Article 3 / 4

Guide to mental health protectionGetting right blend of cover for mental health issues

Mental health issues are one of the most commonly cited reasons for claims.

According to latest data from the Association of British Insurers and the Group Risk Development (Grid) trade bodies, it is one of the top three most prevalent reasons why people submit an insurance claim.

In 2017, the data shows, 11 per cent of income protection payouts were for mental ill health claims.

And the 2017 Stevenson-Farmer review, Thriving at Work, claims this issue will only get worse.

The review suggests 300,000 people with a long-term mental ill health problem leave work or lose their jobs each year - at a much higher rate than those with physical health problems.

There is a problem building up here, as evidenced by an LV survey, with the average UK household having less than the Money Advice Service's recommended 90 days' worth of outgoings in savings, in case of emergencies.

LV's 2017 Income Roulette survey, carried out among 9,000 adults in the UK, found 37 per cent of people would not have enough savings, and 45 per cent of 25 to 34-years-olds in particular said they could only cope for one month or less without their income.

Most households do not have enough in ready cash in case of emergencies - but as Royal London's State of the Protection Nation research also showed, only 4 per cent of the population have some form of income protection.

It seems the financial resilience of Britons is weak at best - add to this the stress that comes with being financially unstable and it is clear the problem can only get worse.

So how can the group and individual protection market help more people suffering from mental ill health?

Group market

Financial advisers and healthcare providers have found there can be huge variations in the way some employers provide insurance cover and support services for mental health issues, and it can often be as a result of the type of employee benefit that is on offer.

According to Brett Hill, managing director of The Health Insurance Group, there has been a "traditional divide" between the employee assistance programmes (EAPs) offered alongside group income protection, and the provision of mental health support given by private medical insurance (PMI) policies.

Mr Hill says while income protection policies offer good support to staff with mental illness, these benefits are often not understood well by employers and therefore not communicated well to staff.

As a result, employees who need the support are unaware of the group risk policy and what help is available to them if they are in the scheme.

By contrast, more people understand the benefits of workplace PMI, and this is often communicated better - not least because of the tax position - but many PMI policies have not provided the sort of early intervention support needed where mental health conditions are concerned.

He explains: "EAP providers offer early intervention support and counselling, but EAPs are often poorly communicated to staff, so people may be unaware of the support available to them.

"Employees typically have greater awareness of PMI cover, if only because the benefit attracts a tax liability for them, but PMI may not always cover mental health conditions, depending on the benefits selected by their employer.

"Where it does, it would typically require a GP referral before a claim could be approved, which can create a barrier to access when GP appointments are difficult to obtain, and mental health conditions can come on suddenly."

However, Mr Hill believes this is starting to change, citing "developments in the PMI space that are bridging that gap, by extending benefits to include more accessible, earlier stage support services and treatments, which were traditionally associated with EAPs."

Assessing group claims

The benefit of early intervention and good support services are significant, as Katharine Moxham, spokesperson for Group Risk Development (Grid), points out.

She comments: "In terms of group income protection, while diagnosis is obviously important, the key factor considered in assessing a claim is whether or not (and how) it prevents someone from undertaking the day-to-day activities of their job.

"Through early intervention, case management and practical support, group income protection providers work with and support the employee, line manager and the business to help people back to work (through reasonable adjustments, mediation, role redesign etc), well before a claim payment even becomes due."

According to data from Grid's 2018 claims survey, published in April this year, both the cover itself and the benefits attached to it have helped many people, including a significant proportion of people with mental health problems.

The claims survey shows:

- 2,989 people were helped back to work in 2017 with active early intervention support from a group risk insurer.

- This represents 33 per cent of all claims submitted.

- Of the 2,989 employees who benefitted from some form of intervention, 52 per cent had help to overcome mental illness.

So it is not just about writing cover but also communicating what that cover might entail for both corporate and individual clients, and making sure that, at point of sale, the client knows what sort of support and payout they could reasonably expect with the cover they are buying.

The individual market

To ensure clients - whether corporate or individual - are given the best possible policies, with the best possible support for themselves or their employees, an adviser has to do some thorough investigations.

Sometimes this is harder with individual clients, many of whom might not like to discuss 'personal' health issues with their financial advisers, or perhaps the individual just can't think of any particular issue during the initial meeting with an adviser.

According to Phil Jeynes, head of sales and marketing for UnderwriteMe, part of the problem is getting enough information from the potential policyholder in the first place.

He says: "The biggest difficulty is in eliciting enough information from a customer to determine whether they have mental health issues which present a genuine underwriting risk, or whether they deal with stress as a natural part of life, like all of us, but are lucky enough that it never impacts on their lives to a significant degree.

