Article 2 / 4

Guide to finding yield globallyHow far up the yield curve should investors go?

Generally speaking, the higher the yield, the more risk an investor is taking because the quality of the credit is lower.

Ben Edwards, fixed income manager at BlackRock, explains investors need to think about two distinct curves when investing in bonds.

“Firstly, the credit curve, which is generally well understood – the lower the quality of the issuer, the higher the yield. That higher yield compensates investors for an increased probability that a company will fail to meet its financial obligations,” he says.

“Less well understood is the important effect the maturity curve can have on the returns of bonds.

“Irrespective of the current quality of a particular company, its revenues, costs, management team, strategic direction and financial policy all become less certain as time goes on. For this reason, corporate bonds tend to pay a higher yield for longer maturities.”

He explains how this works in practice, using corporate bonds as an example.

“The longer end (those with maturities above 15 years) of the sterling corporate bond market offers a poor risk/reward trade off,” Mr Edwards notes. The additional compensation to own a BBB sterling bond with a maturity of 30 years is only 0.3 per cent higher than that of 15 years.

“For that, investors take on additional asset volatility and give up considerable certainty of the direction of the company. That additional yield could more easily be captured by buying seven-year bonds rather than five-year bonds, for example.”

He continues: “And for that reason, the six to 10-year part of the maturity curve offers strong relative risk-adjusted returns.

“By selecting bonds whose yields are expected to fall more quickly as they progress toward maturities, investors can earn above-market returns and avoid the volatility of longer maturity bonds.”

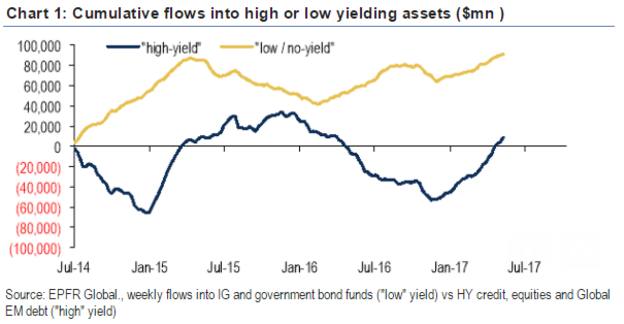

Figure 1: Cumulative flows into high or low yielding assets ($m)

Source: EPFR Global, BofA Merrill Lynch

Predicting the future

But given investors have become used to being in a bond bull market for many years, what should they expect from future returns from bonds?

With such a close relationship between interest rates, inflation and bonds, investors will have to consider their duration positioning, as Ben Willis, head of research at Whitechurch Securities points out.

Those who believe interest rates are on an upward trajectory will be positioned differently from those who think interest rates will stay where they are or get lower.

Mr Willis says: “If you believe that interest rates and/or inflation numbers are going to increase more rapidly than consensus, then you will be focusing on short duration bonds and will be prepared to accept a lower yield as your concern will be a drop in bond prices.

“Of course, the opposite to this scenario is also true, and you would seek out longer dated bonds where you may be able to pick up some higher yield.”

He cautions: “However, the outlook for bond markets remains uncertain, although the backdrop does appear to be moving into a new phase. Having experienced several years of low growth and low inflation, combined with monetary stimulus and emergency interest rates, you could have invested anywhere in bond markets over the last eight years or so and you would have received equity-type total returns.

“Investors should not expect this to continue. Inflation numbers are ticking up, economic growth is proving robust and the US has already started on a rising interest rate cycle.”

Both US and UK central banks are trying to keep a lid on inflation. Having targeted 2 per cent inflation respectively for the past few years, the Federal Reserve and the Bank of England (BoE) are adjusting interest rates higher to contain the inflationary environment.

The US Federal Reserve has only raised interest rates three times since 2008, with the latest move in March this year taking the base rate from 0.75 per cent to 1 per cent.

Meanwhile, in the UK the BoE held the base rate at 0.25 per cent in March, although CPI inflation picked up to reach 2.7 per cent in April – its highest level in 2013 and exceeding the bank’s target.

Up the curve

Nicolas Trindade, senior portfolio manager at AXA Investment Managers, believes with the yield curve relatively flat at the moment by historical standards, the pick-up investors can get by going further up the curve is limited.

“Also, with yields set to rise on the back of higher growth and inflation, investors should avoid extending maturities and instead consider adopting a short duration approach,” he adds.

But Martin Horne, head of European high yield investments at Barings, suggests the high yield market has historically adjusted quickly to rising interest rates.

He observes: “Interest rate rises are typically accompanied by robust economic conditions, which in turn lead to spread tightening, a positive catalyst for the pricing environment of fixed rate bonds.

“While the exact timing on interest rate rises appears uncertain, central banks today seem keen to ensure policy movements do not cause negative market disruption, which will likely translate to near-term developed market movements that are proportionate and well-flagged.”

Certainly, any rate rises have so far been well signaled and many are predicting the Fed is preparing to hike again at its meeting later this month (June).

“Regardless, high yield carries significantly less interest rate or duration risk than many other fixed income markets,” Mr Horne notes.

“And while we would advocate portfolios not being too centered in long maturity bonds, particularly in the context of Europe where the curve looks the flattest, we think the overall disruptive effect of the curve will be relatively short-lived and may offer a significant investment opportunity amid a strong corporate earnings backdrop.”

Ultimately, investors need to have a good understanding of their own risk and reward limitations before deciding where to sit on the yield curve.

Lombard Odier’s chief investment strategist Salman Ahmed claims with yields so low, it is risky to search for yield by extending duration still further.

He adds with yield curves as flat as they are, the compensation for doing so is meagre, “meaning the correlation between interest rate risk and yield has broken down to the disadvantage of investors”.

“In our view the true ‘sweet spot’, especially for more conservative investors, is in ‘crossover credit’ – corporate bonds rated at the lower end of investment-grade (BBB) and the higher end of high-yield (BB),” Mr Ahmed explains.

“Lower-rated bonds offer higher yields and a better balance between duration and credit risk than investment-grade bonds.”

eleanor.duncan@ft.com