Article 4 / 4

Guide to the return of subprimeHow to help complex clients onto the mortgage ladder

Advisers and brokers with clients who may be described as credit impaired or who have more complex borrowing needs must ensure they are not left at risk of missing repayments.

Getting the right mortgage deal is vital, regardless of a client’s financial history but especially given that, as Charlotte Nelson, press officer at Moneyfacts points out, the cost of mortgage deals aimed at those with a tarnished credit history “can be significantly higher than standard deals in the market, reflecting the extra risk that is involved”.

While the low interest rate environment has prevailed in the UK for some time, there is also the threat that the Bank of England’s monetary policy committee (MPC) will begin raising interest rates more aggressively and quickly this year and in 2019.

David Torpey, chief operating officer at Bluestone Mortgages, says: “Brokers should think carefully about their clients’ current and expected monthly expenditure, and make sure they have a realistic surplus amount saved to protect themselves against any future interest rate rises.”

Credit check

But there is an onus on clients too.

Ms Nelson suggests those who are unsure about their credit history can start by checking their credit score online, with many companies offering free reports.

“If there are any errors, contacting the relevant companies is a must, to correct the report and try to improve the credit score,” she explains.

“Any mortgage seeker considering a credit impaired deal should seek advice from a financial adviser to see if it is financially viable to get such a deal, and whether it is the best choice for them.”

This is especially true for those with an adverse credit history as consumers tend to rely on searching the mortgage deals offered by the high-street lenders.

But it is, more often than not, the smaller specialist lenders and building societies who are offering a wider range of products for the credit impaired market.

Mr Torpey adds: “Consumers should be encouraged to look around and use a specialist mortgage broker to ensure they can secure the best possible mortgage deal and assess their application on a case-by-case basis.”

This means those potential borrowers who do not seek advice from a broker or financial adviser could be left believing there are no mortgage deals out there for them.

Beyond the banks

Jeremy Duncombe, currently director of the Legal & General Mortgage Club, acknowledges there is a significant amount of work to be done on educating clients generally.

“Our latest research shows that over half of consumers are unaware that a mortgage broker can offer greater product choice than a bank or building society,” he warns.

“It is therefore up to us to promote the benefits that brokers can offer. If we can encourage borrowers to speak to a mortgage broker about the different options on offer, we can ensure that they are getting the support of professional advice when making the biggest financial decision of their lives.”

A number of government schemes have been launched in recent years which can also help clients get onto the property ladder without stretching themselves financially.

Mr Duncombe suggests: “Brokers should educate their clients on the variety of schemes available which can help first-time buyers onto the property ladder.

“Shared ownership, Help to Buy, or even support from the Bank of Mum and Dad can give potential buyers the boost they need to secure homeownership.”

Making clients aware of these schemes and whether they are eligible could help those credit-impaired borrowers who are buying for the first time.

The two best-known schemes are Help to Buy: Equity Loan and Help to Buy: Shared Ownership.

The former means it is possible for someone with a 5 per cent deposit to purchase a property, while the latter scheme also requires a lower than usual deposit.

Under the Shared Ownership scheme, buyers are able to purchase as little as 25 per cent or as much as 75 per cent of their home and then pay rent on the rest.

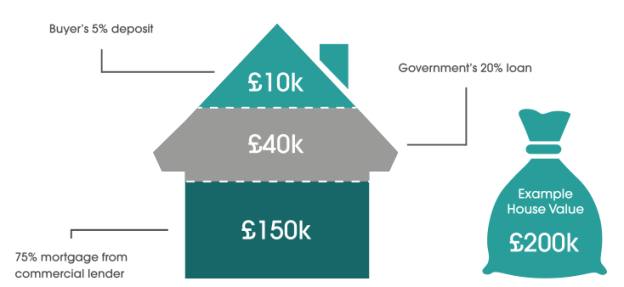

Figure 1: Help to Buy Equity Loan - example for a home with a £200,000 price tag

Source: www.helptobuy.gov.uk

Ray Boulger, senior technical mortgage manager at John Charcol, explains: “The Help to Buy equity share second charge scheme helps to reduce risk as mortgage payments are much lower for the same value property and, as the government shares in any increase or decrease in the value of the property, only part of the reduction in value falls on the purchaser.”

The Help to Buy Isa offers another avenue for first-time buyers to save a deposit as each payment into the Isa receives a government top-up of 25 per cent of the savings, up to £3,000.

Knowing what options are open to them is part of the process for borrowers with adverse credit.

Being aware of the risks associated with having to pay a mortgage each month is also important, but being able to remove any risks entirely is unlikely.

Mr Boulger admits: “One can’t completely eliminate risk, but it can be mitigated by sensible financial planning for known events which would result in a reduction of income – such as starting a family – and unplanned events, such as redundancy, by keeping readily available savings of, say, three months’ expenditure.”

eleanor.duncan@ft.com