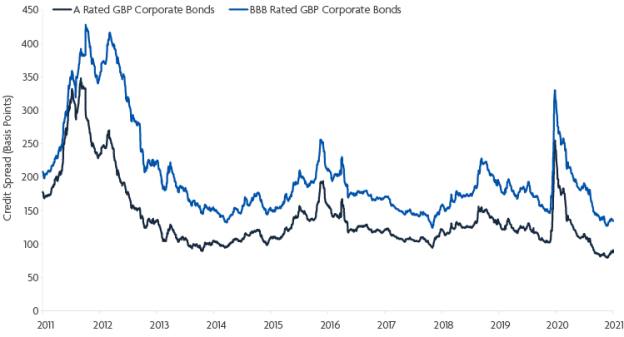

Source: Bloomberg, as at 31/3/21

Credit spreads are at historically low levels, but history shows that their tendency to revert rapidly to the mean should not be underestimated.

While equity investors may continue to anticipate strengthening performance into a reflationary growth environment, we believe credit investors would be wise to display greater caution. We reiterate that the upside in bonds is at all times capped by their defined and finite cash flows.

When market sentiment has led to credit spreads already anticipating a huge amount of good news, as is the case today, then incremental positive updates around vaccination and economic re-opening may be incapable of delivering future outperformance. It has been informative to us that sterling investment-grade corporate bond spreads have moved very little year to date despite increasingly bullish economic news and ongoing fiscal and monetary stimulus. This may signal the start of broader market exhaustion and/or unease with prevailing bond valuations.

In essence, there is a strong argument to be made that the so-called “beta trade” is complete in sterling investment-grade corporate bonds. If this thesis is accurate, then it is the more cautious investors who will be best placed both to cushion themselves against capital losses if sentiment should turn and spreads should widen, and indeed to capitalise on potentially attractive re-entry points that could materialise thereafter. Rotating into more defensive bonds now and reducing exposure to sectors and/or issuers where the current bull market has led to risk being mis-priced provides the platform to re-engage when valuations are more attractive. It is, we would suggest, a textbook example to support the arguments in favour of taking an active, pragmatic and risk-aware approach to the asset class.

How low can spreads go?

Credit spreads are currently at historically low levels, reflecting the very low level of additional interest that corporate bond issuers must pay to bondholders relative to the rates paid by the UK government on Gilts, despite the key differences in the risks to the holders. Our view is that credit spreads at these levels can only be justified if investors believe the world has entered a fundamentally new paradigm of global economic growth and fiscal/monetary accommodation.

In our opinion, new paradigm arguments are potentially dangerous and only surface at the peak of bull markets, and we believe that bond investors would be wise to look beyond this rose-tinted view of the world. In investment-grade credit, the new paradigm theory seems to combine two drivers which, to us, are mutually exclusive: (i) that the world is moving into a period of robust economic growth (“the roaring 20s”), and that (ii) central banks and governments in this period of robust growth will continue to provide unbridled liquidity and fiscal support to markets. With covid-19 still ongoing, with concerns around global asset bubbles, with increasing focus on inflation risks, and with economic growth rates picking up as the world emerges from lockdown, we believe that risks to current complacency are high. Valuation is a poor short-term timing tool in markets, but history teaches us that from current valuations prospective future excess returns in credit will be poor.

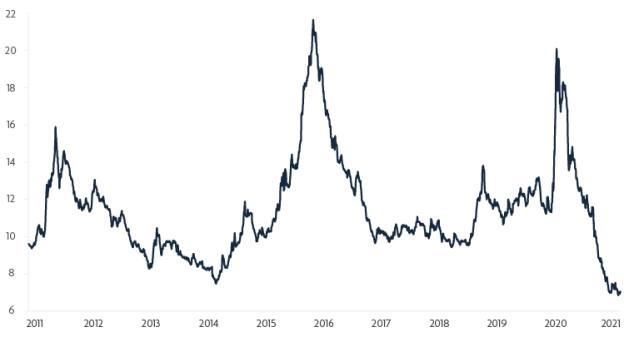

Our strong belief that we are at a cyclical top in credit is reinforced by what we are seeing in the high yield market, where we manage portfolios in other strategies. Typically, it is in the high-yield market that warning signs first manifest themselves of egregious bullishness, and at present we would point to a number of red flags, including record low credit spreads, the emergence of increasingly leveraged businesses, issuance of bonds with weak covenants, and companies raising large amounts of debt to pay dividends to shareholders.