"Inevitably, point-of-sale underwriting can only give you a snapshot of a person’s life; we can see the past quite clearly and can make educated guesses about the future, but they remain guesses nonetheless."

However, he says the types of question insurers ask are evolving to deal with this better and get a fuller picture of the customer, and this, together with the adviser's own questions and explanation, can go a long way towards helping people get the cover they need.

Assessing individual cover

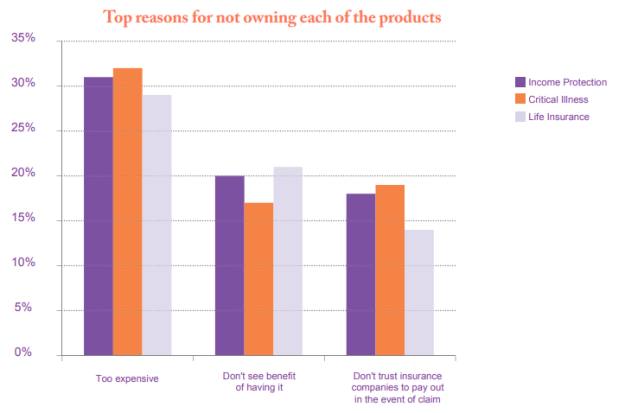

There is also the question of 'will it pay out'? Some people just do not think it is worth the price. As Royal London's State of the Protection Nation report showed last year, most people want to protect their families financially, but do not believe insurance policies are the way to do this.

Figure 1 shows the main reasons given for not taking out life insurance, income protection or critical illness cover.

Figure 1:

Source: Royal London

Some of the perceived problems cited by the Royal London research may not necessarily just be in the person's head when it comes to mental ill health conditions, says Alan Lakey, founder of CI Expert.

He believes while protection is crucial to help people, there has been a historic lack of product development and decent terms for people with mental ill health.

Mr Lakey explains: "There seems to be a knee-jerk reaction with underwriters where any indication of historic anxiety/stress/depression involves excluding future claims for related conditions (including ME).

"It also appears to many advisers that underwriters treat event depression - such as being depressed due to the death of a family member - the same as clinical conditions.

"This certainly seems an unfair methodology."

Advisers therefore have a doubly difficult role: to encourage clients to take out much-needed cover while also making sure the provider will not penalise the client for having any previous history of stress or depression.

Providers are aware of this and have been making efforts to improve the scope of their cover for policyholders with mental ill health, especially considering mental health conditions are not always permanent and can be treated successfully.

Transparency

According to Deepak Jobanputra, deputy chief executive of Vitality Life, flexibility and transparency are key.

He explains: "Getting the right diagnosis is the essential first step to ensuring the right help can be provided. As the awareness and understanding of mental health increases, individuals will hopefully recognise they need help and be encouraged to seek that help.

"With mental health issues taking many forms, protection products need to be flexible and transparent in order for customers to feel confident that they will get the right support at the right time."

For example, Vitality provides a range of support options from preventative help such as understanding the importance of sleep, exercise and nutrition, through to full psychiatric treatment.

He adds: "We also cover and regularly pay out on income protection for mental health issues. The protection industry needs to have a louder voice in communicating the range and variety of support it can provide and how essential it can be to the recovery process."

That said, there still seems to be a higher cost associated with cover for someone who may have had a period of absence from work due to stress, for example.

Scott Cadger, head of underwriting and claims strategy at Scottish Widows, comments: "Cover can be provided if more serious conditions are controlled with treatment but may have increased premiums.

"Stress and anxiety can usually be offered on normal premium rates or with small additional loadings."

Part of the reason seems to be a tendency for mental ill health to recur. Rob Harvey, independent protection expert at Drewberry, says: "The difficulty in covering mental health is that it can manifest itself in so many ways and many conditions can be comorbid, such as the relatively high incidence of people who suffer from anxiety who also suffer from depression.

"Therefore, someone who's had one mental health condition in the past before taking out a policy may find themselves excluded for claiming for all mental health conditions going forward, even if they go on to develop a different condition.

"I also think there’s a feeling among providers that diagnosing mental health conditions is far more subjective compared to physical ailments, making claims far harder to assess."

So while it is not impossible for advisers to get protection for individual clients, the greater onus on the individual to disclose all previous conditions could be met with higher premiums.

With group schemes, while some pre-existing conditions might not be covered, meaning an individual having a recurrent bout of mental ill-health might not be able to claim, at least the related support services can kick in sooner to prevent absence in the first place.

It is always worth finding out from individual clients whether their employers do offer any form of group protection in the workplace as a first port of call.

simoney.kyriakou@ft.com