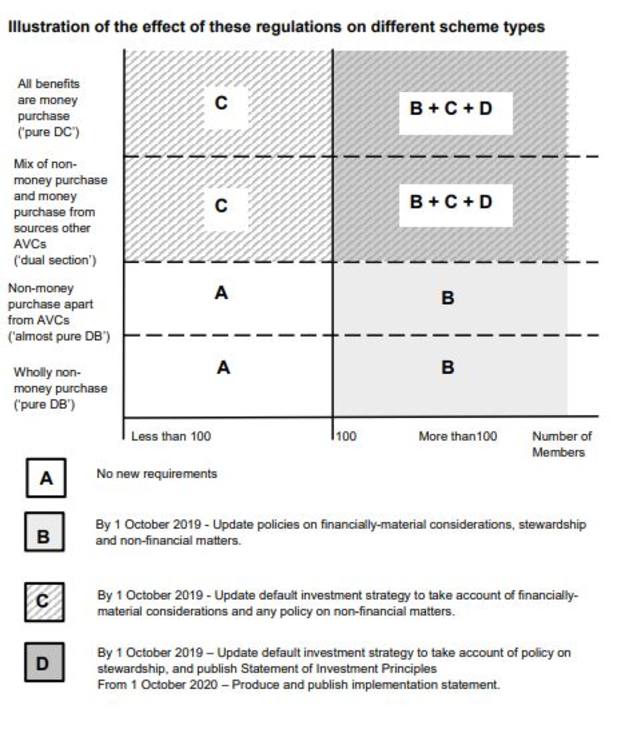

Pension schemes with more than 100 members will be forced to disclose the risks of their investments, including the ones arising from environmental, social and governance (ESG) considerations, by 1 October 2019.

Until now, trustees were obliged to state the extent to which they take ‘social, environmental or ethical considerations’ into account in the scheme's statement of investment principles.

According to new rules, published by the Department for Work & Pensions (DWP) today (11 September), trustees of both defined benefit (DB) and defined contribution (DC) plans will have to state their policy on taking account of "financially material" considerations, including ESG factors, such as climate change.

In its response to a consultation launched in June, the DWP set the timeline for the introduction of the new rules, which also mandate trustees to set out the pension fund policy on stewardship (the exercise of voting rights and influence on the management of investments), for 1 October 2019.

DC schemes will have other requirements to comply with by that date, such as to publish their statement of investment principles on a website available to the public, and to signpost members to it via their annual statement.

The plans will also have to prepare or update their default strategy to set out how they take account of financially material considerations, including those arising from ESG.

Guy Opperman, minister for pensions and financial inclusion, said it remained government policy not to direct the investment decisions or strategies of schemes but he said given the time horizons of pension saving, "broader considerations are likely to present long-term financial risks and opportunities to the solvency of DB schemes and the value of members’ DC (and in time Collective DC) pensions".

From October 2020, DC trustees which publish an annual report, will have to prepare a statement setting out how they have implemented their investment policies, and explaining any change made to them, the DWP said.

This statement must be included in the annual report, and signposted to members in their annual benefit statement.

According to Catherine Howarth, chief executive of campaign group ShareAction, the new rules are "a major development".

She said: "We commend the government on this action to protect UK pension savers.

"Working people in the UK deserve 21st century risk management of their retirement assets and investment strategies that anticipate the impacts on portfolios of issues like climate change. They also deserve to be heard by the trustees and investment professionals looking after their savings.

"These regulations are a big step forward in shifting the culture and practice of the UK pensions sector, and we warmly welcome them. It is now over to the Financial Conduct Authority to ensure savers in schemes it regulates are given similar information and protection."

Ralph McClelland, partner at Sackers, said the DWP has put a "firm marker down for trustees on their responsibilities regarding ESG risks".

He said: "While some trustees have been working to integrate ESG into their investment strategies for many years, we know a number have found the law unhelpful and unclear.

"By including a clear requirement to articulate a policy on ESG considerations (including climate change), we think the DWP will have removed much of this uncertainty.

"As a law firm which has advised trustee boards over many years, we are seeing a new level of engagement in these topics from trustees, investment consultants and investment managers, so this intervention is very timely."

maria.espadinha@ft.com