The long-term success (or otherwise) of the Eurozone’s first go at quantitative easing is still up for debate.

Nevertheless, it was an instant hit in some quarters and now hints from Mario Draghi, president of the European Central Bank, have its fans clamouring for more.

In the decade since recovery from the global financial crisis, the Eurozone’s economy has grown at only a very slow pace, peaking at a year-on-year rate of 2.8 per cent in the first quarter of 2011 and the fourth quarter of 2017.

Inflation in the region has also been determinedly sluggish.

Couple these with faltering German industrial production and the block’s position in the middle of the US-China trade dispute, and it is easy to see why the ECB recently downgraded its growth and inflation expectations to levels that highlight the need for more stimulus.

It now expects growth of 1.4 per cent next year, above our expectations of 1.1 per cent.

In June, the ECB stopped short of a rate cut, but Mr Draghi stated that “additional stimulus will be required” if economic performance continues in the same vein.

Since his speech in Sintra, Portugal, markets have moved quickly to price in a sharp slowdown in inflation.

In the past, such low expectations have triggered asset purchases from the ECB. Since the ECB needs to generate confidence in its ability to reach and maintain inflation at 2 per cent, it is very likely that, once again, QE will be a key part of its approach to raising inflation expectations.

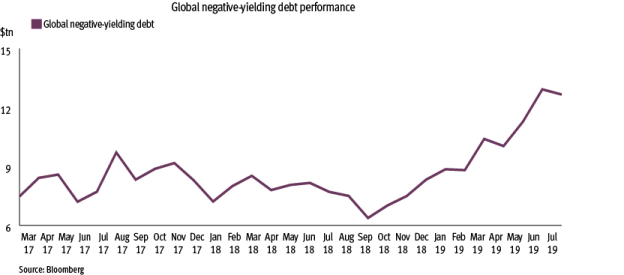

Already, we have seen government bond yields collapsing to lower levels.

At the time of writing, negative-yielding debt is valued at $13.1tn (£10.8tn) globally.

This trend is likely to continue and, with the ECB forecast to cut the deposit rate once again, a move towards -0.5 per cent for 10-year bunds cannot be ruled out. Investors’ search for yield, therefore, is leading them increasingly to longer-dated corporate bonds in Europe and further afield.

This should continue to support European credit, which has performed well over the first half of 2019. I expect it to continue to do so, supported by strong returns from government debt and a narrowing spread.

This dynamic is also likely to lift UK credit – European issuers make up just over 20 per cent of the UK market.

There are also likely to be some subtle differences from QE’s first European outing.

The ECB might adjust its self-imposed maximum limit on how much it can purchase from each government.

If it does, it might choose to make 50 per cent of the total purchases from the German market.

And because it will be keen to avoid political fallout from buying too many bonds from countries such as Italy, corporate bonds could get a much higher billing this time around.

Globally, the links between credit markets are strengthening.

Gaps in relative value between the sterling, euro and dollar bonds of any one issuer can be absent for extended periods.

With the ECB likely to be buying corporate bonds in secondary and primary markets from the end of this year, any difference in relative values between euro and sterling bonds from the same issuer is unlikely to exist for long.

While European corporate bonds have their attractions, it is important that UK investors do not forget what is driving the need for this second instalment of QE in the Eurozone.

The region’s troubles also put a spotlight on slowing UK growth and the increasing risk of recession.

It is not an environment in which credit would typically thrive.

We are looking to add to funds - companies with proven track records of coping well in downturns. Good asset quality and good governance are among the best indicators of star quality.

Luke Hickmore is investment director of fixed income at Aberdeen Standard Investments