PARTNER CONTENT by ARTEMIS

This content was paid for and produced by ARTEMIS

2025 vision: Three high-conviction predictions for long-term investors

Anyone can make predictions about the next 12 months (who knows – some of their predictions might even come true…) But on the Artemis Positive Future team we prefer to take a slightly bolder approach by looking back on what we are confident will have happened by the end of 2025.

While financial markets are unpredictable in the short term, the initial conditions surrounding us today make a number of developments over the next three years extremely likely. For example…

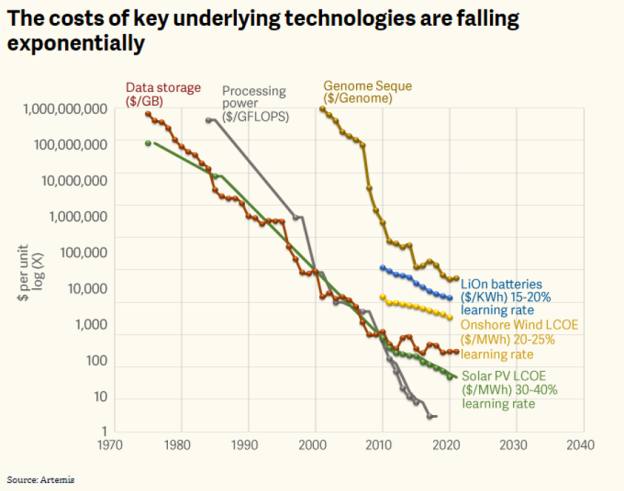

- computing power

- data storage

- solar panels

- wind turbines

- fuel cells

- heat pumps

- genome sequencing and

- battery energy storage

…will continue getting cheaper at highly predictable rates, driven by ‘Wright’s Law’ learning curves.

This is incredibly useful information to investors. It means we can confidently predict that many large and established industries will be disrupted and that most incumbents will struggle to adapt to technological shifts in the basis of competition. We can forecast that many of the companies that are building businesses around these structural transformations will create significant value for their shareholders, regardless of what interest rates are – or where inflation prints come in – over the next three years.

So when we settle back in our armchairs on Hogmanay 2025, put down our iPhone 17s and review three years of fascinating debate about inflation, interest rates and bond yields (all of which will have seemed vitally important to financial markets at the time), what will actually seem important? What will really have changed?

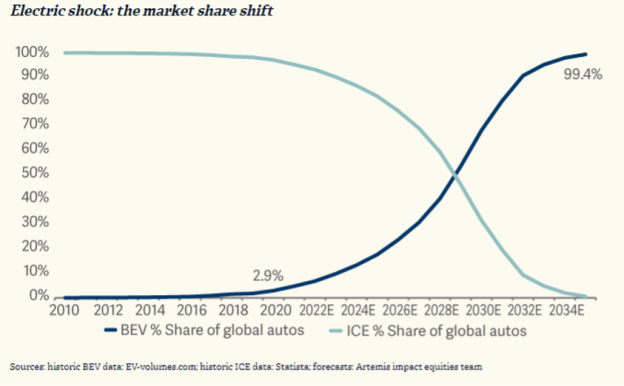

1. Battery electric vehicles become the mainstream choice

Over the next three years, the cost of battery electric vehicles (BEVs) will come close to undercutting those built around internal combustion engines. That is not wishful thinking on our part. Our conviction is based on predictable learning rates which make further increases in the range of BEVs – and a decline in their costs relative to those powered by internal combustion engines (ICEs) – inevitable. As relative costs fall, sales will rise. Like it or not, as ‘cybertrucks’ designed to appeal to America’s appetite for super-sized vehicles begin to roll off the production line – the addressable market for zero-emission vehicles will expand in lockstep.

That will create a negative cycle of diseconomies of scale for legacy auto manufacturers as demand shifts away from their largest source of revenue – combustion engines – and as the factories that make them become structurally underutilised. Companies that fail to pivot to this new drive-chain technology are at high risk of bankruptcy. Companies that are optimised around BEVs – or whose technology underpins infrastructure such as charging stations – have an opportunity to prosper.

2. The ‘artificial pancreas’ starts to offer practical, daily help to diabetics

Over the next three years, emerging and existing technologies will continue to converge, creating new opportunities to solve significant problems facing the global economy such as climate change, lack of access to education – and the daily challenges faced by millions of diabetics.

