Article 1 / 4

How to build a robust yield into a portfolioHow to find yield in this environment

Globally, government bond real yields are low, central bank manipulation has meant indiscriminate, price-insensitive bulk buying, spreads are tightening and the past decade’s hunt for income has seen so many people allocate to fixed income that liquidity is now a problem.

And yet, despite these signs, people like fixed income.

According to data from the Investment Association (IA), fixed income funds saw a surge of popularity in March 2017.

The data shows fixed income was the third best-selling asset class, with net retail sales of £720m. Overall, fixed income funds were the second-best sellers of the first quarter of the year.

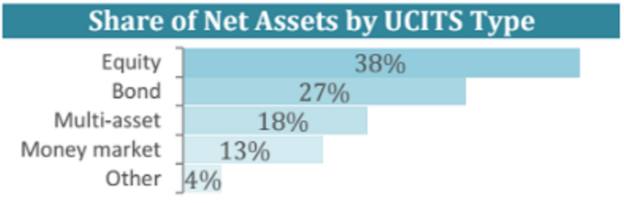

This isn’t just a trend local to the UK. Across Europe, bond funds have been popular with investors; the below graphic from European Fund and Asset Management Association (EFAMA) shows how strong the appeal

In March alone, according to data from the EFAMA, bond funds saw inflows of Euro 32bn, up from Euro 22bn in March. In terms of share of net assets, bond funds were at 27 per cent, compared with 38 per cent for equities.

So what is driving the popularity of the asset class?

Bernard Delbecque, senior director for economics and research at EFAMA, comments: “The upward trend in net sales of Ucits continued in March, thanks to bond funds, which enjoyed their highest monthly net sales ever at a time when investors are looking for return without increasing their exposure to equity markets too much.”

The answer: perceived safety compared with equities, and the lure of a ‘fixed’, quantifiable, regular income in the form of a coupon. People like the idea of a reliable yield without the higher volatility of investing in equities.

However, more recently, the 146-strong IA Global Bond sector has seen average fund performance start to stall after an exceptionally strong run.

Yet over one year, the average global bond fund has returned 8.1 per cent (bid-to-bid, net income reinvested, according to FE Analytics). This compares with the average IA Global Equity Income fund has returned 28.1 (again, net income has been reinvested). All data is at 26 May 2017.

Global bond fund performance seems to have stalled as inflation rises, a tightening US monetary policy cycle starts to impact on US growth, politics and a general global slowdown have come to the fore.

Higher popularity; higher price

So despite the popularity, we are in a tougher environment for bonds, with too many investors chasing too little yield, paying too much for their fixed income exposure, suffering from compressed yields in developed market bonds and experiencing a poor outlook for inflation.

Says Patrick Connolly, head of communications for Chase de Vere: “Many fixed interest assets are expensive, and so yields are correspondingly low.

“This creates a real challenge to advisers, who are looking to construct and manage client portfolios.

“If they focus too much on yield, they risk being over-exposed to riskier fixed-interest investments, and lower-quality high-yield bonds.

“While this would produce a higher yield, it also is likely to give greater levels of volatility and potentially significant, shorter-term capital losses.”

This is especially so in the UK, where inflation at 2.7 per cent now outstrips the yield on a 2-year and 5-year government bond (gilt), at 1.75 per cent and 0.5 per cent respectively, according to Bloomberg Data.

Data from the FT shows how the UK gilt yield has dropped off a cliff in recent months.

Gilt yield since 2014 on 10-year UK government bond (source: FT.com)

But while a good yield is hard to find in the more traditional markets, fixed income managers have been able to find some great opportunities by looking further afield and considering reducing duration to mitigate volatility and higher interest rates.

Chris Iggo, chief investment officer of AXA Investment Managers, says: “Investors could benefit from looking further afield for income.

“As well as high yield and financial corporates, today we see opportunities in emerging market debt, for its diversification benefits, improving macroeconomic picture, and the fact that emerging market yields and spreads appear attractive relative to developed markets.”

He adds: “If portfolio volatility is an important consideration, a short-duration approach could be particularly appealing to mitigate the impact of rising interest rates.”

