Article 2 / 4

Investing in property & infrastructureProperty still key in diversified portfolios

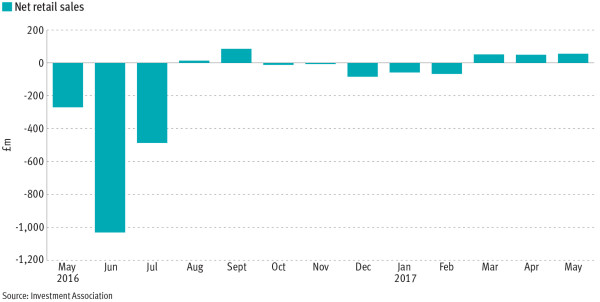

Open-ended commercial property funds have attracted a lot of negative publicity in the past year. But the market remains resilient 12 months after several funds were temporarily forced to suspend redemptions, despite the outcome of the general election and continued uncertainty surrounding Brexit.

Fund buyers and retail investors alike remain divided on whether managers were right to gate funds, and on the pros and cons of the asset class.

However, negative headlines following the referendum were driven by a fairly small segment of the overall market. Gating was a sensible move to protect remaining investors given the prevailing market conditions.

Comparisons between this period and the 2008 financial crisis were misleading, as acquisitions in recent years have largely been financed by equity capital and not debt. Commercial property values were equally still some 20 per cent below their pre-crisis peak.

Liquidity remains the well-documented drawback of commercial property in open-ended funds. The unit cost of many properties will be in the millions of pounds – each with unique characteristics, making the sales process complex and different from equities and bonds.

Investors can alternatively use real estate investment trusts, but this brings another element of volatility to a portfolio.

The outlook for the sector remains strong. Despite the current mixed sentiment, most large, well-diversified UK property portfolios (by sector, region, property type and tenant) with strong covenants should not see any significant increase in vacant properties, enabling them to continue to deliver robust yields.

Long-term leases, between five and 10 years with financially strong tenants, can offer the potential for predictable, regular income. Investors should expect rental income to make up most of their total return as capital growth can be cyclical.

Performance is generally less volatile as the value of a commercial property is largely based on the reliability of rental income. Volatility may also be reduced as performance is based on valuations, as opposed to transaction data, and this can underestimate market peaks and troughs.

The most important thing to consider when contemplating investing in a property fund is to ensure diversification within a portfolio. Hold it for the long-term, have sensible expectations and ignore short-term noise.

The UK commercial property market in which these funds invest is well-established and still offers relatively attractive transparency and greater liquidity than some markets, and depth and diversity of opportunities compared with other regions.

There are still very few retail funds that own global physical property. Advisers and investors will need to understand stages of the cycle, transparency of market, liquidity, legal system, property rights and tax regime before considering these products.

For patient investors with longer-term time horizons, commercial property still plays an important role in diversified portfolios. Most experts believe the market will deliver lower returns in comparison to recent years, but it still offers an attractive yield relative to bonds, with the potential for some capital growth.

While central London offices may be negatively affected during Brexit negotiations, other sectors such as industrial and logistics have much better prospects. A diversified portfolio will be important. Further sterling weakness is likely to attract more foreign investors into UK commercial property, boosting valuations.

Investors who do choose to hold commercial property over the next few years may see some volatility, but good active management focusing on well-located prime and good secondary property will potentially be rewarded over the long term.

Adrian Gaspar is a multi-asset investment specialist at Prudential Portfolio Management Group