Article 2 / 4

Guide to bitcoin and blockchainHow blockchain can revolutionise fiscal transactions

Blockchain, the global ledger technology outlined in the first article of this guide, is being explored and developed by institutions across the world and across sectors to see how it can be used to help make things easier and better for the end user.

For example, gaming on the blockchain is a real-world use case of the technology that could displace the whole gaming console industry.

Egor Gurjev, founder of the new blockchain gaming company Playkey, recently raised $10.5m (approx £7.4m) in an initial coin offering (ICO) and is working on ways to improve features such as remote game control.

But the technology can go far beyond gaming. Blockchain and distributed ledger technology (DLT) has practical uses across other sectors and industries.

Many are already in development, with cases being trialled and tested in a number of areas including digital identity management, energy trading, tracking development finance, music royalties and asset clearing and settlement.

Financial services firms in particular seem to be at the vanguard to be early adopters of the technology, believing blockchain can create lower-cost, higher-security and more compliant processes.

Last year in a series of talks during London Blockchain Week, Peter Bidewell, blockchain technology advisory consultant for Accenture, outlined a series of benefits blockchain could bring.

These include:

- Simplified IT infrastructure.

- Reduced cost of service.

- Enhanced regulatory compliance.

- Faster transactions.

- Tamper-proof know-your client (KYC).

- Improved cyber security.

- Instant clearing and settlement.

"While the benefits of blockchain technology are widespread, the benefits provided are especially well-suited to enhancing the financial services infrastructure," says Jim Bai, chief executive of futures trading platform EverMarkets, which uses open-source blockchain technology.

Cleaner processes

For example, as Dror Futter, partner at Rimon Law, outlines, the "unique attributes" of blockchain make it well suited to "address pain points" in the financial services industry.

He explains: "For example, the cost and speed of the share-trading settlement process could be significantly lowered through blockchain-based solutions, while providing greater accuracy and transparency."

According to Mr Futter, cross-border payments represent a similar set of "pain points" which could benefit from blockchain improvements.

The safety and security of blockchain processes - despite the recent accounts of cyber-hacking into cryptocurrency wallets - is improving at a pace, meaning financial services transactions using blockchain could stand to benefit from ever-more robust technology, especially where data is concerned.

For Matthias Kroner, co-founder and chief executive of Fidor Bank, data is an important point to mention. "Data will become an organisation's most valuable asset," he predicts. "Blockchain provides new ways for registering, storing, managing and interacting with data."

As a result, he also believes blockchain will become even more important as a foundation to the open banking concept.

Mr Bai is of a similar opinion: "As ongoing blockchain-based initiatives mature and the decentralisation movement continues, we expect efficiency to increase, transparency to prosper and systemic risk in the financial ecosystem to be mitigated.

"The benefits derived from the adoption of blockchain technologies will help to fortify our ageing financial services backbone."

Gerry Sachs, financial services regulatory attorney at Venable LLP, says this will only grow as open banking becomes the expectation of businesses and consumers looking for clean, streamlined, branchless banking concepts.

"Blockchain is not hampered by issues that stem from legacy technology systems. Importantly", he says, "it provides a clean technological base from which to build innovative products, and it is more flexible relating to development and use."

Registering ownership, transfers and escrow

For many advisers, insurers, pension funds, discretionary fund managers and anyone involved in financial services, the fact Blockchain has the potential for the secure storage of digital records is also a boon.

At present, because of its distributed nature, recording new assets on a blockchain can be quite slow, compared with the seconds or even nano-second that are typical of e-commerce. Consider the high latency of exchanges such as the London Stock Exchange, and compare this to the slow transaction times of blockchain, which can sometimes take hours or even days to record new assets.

But as firms build on this and develop it, the speed of registration will improve significantly.

Although it is not available currently, blockchain could be used to document financial transactions, such as mortgages, or to store compliance information for processes such as know your client and anti-money laundering compliance.

"If I can do a remittance payment with someone in Eastern Europe in minutes, compared with days in the traditional banking system", says Philipp Pieper, chief executive of Swarm Fund, "that is compelling and appealing."

Property, financial derivatives and even international financial transactions might also be a beneficiary of blockchain.

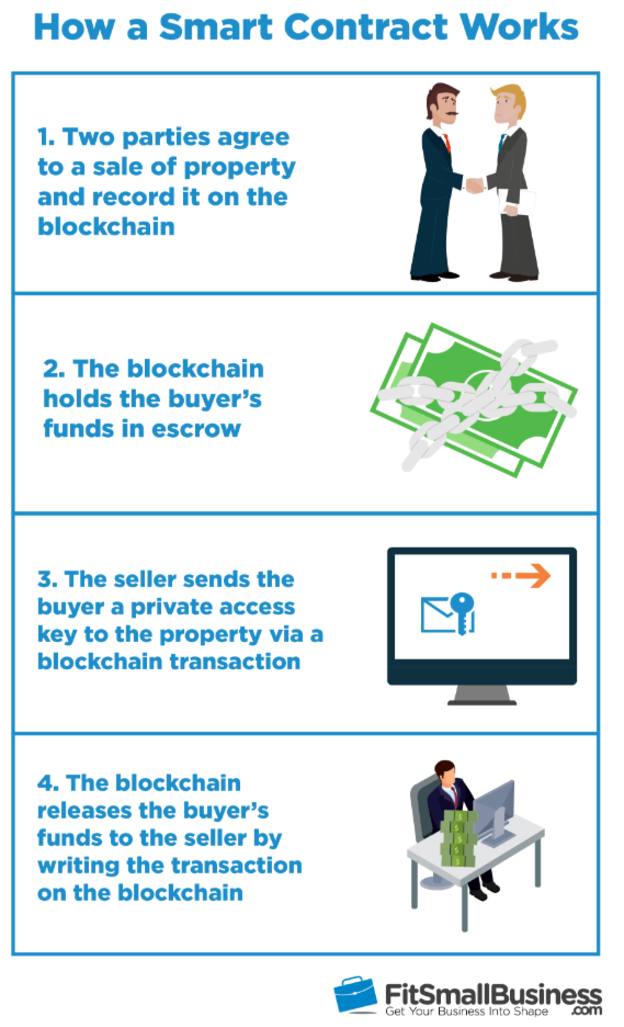

For example, smart contracts - such as the ones operating on Ethereum's blockchain - hold more than the register of the ownership of an asset.

