Article 3 / 4

How multi-asset wrapped up the funds marketHow to assess multi-asset risk and reward

Ben Willis, senior investment manager for Whitechurch Securities, says it is unusual these days to see just one, standalone multi-asset fund on offer from a fund manager.

"Providers", he says, "will offer a range of funds, tailored to meet specific risk profiles. Traditionally, these would have sat within the old Investment Association sectors: Cautious, Balanced and Adventurous, which will limit the amount of equity exposure in the fund."

Now, these sit across four sectors: the three Mixed Shares sectors and the Investment Association Flexible Investment sector, as outlined in the first article in this guide.

But how can an adviser choose which one from these four sectors might be right for a client? And how, importantly, does one get the risk/return balance right for each individual client?

Risk profilers

Many investment advisers will use risk profiling tools to help assess the client's risk tolerance and risk appetite, with a view to defining a particular band of risk within which the client will be comfortable.

This can often lead to investors being directed towards the middle or either end of a spectrum of risk-rated model portfolios - often seven - with seven being the most risky and one being the least risky, as a guideline for the adviser to assess what sort of portfolio from a wide variety of fund managers would be the best fit.

Risk profiling tools have come a long way since the first suitability review of the sector back in 2011, when the former Financial Services Authority (FSA) (now the Financial Conduct Authority) found the over-reliance on "flawed" risk profiling tools could lead advisers to make decisions for their clients which could be prejudicial.

The 2011 report found that nine out of 11 risk profiling tools “had weaknesses which could, in certain circumstances, lead to flawed outputs” and led to questions as to whether these were fit for purpose.

Descriptions of risk on some tools were so unclear the FSA gave their creators a 'red flag' on the scoring system. Which was bad.

At the time, the FSA wrote:

- Although most advisers and investment managers consider a customer’s attitude to risk when assessing suitability, many fail to take appropriate account of their capacity for loss.

- Where firms use a questionnaire to collect information from customers, we are concerned that these often use poor question and answer options, have over-sensitive scoring or attribute inappropriate weighting to answers. Such flaws can result in inappropriate conflation or interpretation of customer responses.

The industry responded with better tools, more consumer-centric questionnaires and more rigorous testing of these models.

Although recently the current regulator the FCA has warned about advisers failing to offset any shortcomings of such risk-profiling tools with their own due diligence, the intrinsic issues the regulator had with risk profiling tools seems to be a largely historic problem.

At the moment, the majority of risk profiling tools available nowadays do useful guides for the adviser community. This is the view of Mr Willis, who explains: "More recently, we have seen the rise of independent risk profilers being used by the adviser community.

"The companies providing these risk profilers have approached fund providers and, in a commercial venture, have mapped multi-asset funds to their risk outcomes."

Once the funds have been through the process, which is monitored on an ongoing basis to ensure the fund is continuously risk rated (which had been an issue raised in previous years by the FCA), the fund can then be badged with the risk profiler's outcome.

Mr Willis says: "As a result, all of those advisers who use that risk profiler for their clients can then select from the multi-asset funds that fit with the same risk outcome."

Assessing suitability

For Chris Leyland, deputy chief investment officer for True Potential, selecting the right multi-asset fund for clients is far more than carrying out a simple risk versus reward assessment.

He comments: "It is vital to understand the clients’ expectations and needs, summarised as their investment goals. From there it is important to work out how you feel the fund will perform in differing market conditions."

He gives a list of questions to help decide whether a particular multi-asset portfolio will be suitable for any one client. These are:

- Can it offer something different to a traditional equity:bond fund?

- Does it hold assets that are lowly correlated or even uncorrelated to equity markets?

- How does the manager control risk?

- What is their currency exposure and how is this managed?

- What is the manager’s investment process?

- Does the fund give the client value for money?

Peter Sleep, senior investment manager for Seven Investment Management, says selecting the right multi-asset fund for a client is "usually the first thing a good financial planner does, and it is absolutely a regulatory requirement".

According to Mr Sleep: "A planner will usually have a questionnaire for clients to fill in, which will help the planner guide the client to the right balance of risk and return, and understand what the client is willing to lose."

