Investment professionals will tell you there is no such thing as a crystal ball when it comes to working out where to put your clients’ money. There is, however, a heat map, launched by Kroll – a division of Duff & Phelps that specialises in risk analysis.

Kroll’s global teams of analysts have analysed hundreds of geographies and sectors to ascertain what effect Covid-19 has had on investment prospects across the world, mapping this against performance data, as well as known policy changes and central bank efforts to curb the financial impact of Covid-19.

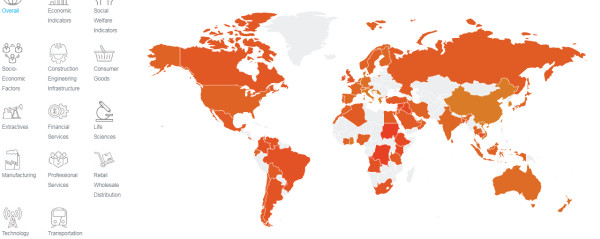

According to Louis-David Magnien, EMEA regional managing director in the business intelligence and investigations division at Kroll, the map has been designed to help investors and their advisers identify trends and tweak portfolios, within the context of individual’s specific requirements.

Mr Magnien said: “In terms of geographies, Covid-19 hit some developing markets somewhat later than developed markets. And the fiscal response from developing markets has been lower than that of developed markets.

"So the strength of these states or companies or banks in [the former] may be less supported than in Europe or the US or Japan, and there will be more dislocation in these markets.

“For this reason, geographically developed markets will probably remain a safer bet, depending on the level of risk one is willing to take.”

Some developing markets have weathered the storm very well, such as Vietnam, which the Kroll heat map places as having little to no negative impact as a result of Covid-19. But other developing markets will experience big knock-on effects, such as in Bangladesh.

The country’s textiles and clothing supply to western shops, a significant economic contributor to the country’s GDP, have been severely disrupted.

“With developing markets, the disruption is not just Covid-19 related, but other restrictions in travel and movement and flows of money will be felt relatively for quite some time, in our view,” Mr Magnien added.

Stimulus

One of the question marks of this crisis is whether countries’ individual responses have been the most appropriate.

For example, Brazil’s government has been accused of failing time and again to provide the right level of support, but some think Europe is over-stretching itself to offer help.

Last week, the European commissioner for the economy Paolo Gentiloni announced a “landmark” stimulus package of some €750bn (£661bn) to help economies damaged by the pandemic. Some of this will be in the form of loans that do not need to be repaid.

Japan also announced its cabinet had approved an additional $1.1tn (£800bn) budget to counter the recession.

The Kroll heat map focuses on public and regulatory reports to buttress qualitative analysis of economic, social welfare, and other socio-economic indicators of 61 key regions of the world.

Analysts located in each of these key regions provide qualitative assessments of nearly 30 such indicators, as well as regular updates.

Although the nature of the sources, reports, and other public information relied upon for this dashboard are subject to regional variances, its findings seem to be in line with what large fund management groups are also suggesting.

Jeremy Podger, portfolio manager of the Fidelity Global Special Situations fund, said it is important to work out the implications of huge support programmes on government finances in the long-run, as this can affect the ability of countries to rebuild their economies.

He said: “On the economic front, economies will avoid a spiral into depression due to liquidity being provided by central banks and direct government support for labour markets. Nevertheless, the economic shock will take time to repair: economic forecasters currently assume that GDP will recover to 2019 levels in the second half of 2021, depending on country specifics.”

Globally, he said as earnings forecasts typically follow GDP progression (typically with a lag), Fidelity sees earnings consensus for 2020 moving down close to 30 per cent from where it was at the start of the year.

Sector views

When it comes to individual sectors, Mr Magnien said one should look at trends that emerged during lockdown, such as online shopping and home working.

Research by digital commerce specialist JGOO shows 33 per cent of people expect to do more shopping online because they have become used to doing so during the coronavirus lockdown.

“These are trends that are not going to go away and, therefore, you have to consider whether the High Street shops are still worth investing in, and whether office real estate will be a long-term safe bet,” added Mr Magnien.

“We can already see from the heat map that online banking has increased in usage again. For example, in Columbia, there has been a 40 per cent surge in usage. Again, bricks and mortar may disappear as more online banking apps are used globally.”

But while these trends may affect sectors such as technology and property, albeit for different reasons, it is important, according to Mr Podger, to look at individual names and how their own earnings are likely to progress over the next three years, compared to previous expectations.

Individual companies

Mark Walker, managing partner at Tollymore Investment Partners, agrees it is important to drill down into company specifics to avoid risky blow-ups and stick with safer, perhaps less exciting, stocks.

He said: “Credit conditions of recent times have possibly allowed weak companies to thrive. This event-driven macro-crisis may expose those firms who have been swimming naked. Likewise, investors, seduced by a decade of low finance costs, have geared up their investments, leaving them ill-equipped to invest counter-cyclically. Both dynamics may exacerbate quoted price declines.”

This is why managers have said they are reviewing their portfolio holdings case by case, and focusing on those sectors and stocks where the prospect for longer-term performance is evident.

Mr Podger explains: “We have been adding holdings where valuations are cheaper, but three-year earnings prospects may be better than previously expected – mostly growth names – and also where stocks have performed poorly but the market has been unduly short sighted.

“Specifically, we have been adding to US health care, US refining, utilities in the US and Europe, and Asian insurance. We are also looking at Japanese electronics and machinery, which sold off more than fundamentals justify, as well as UK domestic names. Beyond that, we have a growing list of potential new investments in both value and growth names.”

Kroll’s analysis backs this up, with growth areas continuing to emerge in clean energy, such as Norway’s increasing output of electric cars, pharmaceuticals – as vaccines development gets underway – and luxury goods, as China’s big spenders start to make the most of the end of their lockdown.

Winners and losers

Mr Magnien’s view is that any business models rooted in the past will have to change now they have experienced this business disruption or they will fail. Stores that never operated online deliveries may have to make adapt quickly.

Care homes – a previously “safe infrastructure investment” – may face huge litigation costs over their handling of Covid-19. “So you need to make careful decisions,” he said.

But when it comes to a battle for survival, he does not think it is as simple as small or large. “With a crisis like this, governments such as the UK’s are doing the right thing to open the tap.

“The real risk is when the tap is closed – and the ability of firms to hold sufficient financial reserves will be very complicated. The smallest companies, unfortunately, will find it difficult to recover unless they have cash reserves.”

Therefore, clients without proper diversification may find themselves over-exposed to some pretty risky holdings.

simoney.kyriakou@ft.com