2018 was a defining year for the policy of the world’s central banks as the monetary stimulus made available by governments after the global financial crisis started to be reined in.

The differing approaches by the world’s central banks in the coming 12 months will have a significant influence on bond performance, with asset allocation becoming far more important than it has in recent years.

“Central banks seem increasingly convinced QE [quantitative easing] has had its day and interest rates need to rise,” explains Schroders’ head of global macro strategy, Bob Jolly.

“Having fretted over the potential for inflation to fall into deflation, central bankers are willing to say such risks have receded enough to take away some of the QE punchbowl.”

David Riley, chief investment strategist at BlueBay Asset Management, explains that markets have been pricing in much of the anticipated policy tightening during 2018, which has led to a “deep decompression” theme.

This theme has been characterised by higher-rated credit performing slightly better than lower-rated credit, as investors repriced growth risk.

EM opportunities

Mr Riley believes that the wider markets may have “overshot” or “exaggerated” those risks, however, and this could now present an opportunity for canny investors, particularly in emerging markets.

“Given where rate expectations, equity and credit valuations have moved within emerging markets, we are setting up for a better starting point in 2019,” he confirms.

2018 was something of a setback for EM debt because of new US import tariffs and a cut in US corporation tax, but the broad consensus among fund firms is that emerging market fixed income markets will make a comeback in the coming 12 months.

“We view the 2018 pullback in emerging markets as a mere interruption in much more profound market forces, which should push the dollar lower in 2019 and beyond,” explains Ashmore’s global head of research, Jan Dehn.

“The tax cut and tariffs were designed to help Republicans in November’s mid-term elections but are unlikely to provide lasting support for the dollar,” he says.

US “soft landing”

With utterings of a potential slowdown in the US a feature in many of the year-end investment outlooks, fund managers are broadly expecting the US Federal Reserve to pause rate rises after June 2019. This would have the effect of cooling the domestic economy by urging banks to tighten their own lending criteria

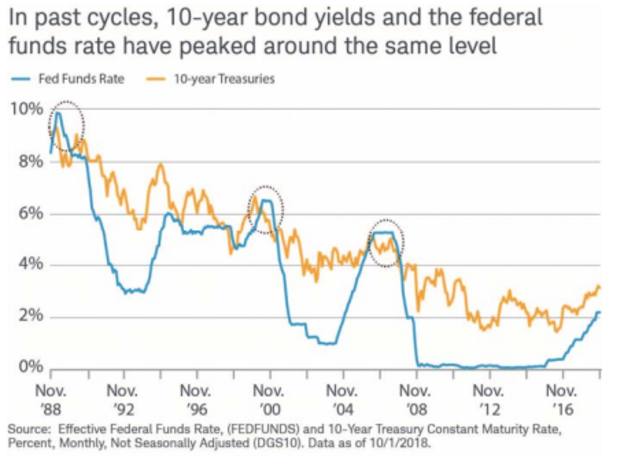

“The inverted curve means our forecast for 10-year US Treasury yields is lower than most,” says Vontobel Asset Management portfolio manager, Mark Holman.

“We think we see them back up over 3 per cent in the first quarter [of 2019] and then possibly as low as 2.5 per cent by the time the Fed pauses and the fear kicks in. Timing is going to be important in government bond markets in the year ahead.”

Source: 2019 Schwab Market Outlook

Columbia Threadneedle’s head of global rates and currency, Adrian Hilton, says that he also expects the US growth story to cool in 2019.

“Given that we think we have seen the best of US growth, our bias is towards lower yields over the course of 2019,” he explains.

“Against that, the normalisation of the Fed's balance sheet, and the evolution of monetary policy elsewhere, may exert a positive influence on term premia, which have been very compressed in all government bond markets.”

European opportunities

Vontobel’s Mr Holman expects European credit to outperform the US throughout 2019, and is anticipating that defaults will continue to be low throughout the coming 12 months, albeit up on the levels witnessed in 2018.

This view is shared by Columbia Threadneedle’s Mr Hilton and BlueBay’s Mr Riley, who agree that the eurozone looks robust from an economic standpoint, thanks to steady employment growth, increasing wages and relaxed borrowing conditions.

“European credit looks relatively attractive,” says Mr Riley. “We think that European credit, including bank debt, offers value at the current valuations.”

However, risks to watch for within Europe include any impact from a slowdown in China, according to Mr Hilton, who warns that the eurozone has become heavily reliant on exports in recent years.

He notes that the shaky relationship between the Italian government and the European Commission must also be watched closely by fixed income investors.

Then, there’s Brexit

Unsurprisingly, few investors were willing to give a firm view for how Britain’s scheduled exit from the European Union will impact UK fixed income assets.

Mr Riley simply remarks that there will be inevitable “associated complications”.

The true extent of such complications, of course, remain to be seen.

Joe McGrath is a freelance financial journalist