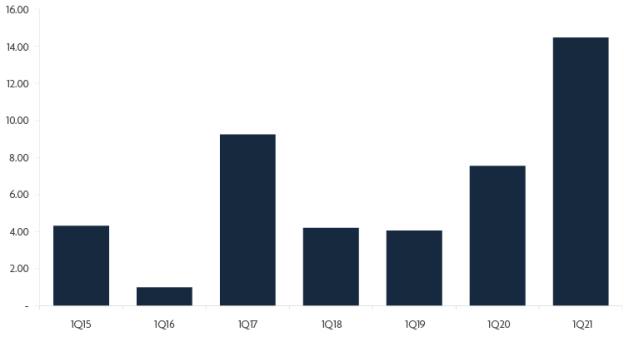

Source: JP Morgan, as at 31/3/21

Source: Bank of America, as at 22/4/21

Issuance of low-quality CCC-rated high-yield bonds so far in 2021 relative to previous levels, combined with a sharp decline in yields are signs to watch, potentially suggesting that this area of the market is already richly priced amid high investor risk appetite. Could potential trouble here make its presence felt further up the credit-quality spectrum?

To us, these realities all point towards sentiment being stretched to the upside. Meanwhile, if sentiment reverses sharply in the high-yield market, the effects can quickly ripple up through the credit-quality spectrum into investment grade.

Risk and opportunity: a delicate balance

This begs an obvious question: what is the appropriate response to stretched valuations in terms of allocations to investment-grade credit? Simply put, current tight spreads do not scare us, for the simple reason that we believe a pragmatic, active and risk-aware approach to portfolio management allows us to be well prepared for what we see as the inevitable turning of the credit cycle, and to capitalise on subsequent opportunities. Conversely, we believe there is good reason to believe that an eventual rotation in sentiment could cause significant challenges for those portfolios with a less active approach and/or consistently higher risk allocation.

At the time of writing, we hold more than 22% of the portfolio in ultra-high-quality AAA-rated corporate bonds, around 6% in Gilts, and have a modest allocation to cash which should enable us to cushion our investors from the worst effects of any negative shift in market sentiment, while providing us with the ability to rotate from this defensive ballast into riskier assets once any spread widening has occurred.

At the same time, it is important to emphasise that this is not a homogeneous asset class; as such, the detailed research work the team undertakes is enabling us to maintain exposure to credit risk in those areas where we believe there is still upside potential, such as in bonds issued by airport owners.

This tactically cautious approach has served us well in previous sentiment rotations, and we see few reasons why it should not continue to do so in the present environment.

Fund-specific risks

The fund can invest up to 20% in non-rated bonds. These bonds may offer a higher income but carry a greater risk, particularly in volatile markets. In difficult market conditions, it may be harder for the manager to sell assets at the quoted price, which could have a negative impact on performance. The fund may use derivatives which may result in large fluctuations in the value of the fund. Counterparty risk may cause losses to the fund. In extreme market conditions, the Fund’s ability to meet redemption requests on demand may be affected. The Key Investor Information Document, Supplementary Information Document and Scheme Particulars are available from Jupiter on request. This fund can invest more than 35% of its value in securities issued or guaranteed by an EEA state.

Important information

This document is for informational purposes only and is not investment advice. Market and exchange rate movements can cause the value of an investment to fall as well as rise, and you may get back less than originally invested. We recommend you discuss any investment decisions with a financial adviser, particularly if you are unsure whether an investment is suitable. Jupiter is unable to provide investment advice. For definitions please see the glossary at jupiteram.com. The views expressed are those of the Fund Managers at the time of writing, are not necessarily those of Jupiter as a whole and may be subject to change. This is particularly true during periods of rapidly changing market circumstances. Every effort is made to ensure the accuracy of any information provided but no assurances or warranties are given. Jupiter Unit Trust Managers Limited (JUTM) and Jupiter Asset Management Limited (JAM), registered address: The Zig Zag Building, 70 Victoria Street, London, SW1E 6SQ are authorised and regulated by the Financial Conduct Authority. No part of this document may be reproduced in any manner without the prior permission of JUTM or JAM.

Find out more