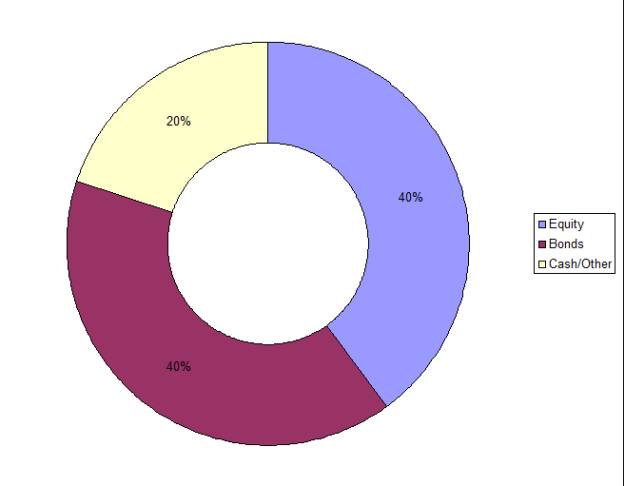

Usually, Mr Sleep adds, the most popular funds tend to be the 'balanced' funds in a multi-asset fund range, which are broadly comprised of an equal weighting of bonds and cash, as the pie chart below shows.

Typical breakdown of a balanced fund

Source: Seven Investment Management

"As a rule of thumb, the more the equity, the greater the risk," Mr Sleep states. "If clients are not happy with a large drop in one's investments, and find they cannot sleep at night when this happens, then they could go for a fund with very little equity content."

The investment horizon and the investment outcome

Rules of thumb aside, for Seven Investment Management, there is no 'grey' area when it comes to fund selection and assessing suitability, regardless of whether the client has answered enough questions to be categorised by a risk-profiling tool into a particular investor profile.

His colleague Chris Justham, relationships manager, says this sort of fact-find to assess an individual's objectives and risk tolerance acts as the first stage of a screening process. What also matters is understanding what the manager's process is and how this might fit with the client's own objectives and tolerance.

Mr Justham extrapolates: "With a multi-asset fund, there is a clear correlation between the level of equity/bond content and the risk.

"As a rule of thumb, the higher the equity, the greater the risk; the inverse is the same for the bond weighting. This can be a guide as to what may be appropriate for the client's risk profile.

"However, understanding the rationale behind a fund manager's investment process is important in assessing what may be appropriate here, as there can be a big difference between a 'static' asset allocation, and one that tactically adjusts according to the environment."

He adds the style of the manager will also inform the adviser on how his or her view of the world is implemented - whether through in-house solutions or best-of-breed third parties.

"Lifting up the bonnet and gaining an appreciation of the driving factors behind returns is a useful exercise."

For Andrew Harman, portfolio manager of the First State Diversified Growth fund, because the aim of investing is to achieve financial goals, one should ask whether the fund has delivered the required return over the investment horizon, for example whether it is to achieve cash plus 5 per cent or inflation plus 4 per cent.

He explains: "Achieving the investment return over the investment horizon is a key criteria in evaluating objective funds. Being too conservative could be risky as the fund may fall short of meeting its investment target."

Another question he believes advisers should ask is how the fund performed after adjusting for risk. Often this can be done using the Sharpe Ratio, which is a measure for calculating volatility adjusted excess return for a fund. It is calculated as the return earned in excess of the risk-free rate per unit of volatility.

"This provides investors with a tool to evaluate funds with similar return objectives and investment horizons," he states.

Managing large drawdowns

Mr Harman believes it is also important for advisers to pay heed to how often large drawdowns occur on the fund, and how long it takes for the portfolio to recover, as this could present a significant risk to some clients.

"A drawdown is the peak-to-trough decline over a period for an investment. The maximum drawdown provides an indication of the worst loss one would have experienced had they withdrawn their capital at an unfavourable time in the market cycle.

"It is also important to examine how long the portfolio took to recover from the loss. The portfolio needs to work harder after a drawdown as a 20 per cent loss requires a 25 per cent return to recoup the losses."

Knowing the client

Lukas Daalder, chief investment officer for Robeco, coyly suggests it is the client who ultimately chooses the fund that is right for them, based on what they want and having taken all the advice into consideration.

He explains: "Most clients would like to see a product with the volatility of a bond and an equity-like return, but this is a bit like looking for the unicorn.

