Despite widespread handwringing in the market over the current high valuations at which many equities trade, what we have seen for the past decade is not the pumping up of a ‘bubble’, instead it is a slowly growing structural imbalance that has created too much capital.

A bubble results from optimism-fuelled concentration within the pool of capital.

Despite idiosyncratic excitement in individual stocks and cryptocurrencies, this is not what is currently happening across markets as a whole. The reality is the pool of capital itself has surged relative to the available assets worth investing in.

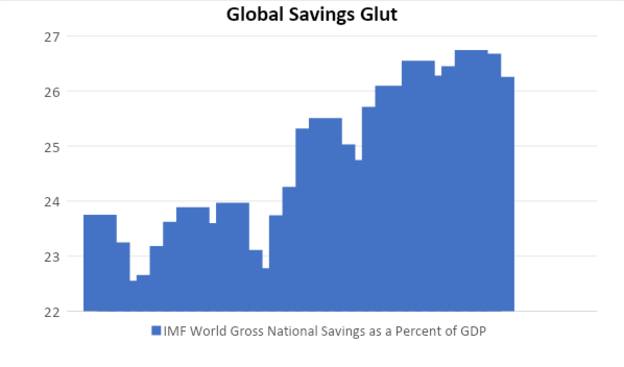

This expansion of capital was initially born out of pessimism. Personal spending and business investment have been timid for a decade, with global savings swelling as a result, and the cash saved from delayed consumption found its way into investment markets.

People may have delayed spending in anticipation of a recession that did not come in the decade after the financial crisis.

Source: IMF, World Bank, Bloomberg; Gross savings are calculated as gross national income less total consumption, plus net transfers. As of 8 January 2021.

The dominant investment dynamic became one where the pool of capital continuously outpaced the growth of investable cash flows.

This means the extra cash in the system from quantitative easing, and more recently from government spending, has gone into company shares, but the sluggish pace of economic growth means company earnings have not risen as fast as has the rate of increase of capital looking to invest in those companies, pushing valuations upwards.

If the savings glut diminishes, then the probability is the cash being spent would boost the earnings of companies, and so continue the positive environment for equities.

This dynamic caused more generous capitalization rates for all asset classes, rather than an overconcentration of a relatively stable pool of capital.

This isn’t to say certain specific market concentrations haven’t appeared. Private assets and fixed income in particular received growing shares of the expanding excess pool of capital, so valuations have risen. In the equities, the success of the ‘FAANGs’ (Facebook, Amazon, Apple, Netflix and Google), and other secular winners, masked the fact that overall investors have shed equities.

The structural imbalance between capital and investment opportunities has continued to worsen, particularly as savings and quantitative easing have bloomed during the coronavirus crisis and are likely to keep expanding over the coming months.

While the tapering of monetary support in 2022 will put pressure on asset prices, the global savings glut will linger for longer and likely take a decade to recede.

Meanwhile, economies and companies are only just beginning to recover from the pandemic, having operated significantly below capacity for nearly a year.

With significant slack remaining in the system, corporate earnings and cash flows have the potential to rise for several years until confidence and ‘animal spirits’ rise enough for investment to kick in.

If the savings glut diminishes then the probability is the cash being spent would boost the earnings of companies, and so continue the positive environment for equities.

These factors indicate that we are at the beginning of the cycle, rather than the end. With massive fiscal spending now more likely than not, growth is more assured. However, it will still take at least five years to dig the global economy out of the ditch and get back to neutral.

Until this output gap is closed, monetary policy will not cause inflation, the other major worry for investors, at a rate that will significantly derail asset prices. True, inflation will pick up, particularly via technical base effects in the spring. However, inflation will not last in a meaningful way while the economy has too much slack.

So how do we get out of this imbalance? For a start, growth should slowly chip away at the global savings glut as investment picks up. Meanwhile, demographic trends mean millennials are starting to buy their first homes, unleashing investment in housing.

These factors will help, but only slowly. A bolder approach would be for policymakers and corporates to massively increase investment in the hydrocarbon infrastructure needed to reorient the global economy towards clean energy.

This investment is needed to achieve ‘net zero’ emissions by mid-century, in line with Paris Agreement goals. Beyond an ethical imperative, green investment likewise represents one of the largest replacement cycle opportunities ever.

Asset owners’ increasing focus on ESG and engagement will be key to achieving this investment growth, but also requires a coordinated global policy response.

Overall, this backdrop of oozing capitalisation and rising growth is unlikely to significantly unwind markets, while the transition to a green economy may provide a bridge to grow our way out of this imbalance.

Rather than bursting bubbles, investors should focus on the long-term workout of the structural illiquidity imbalance and what this means for asset allocation. In particular, this environment favours a balanced approach between cyclical and secular growth, while avoiding the most defensive assets.

Michael Kelly is global head of multi-asset at Pinebridge Investments