The energy sector has proved more unpredictable than most for investors over the past three years, with ongoing supply and demand issues causing fluctuations in the price of oil.

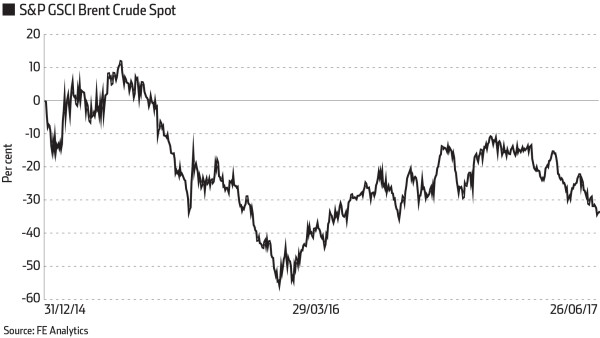

The S&P GSCI Brent Crude Spot index is down 10.5 per cent in the past 12 months to June 26 in sterling terms, data from FE Analytics shows. The most recent decline began at the end of December 2016. It has seen the index lose 24 per cent year to date, and drop more than 8 per cent in June alone.

All eyes have been on Opec amid these falls, as the group of oil exporting countries aims to contain the supply of the commodity from places such as Saudi Arabia and Russia.

Rob Crayfourd, portfolio manager at New City Investment Managers, says challenges remain for the cartel, although he sees the price of oil – currently hovering at close to $45 a barrel – staying in the $45-55 range for now. Most concerning, he believes, is an increase in group members failing to adhere to quotas, with Iraq likely to be the first to break ranks.

“Most notably, Saudi Arabia is transitioning to a fiscal breakeven of $40 barrels by 2020 and so is likely to increase its production levels in 2019-20 as it is unhappy about handing market share to the US,” Mr Crayfourd explains.

“The US has become the de facto swing producer due to US shale oil production being able to come on-stream in a relatively short period of time and at relatively low cost of production.

“US shale production has changed the landscape for global oil production, as US onshore producers will now act as the swing producer, with an ability to rapidly bring on production when oil is at $50 [a barrel] and above,” he adds.

But Thomas Benedix, portfolio manager at Union Investment, believes the supply discipline asserted by Opec is working.

Mr Benedix says: “Opec production restrictions and the seasonal increase in demand will create an oil market deficit in the second half of the year – regardless of growing US shale production. Therefore, we expect a price of $60 per barrel for Brent at the end of 2017.”

James Sutton, client portfolio manager on the JPM Natural Resources fund, points out: “Now that debt levels are under control – post the massive deleveraging conducted in 2016 – this money will find its way back to shareholders through dividends and buybacks. [BHP Billiton spin-off] South 32 was the most recent large diversified miner to announce a share buyback of $500m [£390m].”

Mr Sutton thinks attractive investment opportunities lie in the base metals and oil and gas exploration and production sectors, with comparatively less value in the integrated oil majors and downstream sectors such as storage and transportation.

For those investors who believe the future of the sector is with cleaner, alternative forms of energy, there are also funds offering exposure to this area.

The Pictet Clean Energy vehicle invests in companies operating in the field of carbon-reducing technologies and equipment. In addition, the Guinness Alternative Energy fund states: “Over the next 20 years the alternative energy sector will benefit from the combined effects of rising energy prices, falling costs of alternative energy assets, energy security concerns and climate change and environmental issues.”

FE’S PICKS

BlackRock Natural Resources Growth & Income

This £50m fund, run by Tom Holl, Skye Macpherson and Alastair Bishop, targets stocks in three major sectors: energy, agriculture and mining. The team invests globally with no restrictions, and starts by taking a view on commodities such as oil, base metals and forestry, focusing on price direction and sector risks, before looking for companies likely to benefit from its outlook. The resulting portfolio is usually made up of around 50 stocks and has returned 6.5 per cent in the three years to June 27.

BlackRock New Energy

BlackRock announced Robin Batchelor was retiring from managing its energy funds at the end of 2015 with his departure seeing Mr Bishop take over this $1.1bn (£876m) fund. The manager focuses only on new energy stocks, with the investment universe consisting of solar, hydro and wind power-generating companies. The fund also includes firms involved in emissions reduction, power and smart grids, energy infrastructure and storage. The process combines company analysis with an overlay of broader trends in the industry and the economy as a whole. The vehicle has delivered a relatively impressive 41 per cent over three years.

EDITOR’S PICK

Investec Enhanced Natural Resources

Investec’s George Cheveley and Tom Nelson, who manage this £80m fund, believe resource prices in the short term are driven by supply and demand imbalances. The team forecasts underlying price trends in commodities, and invest in shares of global companies expected to benefit from these forecasts. The team also invests in direct commodities through derivatives, preferring equities, and targets companies where the share price does not fully reflect the underlying commodity price. The duo have returned 5 per cent over three years, but 40 per cent in the past 18 months.