"Sure, in the past year, with equity volatility dropping to extreme low levels, it was possible to achieve, but this is not attainable over a longer period."

This means it is up to the adviser not just to assess suitability for the client at the point of purchase, but over the course of the investment horizon, as clients' lifestyles, financial situations, and markets change.

Jonathan Webster-Smith, head of the multi-asset team at Brooks Macdonald, states the suitability test should be carried out by a professional adviser qualified to provide financial advice.

"As a discretionary investment manager, our managed portfolio service is available to clients only through professional advisers", he says, but cites four useful rules to test suitability:

- Determining the client's investment objectives.

- Reviewing their financial circumstances to determine what level of investment risk (or potential investment losses) they can bear.

- Ensuring they have adequate knowledge and understanding of the risks associated with the proposed service.

- Ensuring their investment portfolio is consistent with their investment objectives and risk profile.

According to James Dowey, chief economist and chief investment officer at Neptune Investment Management, it all comes down to truly knowing your client.

"Advisers really need to know their client: their circumstances, financial objectives and personality when choosing an overall portfolio for them," he opines.

"This means much more than simply matching a basic risk profile to a volatility number. They also need to educate them so they understand that, to meet their long-term financial objectives, they might need to accept some volatility along the way."

Mr Justham also believes it is important to understand what sort of measurable is the best fit for the client. "Is relative performance or targeted return the best fit for the client's objectives?"

Cost

Then there is the matter of cost. Multi-asset funds will by their nature incur higher trading costs than a single-strategy passive tracker fund and carry a larger management fee.

Data from Defaqto shows that, with an increase in equities within multi-asset portfolios, comes a commensurate increase in the overall charges.

Yet since 2014, these have been coming down; as the following tables from Defaqto show, between 2014 and 2018, costs for both multi-asset and multi-manager funds, analysed as part of Defaqto's diamond ratings methodology, have been on a downward trend.

2014 OCF | Mixed 0-35% | Mixed 20-60% | Mixed 40-85% | Flexible | Average |

| Multi-asset | 1.11% | 1.33% | 1.35% | 1.45% | 1.34% |

| Multi-manager | 1.53% | 1.78% | 1.71% | 1.75% | 1.73% |

| 2016 OCF | |||||

| Multi-asset | 1.09% | 1.07% | 1.16% | 1.31% | 1.18% |

| Multi-manager | 1.31% | 1.43% | 1.57% | 1.54% | 1.49% |

| 2018 OCF | |||||

| Multi-asset | 1.03% | 1.06% | 1.12% | 1.19% | 1.13% |

| Multi-manager | 1.17% | 1.42% | 1.35% | 1.41% | 1.37% |

| Source: Defaqto/Morningstar | |||||

Patrick Norwood, insight analyst for Defaqto, comments: "When we carried out our 2014 Diamond Ratings, the ongoing charge (OCF) for multi-asset funds was 1.34 per cent, while the average multi-manager was 1.73 per cent.

"2018 has again seen falls in the average OCF across both multi-asset and multi-manager as advisers and investors continue to focus on costs, and managers respond to this, with the multi-asset average falling by 5 basis points to 1.13 per cent from 2016, and multi-manager decreasing by 12 basis points to 1.37 per cent."

For Mr Justham, an adviser should be considering cost, as it is often "the variable which drives the preference for active or passive implementation".

This means a multi-asset fund comprised of purely passive plays with a slight asset allocation overlay will tend to be less costly overall for the client than a bells and whistles multi-asset portfolio that can invest in the whole range of permissible instruments and securities.

"Net performance is arguably the metric by which the argument should be settled", he comments, "although headline costs are often a key discussion point.

"Finding a fund whose style, performance and risk management fit within your proposition and client's objectives is the priority, although if this can deliver such elements using active or passive solutions, this allows a lot more flexibility for advisers during the recommendation process."

But the virtue of active management means the manager remains within a particular volatility boundary, with an expected level of return, despite the potentially higher cost.

Frank Potaczek, head of UK proposition for Architas, concurs. "A good multi-asset manager will look to diversify away from risks within a portfolio such as credit risk, market risk, currency risk and interest rate risk.

"This is what investors should be getting for the fee they pay for a multi-asset fund."

simoney.kyriakou@ft.com