537 million adults worldwide currently live with diabetes. That is predicted to rise to 643 million by 2030 and to 783 million by 2045. Over $1 trillion is spent on diabetics each year in the US – or one in every four dollars of total healthcare spending. Yet while the outlook may appear bleak, disruptive technology has the power to create positive-sum outcomes…In the absence of an outright cure, technology is on the brink of creating automated devices that will effectively manage diabetes without intervention. These devices will:

- monitor glucose levels and deploy insulin accordingly.

- improve long-term health outcomes and reduce anxiety.

- be discrete, needle-less and tube-less.

- be rugged enough to wear whilst playing contact sports.

- be sufficiently waterproof to wear while showering or swimming.

- connect to the cloud and be managed through your smartphone.

- be clinically approved, available globally and cheap enough for healthcare systems and patients to afford.

Moving into 2023, we have the prospect of discrete automated insulin delivery (AID) devices such as Insulet’s Omnipod 5 providing:

- accurate continuous glucose monitoring,

- tubeless insulin pump patch delivery,

- controllable via smartphone.

By 2025, the affordability of these devices will have improved, widening access and enabling their users to engage in basic activities of everyday life without having to think about their diabetes.

3. The exponential growth of ‘clean tech’ severs the centuries-old link between economic growth and fossil fuels

Since the 18th century, economic growth has been driven by the burning of fossil fuels. At some point in the next three years, that link will be permanently severed, with profound consequences for the climate, the global economy – and for the energy companies that are being disrupted.

The fact of the matter is that – unlike renewables – fossil fuels do not benefit from Wright’s Law; while prices of coal, oil and gas have exhibited huge volatility, there has not been any long-term downward trend in their cost. In fact, a paper published by the Institute for New Economic Thinking at the Oxford Martin School showed that, after adjusting for inflation, prices of fossil fuels today are roughly where they were 140 years ago…. As the Red Queen in Alice Through the Looking Glass observed, no matter how fast they have run, they have stayed in the same place.

Total electricity generation from renewables hit a record high of 8000 TWh in 2021, representing over 29% of the mix. This is certain to have been beaten in 2022, as the past 12 months brought dramatic improvements in the relative cost of clean energy. Meanwhile, unprecedented response from governments around the world to the energy crisis provoked by Russia’s invasion of Ukraine, including…

- the Inflation Reduction Act in the United States

- the Fit for 55 package and REPowerEU in the European Union

- Japan’s Green Transformation (GX) programme and

- Korea’s aim to increase the share of nuclear and renewables in its energy mix

… have brought forward the point at which demand for fossil fuels peaks and goes into irreversible decline. Global economic growth has been tied to fossil-fuel consumption since the Industrial Revolution. Over the next three years, this link will be broken. We are positioning our client’s capital to profit from this pivotal moment.

Article by Craig Bonthron. Craig is part of Artemis’ impact equities team.

FOR PROFESSIONAL INVESTORS AND/OR QUALIFIED INVESTORS AND/OR FINANCIAL INTERMEDIARIES ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS. This is a marketing communication. Refer to the fund prospectus and KIID/KID before making any final investment decisions. CAPITAL AT RISK. All financial investments involve taking risk which means investors may not get back the amount initially invested.

Investment in a fund concerns the acquisition of units/shares in the fund and not in the underlying assets of the fund.

Reference to specific shares or companies should not be taken as advice or a recommendation to invest in them.

For information on sustainability-related aspects of a fund, visit www.artemisfunds.com.

The fund is an authorised unit trust scheme. For further information, visit www.artemisfunds.com/unittrusts.

Third parties (including FTSE and Morningstar) whose data may be included in this document do not accept any liability for errors or omissions. For information, visit www.artemisfunds.com/third-party-data.

Any research and analysis in this communication has been obtained by Artemis for its own use. Although this communication is based on sources of information that Artemis believes to be reliable, no guarantee is given as to its accuracy or completeness.

Any forward-looking statements are based on Artemis’ current expectations and projections and are subject to change without notice.

Issued by Artemis Fund Managers Ltd which is authorised and regulated by the Financial Conduct Authority.

Find out more

Related Content