PARTNER CONTENT by SCOTTISH WIDOWS

This content was paid for and produced by SCOTTISH WIDOWS

Customer segmentation at retirement

Putting a rigorous process in place.

Imagine a cautious 66-year-old using drawdown for income, and a 35-year-old, however cautious, saving with an ISA. The two are unlikely to be well served by the same process and investments. For clients who intend to use drawdown, the industry is now moving to a more structured governance approach: a Centralised Retirement Proposition (CRP).

Many of the drawdown clients of today would formerly have used annuities. Of those wanting flexible access, a number have lower net worth, lack investment experience and are more likely to have a limited capacity to withstand loss.

Sustainability for all

It used to be that unrestricted access to drawdown was only for those with a minimum fund value of £100K+, but this is now clearly a thing of the past. The absence of such natural barriers means advisers now have a responsibility to ensure that they recommend sustainable withdrawal strategies whatever the level of wealth.

With a CRP, advisers can create a structured investment advice process. Like a Centralised Investment Proposition (CIP), a CRP creates consistent, repeatable and deliverable outcomes for diverse types of clients. Good governance not only helps reduce business risks but also improves the ability to service the larger volumes of clients needing retirement income.

The CRP process

The process above can be applied equally to all customers; with the major exception being stage 3: the investment strategy.

The FCA continues to make reference to the appropriate use of of CIPs, and it’s just as applicable to CRPs: “Where a firm has a diverse client bank, it may wish to consider segmenting their clients. This involves offering a range of CIP solutions to meet the needs and objectives of different client segments.”

The stage of the process that is most likely to differ between clients is the investment strategy. Especially when the complexity of their needs, their levels of wealth and their investment experience diverge significantly.

By employing differing investment strategies, firms are able to meet those varying requirements and objectives.

Cost and price sensitivity also need to be taken into account. This gives the opportunity to develop different investment strategies that provide a suitable balance between your clients’ ability to accept the costs, and the viability to deliver a profitable service.

Loss aversion

Although your clients have differing needs that can be segmented using objective measures such as wealth and experience, there may be more subjective attributes that help group similar clients. One aspect that may unite many of them – a trait independent of their level of personal wealth – is the wish to protect, against loss, the savings they’ve already acquired.

The link between objectives and solution

Clients may have many requirements and – with the advent of greater pension freedoms – many options available to them. So it’s important to have a number of contingent strategies in place.

Despite their diversity, clients can be grouped together for the purposes of a shared investment solution by:

• objectives

• wealth

• complexity of their needs

• experience and attitude

• risk aversion.

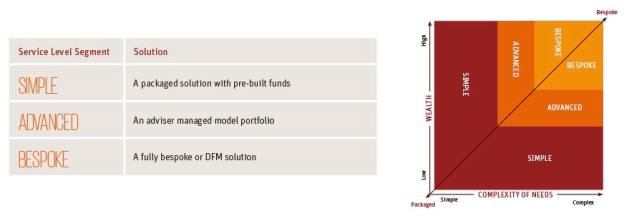

The groupings can be used in conjunction with each other; in the way that “wealth” and “complexity” have been combined in the investment strategy below.

Aligning an investment approach

Following segmentation, appropriate and – above all – practical levels of service and investment approach need to be chosen, to fit both your clients and the ethos of your company.

A bespoke investment service is one that higher-value customers, who generally have more complex requirements, are accustomed to receive. This is equally true of those who have substantial experience and complex finances.

The correlation between wealth and complexity gives greater scope for sophisticated bespoke solutions based on DFM. However, higher wealth is not exclusively restricted to a more complex solution. If the client has straightforward needs and maybe lower financial experience, why load unnecessary cost and complexity?

The greater challenge comes from lower-wealth customers wishing to remain invested.

Lower-wealth clients

Many clients with smaller pension pots now demand the flexibility provided by drawdown. Although their resources don’t command a bespoke investment approach, they nevertheless need sound strategies that provide the opportunity for real growth and for their pensions to be as sustainable as possible.

This creates a delicate balancing act between service, cost and effectiveness.

Single multi-asset fund

For many of these drawdown clients with modest retirement savings and simpler needs, multi-asset funds are an obvious attractive investment solution. They offer a combination of the benefits of equities with the potential returns of other asset classes: namely bonds, property and absolute return.

Therefore the growth potential comes with reduced volatility – due to diversity. However, even highly diverse portfolios are not immune from volatility; which is widely agreed to be the biggest enemy of sustainable drawdown. The good news is that innovation is now starting to deliver results for drawdown investment strategies to help pension pots last longer.

CRP provides the blueprint

Clients will always be hugely varied, and matching the right service to the right client will continue to drive innovation. But, with a CRP process in place, you’ll be able to attend to their needs as efficiently and effectively as possible – whatever their circumstances.

For further insight and expert guidance, please visit Scottish Widows Change Hub.

‘This is a Scottish Widows Paid Post. The news and editorial staff of the Financial Times had no role in its preparation’

Find out more

Related Content