This means the smart contract registers the full contractual terms of a transaction, and therefore can act as a distributed escrow agent, as well as a distributed property register.

Although recently mortgage lenders have been refusing to accept deposits made from investments in cryptocurrency - because they are not able to prove the money has come legitimately and not the by-product of money laundering somewhere down the virtual line - the theoretical use of blockchain in enabling quicker, smoother and easier property purchases marks a significant step forward in making transactions better for the end consumer.

Paul Domjan, global head of research, analytics and data for specialist investment house Exotix Capital, comments: "A smart contract may specify that when the transfer or a property deed is recorded in the blockchain, the payment for the property is automatically completed in digital currency.

"But if the deed is not transferred within a specific period, any deposit on the property, also made in the digital currency, is refunded.

"The same principle can be used for transactions ranging from financial derivatives to international trade."

Banks, especially as there is a move towards open banking, are engaged in launching blockchain-based ways to transact with each other, such as JPMorgan Chase, whose chief executive Jamie Dimon famously called Bitcoin a "fraud" in 2017, at the same time his company was launching a blockchain-based system.

He retracted his comments in January this year, according to an article in sister paper the Financial Times.

But Greg Carter, co-founder and chief executive of online platform Growth Street, is more sceptical: “Undoubtedly, blockchain technology is a valuable innovation, which could change the way money is moved around the world - among myriad other possibilities.

"However, I don’t believe that cryptocurrencies, or indeed blockchain technology more generally, serve much substantive purpose at all for industries like commercial finance."

In fact, he adds: "The blockchain could potentially undermine several central tenets of a field like commercial lending. At its core, a distributed ledger prioritises encryption and anonymity.

"A basic principle for lenders and borrowers alike in a commercial agreement should be that the parties on either side of a transaction know and trust each other."

No more middlemen

For consumers who are tired of having to go through layers of bureaucracy or countless middlemen to get to their investments, Mr Futter comments that using smart contracts on chains such as Ethereum means greater automation and fewer administrators.

He explains: "Financial services processes can be automated and executed and reduce or eliminate the need for middlemen."

Because of this, blockchain can also help to encourage competition and remove the competitive advantage that some traditional companies have simply because of their size or longevity in the market.

Clem Chambers, chief executive of ADVFN, is grateful for the "disintermediation" which is enabled by the policies underpinning the database technology of blockchain.

"Its decentralisation breaks the business moats of many decentralised businesses that rely on gate-keeping and rent-seeking for their businesses," he explains.

By this he means blockchain could break through a firm's ability to maintain competitive advantages over its competitors in order to protect its long-term profits and market share from competing firms.

Developments in 2018

Will 2018 be the year in which the wider financial services industry starts to develop and roll out blockchain-based concepts?

Mr Rutter thinks so. "Players across the financial services industry are engaged in blockchain proof-of-concepts. There is a growing sense that 2018 will be the year where the best of these projects transition to commercial rollouts."

A lot of it comes back to the fact that the end consumers, as evidenced by the jump in Bitcoin's capitalisation from approximately $16bn early on in 2017 to $326bn in December 2017 (before falling back to $110bn in January) "want this to exist", says Mr Pieper.

"It's not just the technology but also the interest, attention and credibility that has come into the space today," he believes.

Ari Nazir, managing partner and chief investment officer of the $APEX Token Fund - a tokenised cryptocurrency fund of hedge funds for retail investors - thinks 2018 will be the year that central banks get in on the blockchain act.

He says: "We expect major central banks, such as the Bank of England, will release public roadmaps for incorporating blockchain technology into their monetary policy management."

It is already fast becoming a possibility for making it easier for people to invest in frontier market investments, given the relatively lower levels of financial regulation in the so-called frontier markets.

In a report by specialist investment firm Exotix Capital, because of poor infrastructure, lower regulation and poor ownership records, this means the barriers to blockchain succeeding is much lower than it is in developed markets with excellent infrastructure, records and high levels of regulation.

The report commented: "Frontier markets may be positioned to leapfrog developed economies through blockchain and cryptocurrencies.

"There are four key functions that blockchain technology and cryptocurrencies provide, which are of unique utility in frontier economies with weak economic and governance institutions." These are:

- A clear reliable record of ownership (blockchain).

- A mechanism for contract enforcement (blockchain).

- A means of exchange (crypto).

- A store of value (crypto).

Because blockchain can provide a "clear, reliable record of anything", this could help more companies in frontier markets to develop these technologies and produce greater returns, without having to deal with weak governments, and potentially remove some barriers for overseas investors to benefit from such innovations.

For Mr Chambers, the possibilities are boundless: "Blockchain will increase productivity in some of the most change-resistant industries and thereby create huge value by releasing resources into higher value-added areas."

simoney.kyriakou@ft.com