The decision to hedge or not to hedge overseas equities will lead to a wide dispersal in returns for pension providers in 2016.

While most are yet to declare their results for the 2016 calendar year, their results are set to diverge as there is a wide variety of practices among pension schemes catering for auto-enrolment.

Now: Pensions has a 100 per cent hedge on overseas investments, Legal & General a 50 per cent hedge, while the People's Pension and Nest do not hedge.

Subsequently, Now:Pensions has reported a 10.8 percent return for the year, while the People's Pension has reported a 20.5 percent return.

Edward Park, investment director at Brooks Macdonald, said with sterling falling by almost 15 per cent on a trade weighted basis during 2016, those investors that have not hedged will have gained a large windfall from the value of their overseas assets rising in sterling terms.

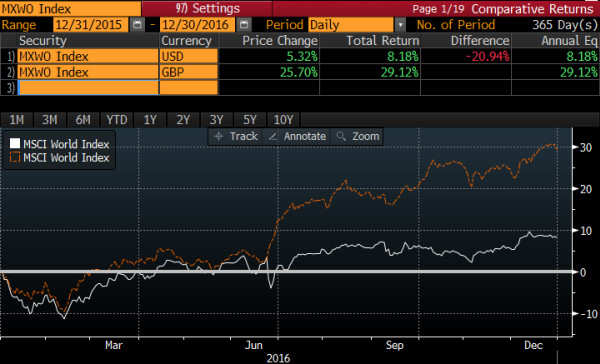

The difference can be seen in the returns for the MSCI World index, which recorded returns of 8.1 per cent in 2016 in US dollar terms, the value of this in sterling terms is 29.1 per cent after currency movements are taken into account - giving an extra 21 percentage points of return.

This could mean an extra 10.5 per cent total portfolio return for a fund that has a 50 per cent passive global equity exposure, compared to a fully hedged fund holding the same assets.

Mr Park said that with the majority of private clients’ liabilities being sterling denominated, the lowest risk approach to investing a pension or other portfolios would be to hedge all foreign exchange risk.

For this reason Brook Macdonald hedges its fixed interest investments that target a steady return, but for overseas equities his firm's default position is to be unhedged.

He noted the currency fluctuations had also impacted FTSE 100 returns in 2016, which outperformed mid-cap stocks owing to the index’s constituents being large multinational companies with a high proportion of foreign-currency earnings.

Some institutional investors that have not hedged their overseas equity exposure are now considering putting one in place to profit from an expected mean reversion in sterling.

Roger Hallam, chief investment officer for currency management at JP Morgan Asset Management, said: "Sterling looks cheap from a long term valuation perspective and if you believe currencies mean revert to their value, it does make some sense that you would [be] hedging up your foreign asset exposure if you were a sterling based investor."

However, he warned that sterling could fall further.

"Our view is that sterling could underperform a bit further, the Brexit process is going to prove challenging and the UK is vulnerable from a balance of payments perspective."

Mark Dampier, head of research at Hargreaves Lansdown, warned that forecasting the direction of currencies was very difficult and that it was best for most investors not to hedge at all for this reason.

"I have a simple view that the more decisions you make the more likely you are to cock it up," he said, adding that where currency hedging is discretionary for fund managers, "nearly all get it hopelessly wrong."

david.rowley@ft.com