Article 2 / 4

Guide to automatic enrolmentRight investment choices for auto-enrolment

Getting investment choices right for auto-enrolment schemes can be difficult, as there are many different factors to consider.

The first thing to bear in mind, according to Robin Armer, senior business development manager at NEST, is why investment is so important to the consumer.

He explains: "We are facing the first generation of savers who will rely almost entirely on their occupational defined contribution (DC) pensions to fund their retirement.

"Those DC schemes need to have investment strategies that are up to the challenge."

However, according to Glynn Jones, divisional director for group savings and investments for consultancy LEBC, the pensions freedom and choice regime, which came into effect in April 2015, has also muddied the waters.

Mr Jones explains: "The investment choice in pensions has become more difficult after pension freedoms, as there are three landing places: annuity, cash or drawdown.

"The employer must therefore decide both the correct risk profile of the investment funds within the auto-enrolment scheme he is setting up, and the landing place - which is beyond the knowledge an employer usually would have of the employees.

"Access to advice has, therefore, become way more important than before auto-enrolment. Default funds were supposed to make things simpler and more cost-effective."

Now, however, employers have to think well ahead to see how an underlying investment might perform for an employee depending on how that employee might, in 20 or 30 years' time, decide to take their pension entitlements.

Default

For now, most employers are relying on the provider's default funds to provide the right risk/return profile.

Helen Baker, partner for law firm Sackers, comments: "Investment choice is always important, particularly in relation to default funds as this is where most members' benefits will be invested."

She points to statistics from the Pension Policy Institute which revealed that 90 per cent of members are invested in their scheme's default funds. This increases to about 99 per cent for master trusts.

"Investment choices matter in terms of the ultimate outcome."

While some members may wish to choose their own fund, Mr Armer says research - both domestic and international - suggests most members will remain in the default fund.

To this end, he says: "In a world where there are no guaranteed outcomes, it is vital to assess how far a scheme's default investment approach can reduce uncertainty for members.

"People equate pension saving with the security and safety they need in old age, which runs counter to the idea their money could be 'at risk'."

Because of this, all default funds must have a good level of diversification, to smooth out the risk and volatility and encourage a wider range of assets to help the risk/return profile.

Nest's video gives an indication of how to carry out due diligence on default funds to ensure there is appropriate diversification.

According to Andy Beswick, managing director of business solutions for Aviva, diversification will vary between provider defaults but almost all will have allocations to equities (developed and emerging) and bonds (government and corporate).

He says: "Some [default funds] will access a broader set of asset classes, including high yield bonds, property and alternative asset classes.

"However, cost, and the cost of accessing the various asset classes, will play a significant role in determining the extent of diversification within a default. It’s worth remembering that typically only larger employers will ask advisers to create bespoke default funds for them.

"Most businesses, especially in the small to medium-sized market will use a default fund created by their pension provider."

Volatility and risk

"We believe taking investment risk is usually rewarded in the long-term but volatility in and of itself is not a good thing", says Mark Fawcett, chief investment officer for NEST.

This is why he advocates: "Smart risk management, true diversification and ongoing monitoring and oversight are likely to provide smoother long-term returns that build trust and limit the drag effect of excess volatility."

"Most members will look at returns and little else", comments Graham Peacock, managing director of the Salvus Master Trust.

"People bandy around 'lifestyle', 'target' and 'date' and 'de-risking' terms but good, solid returns, in a controlled risk environment is what most members want."

He adds: "Diversification for the sake of it is not a good thing, as it can dilute investment returns, but if a lack of diversification misses out on investment opportunities or increases risk, then not having enough diversification is wrong."

For this reason, he says getting the right level of risk and return is what a provider should focus on, by looking at modern portfolio construction theory, and allowing the manager to adapt it to changing market conditions where necessary.

Segmentation

The automatic nature of such workplace pensions means the due diligence around scheme and fund selection has to be "spot-on", says Andy Agathangelou, founding chairman of the Transparency Task Force.

He says this is important because there is "typically zero" input from the ultimate client when it comes to fund choice.

He explains: "The member is absolutely reliant on the decision of others, so duty of care must be paramount."

Yet according to Sackers' Ms Baker, it is tricky to assess whether a default fund is appropriate for a particular workforce.

This is especially in the context of the "new world of pension freedoms", and because of this complexity, she says there has been an increase in the use of multiple default funds.

This practice is sometimes referred to as "segmentation", which relies on a more active approach.

She comments: "Where segmentation is used, a review is carried out and different default funds or options are configured for different segments of DC members, based on the characteristics of those particular members.

"This will look at reasons why members are likely to want to invest in certain investments over others - for example, are they able to take more investment risk, or do they value stability over potential for greater investment growth, or do they want to draw down their benefits?

"The important thing here is to communicate the pros and cons of different funds", Ms Baker adds.

But according to Jason Green, head of workplace research for F&TRC, having too much choice of funds can be confusing and therefore unhelpful in an auto-enrolment context.

He explains: "Offering a range of lifestyle funds, alongside a number of more diverse funds, we would see as optimal.

"More is not always necessarily the best. Having a smaller, well-managed and controlled fund range is better than offering thousands.

"If people are given a limited choice, they are more likely to make a decision, while too much choice is overwhelming."

Duty of due diligence

Employers and trustees of schemes have specific duties when it comes to assessing and monitoring the investment performance of the pension scheme.

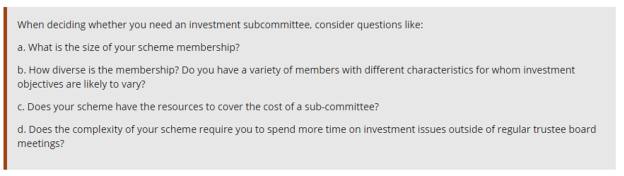

According to The Pensions Regulator (TPR), many schemes may consider setting up independent investment committees who can assess whether the underlying funds - including the default funds - are doing what they are expected to be doing.

There is a useful checklist on the regulator's website to help those involved in the monitoring and establishment of appropriate auto-enrolment investment portfolios, as well as information on what an independent committee or investment sub-committee - which could comprise the external financial advisers - should be examining.

Figure 1: What an investment subcommittee should consider (Source: TPR)

According to Chris Daems, director of Cervello Financial Planning, advisers too have a duty to examine whether the funds - default or otherwise - are diversified enough, and monitored adequately.

Advisers should also pay attention to total costs, performance and risk profiling, as well as the underlying investment choice.

Yet first and foremost, advisers have to make sure the employer (who is usually the client) is fully aware of what they are buying on behalf of their staff members.

Mr Daems says: "It is important to understand that, when we work in partnership with a client to support them with auto-enrolment, the client is usually the employer, not the individuals who are saving in the pension scheme.

"Typically, auto-enrolment schemes tend to have far less fund choice than a personal pension, and typically either have a fund or range of funds which uses lifestyle or target dated funds.

"As the employee tends to make the investment choice, our job as advisers is to provide an appropriate scheme, ensuring the auto-enrolment pensions provider has a decent default scheme as well as sufficient choice for the employees."

simoney.kyriakou@ft.com