Moving up the risk curve

Eugene Philalithis, portfolio manager of the Fidelity Multi-Asset Income Fund, comments: “Our favoured areas so far this year are local currency emerging market debt (EMD), US and European loans and [contingent convertibles] CoCos, which tend to be issued by European banks.

“Local currency EMD, for example, is a reasonably defensive way to play the ongoing strength in emerging market economies, with many currencies also relatively cheap compared to the past five years.”

Nicholas Wall, manager of the Old Mutual Global Strategic Bond Fund, likes looking further afield, particularly because many ‘hunt for yield trades are overcrowded and mature’, and volatility hasn’t been tested for a long time – so investors need to make sure they can ‘tolerate liquidation periods’ and are not forced into selling into these overcrowded and mature markets.

His fund likes “idiosyncratic opportunities where the narrative is compelling and the securities are under owned, so you are not caught in a squeeze for the exit.”

Mr Wall particularly likes Portugal and Argentina, and subordinated financials in Europe, but is avoiding investment grade bonds.

He adds: “If these sovereigns are too risky for your portfolio, then take advantage of the low implied volatility to hedge more conventional plays through options.”

Regarding his previous comment, Argentina has defaulted eight times since 1824, when it issued its first bond.

In the US, as in the UK and other developed economies, monetary spreads are narrower and the currency weaker, which are acting as further dampener effects on bond yields. Many corporate bonds are reflecting the yield compression on sovereign bonds, causing investors to question how far up the curve they should go to get yield.

“Yield is getting harder and harder to come by,” says Darius McDermott, managing director of Chelsea Financial Services. For him, yield can be found outside of traditional government or investment-grade bonds.

He comments: “There are some pockets of value left in selected high yield bonds – particularly in financial subordinated debt.”

This poses a question for Mr Iggo, who says the challenge for bond investors at the moment is how much risk to take to get as high a yield as possible.

“It is frustrating to end investors that income yields are so low across asset classes, but the reality is yields are so low and income return is more difficult to get, which tends to lead to the paradox of higher savings rates. To get the same income, you need to save more when yields fall.”

Popularity of high risk?

So higher risk strategies might become more popular, as these come with a commensurately higher level of return as compensation for the risk attached. But as Mr Iggo points out: “Some strategies try to boost the income they deliver to investors by taking on more risk, or by leverage.

"That can work but the risk to capital is higher.”

He explains: “It is possible to get north of 10 per cent yield in the bond market – the CCC-rated bucket of the European high yield market currently has a market-cap-weighted yield to worst of 11.1 per cent; the equivalent in the US has a yield to worst of 9.8 per cent.

“But with that comes a historical default rate, which has typically been around 25 per cent a year.” He asks whether investors can really risk a one-in-four chance their money will be lost through defaults?

Therefore, taking more risk to get more yield is not always going to be the best way to find income in 2017 from the bond markets.

Looking around

For Chris Leyland, deputy chief investment officer for Newcastle-headquartered True Potential, finding yield is also about looking for alternative ways of finding income.

He comments: “Our investment management partners have a broad skill set and global reach, which means they can access non-traditional income drivers, such as convertibles and preferred stocks.

“They can also dive into areas such as emerging market debt, and energy and infrastructure bonds.”

He said yields may vary, but levels above 5 per cent are not uncommon, because of the higher risk in these areas.

But you don’t have to go too far out to find yield, even in a global environment of tighter spreads and low liquidity. Mr Leyland says: “Investments in non-traditional areas can be blended with traditional income-producing investments, such as government bonds and better quality corporate debts.”

However, to find the right blend of fixed income, Mr Leyland believes it is important to “incorporate bottom-up, fundamental, relative value and macro viewpoints, which matter a great deal when looking for yield.”

Dan Ivascyn and Alfred Murata, managers of the Pimco Income Fund point out, however, that the global fixed income market is huge – currently US$100trn in size, so there are many different sectors available for managers to take advantage of to help generate income and try to preserve capital.

Mr Ivascyn says: “The ability to be opportunistic is important when trying to capitalise on dislocations.

“The fund can tactically shift portfolio weightings across sectors with attractive yields and risk-adjusted returns in this increasingly complex and volatile investment environment.”

simoney.kyriakou@ft.com